B-422666.2 [archived PDF], Perimeter Security Partners, LLC—Costs, August 8, 2025

Perimeter Security Partners, LLC (PSP), a small business of Brentwood, Tennessee, requests that our Office recommend that it be reimbursed for the costs of filing and pursuing its protest challenging the issuance of a task order to Low Voltage Wiring, Ltd. (LVW), a small business of Colorado Springs, Colorado, under request for quotations (RFQ) No. W912DY-24-R-0008, issued by the Department of the Army, U.S. Army Corps of Engineers (Corps), for preventative and corrective maintenance services for access control points at 19 Army installations in the northeast region of the United States. PSP argues that it should be reimbursed its protest costs because the agency unduly delayed taking corrective action in response to its clearly meritorious protest.

The Congressional Review Act (CRA) requires that before a rule can take effect, an agency must submit the rule to both the House of Representatives and the Senate, as well as the Comptroller General. CRA adopts the definition of “rule” under APA but excludes certain categories of rules from coverage. We conclude that the 2025 Policy Statement is a rule for purposes of CRA because it meets the APA definition of a rule, and no CRA exception applies. Therefore, the Policy Statement is a rule subject to CRA’s submission requirements.

Ever since new tariffs were enacted in early 2025, a key policy question has been what is the extent to which businesses will pass tariff costs through to prices, and when? The effects of a tariff are rarely straightforward, given, among other things, competitive dynamics and the challenges of implementation, but the historically large and changing nature of these tariffs have created additional levels of uncertainty over the effects.

In uncertain times, anecdotal evidence from businesses can be especially insightful. We are learning how businesses are reacting to tariffs through the Richmond Fed’s business surveys as well as through hundreds of one-on-one conversations with Fifth District businesses since the start of 2025.

These conversations showcase that navigating tariffs is a complex and sometimes protracted process for firms, particularly when there is uncertainty. Firms describe several reasons they may not have experienced the full impact of proposed tariffs yet (even when goods and countries they deal with are subject to them), as well as reasons that even when they have incurred tariff-related cost increases, there can be a delayed impact on pricing decisions.

Reasons Firms May Not Have Incurred Tariffs Yet

Business contacts describe several strategies or circumstances that can delay or reduce the tariffs on inputs or other imported items. These include the following:

Delayed ordering. In response to announced tariffs, many firms ran down existing inventories or ran inventories lean in hopes that tariffs would become lower. For example, a national retailer said everyone was “delaying all we can delay in hopes we get more clarity on trade deals” and reported meeting with procurement teams multiple times per week to discuss ports and ship capacity, evolving tariffs, and inventories to keep goods flowing and prices as low as possible. One port said they have a crane waiting to be shipped but can’t do so now due to the tariffcost.

Cost-sharing.Vendor relationships are often long term, and many firms report partnering with suppliers and customers to share costs. When tariffs first rolled out, multiple firms (a beverage distributer, supply chainlogistics company) anticipated a “rule of thirds” where the cost was split evenly among the supplier, the importer, and the customer. A national retailer reported being large enough to force suppliers to bear much of the cost, though it varied by relationship and item. Interestingly, firms also reported that cost-sharing is not necessarily a permanent solution: A steeldistributer said that with the second round of tariffs announced in June, “The ‘kumbaya’ of cost-sharing was likely to come to an end.” Similarly, a fabricmanufacturer said that upon an announced trade deal with Vietnam that took tariffs from 10 percent to 20 percent, suppliers took a new stand on cost sharing: “Most vendors said you’re on your own” for the second 10 percent, and one even clawed back cost-sharing from the first round.

Transit time. It takes up to six weeks for container ships to arrive to the East Coast from China, so even if firms are ordering goods, there is a natural delay when the tariff is incurred. Shipping time in a world of rapidly changing tariff proposals add to uncertainty around tariffcosts.

Tariff implementation delays.Richmond FedeconomistMarina Azzimonti has found that a variety of tariff implementation delays help explain why actual tariffs as of May 2025 were much lower than expected. These factors include legacy exemptions and delays in customs system updates. Azzimonti also finds that a small percentage is explained by countries substituting away from high-tariff countries. For example, one national retailer we spoke with was in the process of dropping 10 percent of products sourced from China. Whether a company can change sourcing varies dramatically by type of firm and product.

As our monthly business surveys have found, many firms report deploying more than one strategy to delay tariffs. Notably, many of these delays are only temporary.

Reasons Tariffs May Have a Delayed Impact on Prices

Even when firms have incurred tariffs, they give several reasons why tariffs may not be immediately reflected in the prices they charge for their products. These include the following:

Waiting for tariff policy to clarify. Higher prices could reduce demand for goods and services and/or lead firms to lose market share, so many firms said they are hesitant to increase prices until they’re sure tariffs will remain in place. For example, a large national retailer said if tariffs are finalized at a sufficiently low level, they’ll absorb what they’ve incurred to date, but if high tariffs stick, they’ll have to raise prices. A steel fabricator for industrial equipment described being reluctant to raise prices on the 10 percent cost increases they’d seen thus far but would have to raise prices should the increases reach 12 to 13 percent. A grocery store chain was reluctant to raise prices and instead might reduce margins, which had recovered in recent years, to maintain their customer base. Some firms explicitly noted a strategy to both raise prices over time and pursue efficiency gains to cut costs and completely restore margins within a year or two.

Elasticity testing. Firms reported testing across goods whether consumers will accept price increases. A furnituremanufacturer said he’s seen competitors pass along just 5 percentage points of the tariffs at a time so it isn’t such a huge shock to customers, though in that sector, “We all end in the same place which is the customer bearing most of it.” A national retailer said most firms are doing a version of stair-stepping tariffs through, e.g., raising prices a small amount once or twice to see if consumer demand holds, and if so, trying again two months later. This retailer said prices were going up very marginally in early summer, would increase more in July and August, and would be up by 3 to 5 percent by the end of Q4 and into 2026. Another national retailer said they would start testing the extent to which demand falls with price increases, e.g., when the first items that were subject to tariffs—in this case back to school items—hit shelves in late July.

Blind margin. Some firms reported attempting to pass through cost in less noticeable ways. While any price increase to consumers will be captured in measures of aggregate inflation, the fact that price increases may occur on non-tariffedgoods might make it difficult to directly relate price increases to tariffs. An outdoor goodsretailer said, “Unless it’s a branded item where everyone knows the price, if something goes for $18, it can also go for $19.” A national retailer plans to print new shelf labels with updated pricing, which will be less noticeable for consumers compared to multiple new price stickers layered on top. This takes time (akin to a textbook “menu cost” in economics), so it will not be reflected in prices until July and August. A grocery store said their goal was to increase average prices across the store but focus on less visible prices.

Selling out of preexisting inventory: Many firms noted they still have productioninventory from before tariffs were announced, so they do not need to raise prices as long as they still sell these lower cost goods. A national retailer noted they have at least 25 weeks of inventory on hand for most importedproducts. A firm that produces grocery items said they will decide how much to raise prices as they get closer to selling tariff-affected products. Similarly, retailers order seasonal items quarters in advance. Many were receiving items for fall and winter when the new tariffs were going into effect in the spring. They paid the tariff then, but we won’t see the price increase until those items hit the shelves in the fall or winter. One retailer speculated that seasonal décor items will look the most like a one-time increase.

Pre-established prices. Many firms face infrequent pricing due to factors like annual contracts or pre-sales. For example, a dealer of farm equipment gets half its sales through incentivized pre-sales to lock in demand and smooth around crop cycles. They noted that while it would be difficult to retroactively ask those customers to pay for part of the tariff, they will pass tariffs directly through on spare parts. A steel fabricator for industrial equipment has a contract for steel through Q3, so they haven’t been impacted yet by price increases. However, they will face new costs once that contract expires.

In general, compared to small firms, large firms have more ability to negotiate with vendors, temporarily absorb costs, burn cash, wait for strategic opportunity, and test things out. This matters because large firms often lead pricing behavior among firms, so these strategic choices may influence the response of inflation to tariffs more generally. Even within firm size, one often hears that negotiations on price vary considerably by relationship and item.

Conclusion

A key question surrounding tariffs is whether any effects on inflation will resemble a short-lived price increase—as in the simplest textbook model of tariffs—or a more sustained increase to inflation that may warrant tighter Fedmonetary policy. When asked in May what will determine the answer, Fed ChairJerome Powellcited three factors [archived PDF]: 1) the size of the tariff effects; 2) how long it takes to work their way through to prices; and 3) whether inflation expectations remain anchored. The insights shared above suggest the process from proposed tariffs to the prices set by firms is far from instantaneous or clear-cut, particularly when tariff policy is changing.

Sensing from businesses suggests that the impact of tariffs on their price-setting [archived PDF] has been lagged, but it is starting to play out. Nonetheless, it remains highly uncertain how tariffs will impact consumerinflation. The discussion above makes clear that firms are nimble and innovative in the face of challenge, and they are concerned about losing customers in the current environment, particularly consumer-facing firms. We will continue to learn from our business contacts and share their insights.

by Hamza Abdelrahman, Luiz Edgard Oliveira and Aditi Poduri

Information the San Francisco Fed collects from businesses and community sources for the Beige Book provides timely insights into economic activity at both the national and regional levels. Two new indexes based on Beige Book questionnaire responses track business sentiment across the western United States. The indexes track data on economic activity and inflation, serving as early indicators of official data releases and helping improve near-term forecasting accuracy. The latest index readings suggest weakening economic growth and intensifying inflationary pressures over the coming months.

This Economic Letter examines the economic information collected through the SF Fed’s Beige Book questionnaire over the past 10-plus years. We analyze this information by constructing sentiment indexes from the qualitative data and comparing them with quantitative measures of national and regional economic activity and inflation. We introduce two indexes—the SF Fed Business Sentiment Index and the SF Fed Inflation Gauge Index—which track our contacts’ views and expectations for economic growth and inflation, respectively. We find that these new indexes serve as reliable early indicators of official data releases and help improve near-term forecast accuracy. The SF Fed Business Sentiment Index has generally exhibited patterns similar to other recent business and household sentiment indexes, and the SF Fed Inflation Gauge Index has shown a strong uptick in expected inflation. To regularly monitor changes in these two indexes, the San Francisco Fed has launched a new Twelfth District Business Sentiment data page.

Constructing regional sentiment indexes

The San Francisco Fed sends out a Beige Book questionnaire to business and community contacts across the District eight times a year to gather regional information. In addition to answering questions regarding their organizations, respondents share their views on regional and national topics, including economic activity and inflationary pressures.

In two questions, respondents indicate whether they see national output growth and inflation rates increasing, decreasing, or staying stable over the coming year using a standard five-tiered scale. We use these responses since 2014 to formulate two business sentiment indexes, one on economic activity and another on inflation. We assign standard weights to the five-tiered qualitative scale that are symmetrical around zero. For example, we ask if activity is expected to “decrease significantly” = –2, “decrease” = –1, “remain unchanged” = 0, “increase” = 1, or “increase significantly” = 2. We add up the weighted shares of responses for each tier within each index. We then normalize each resulting series by its own average and standard deviation for ease of comparison with traditional economic indicators.

Tracking business sentiment

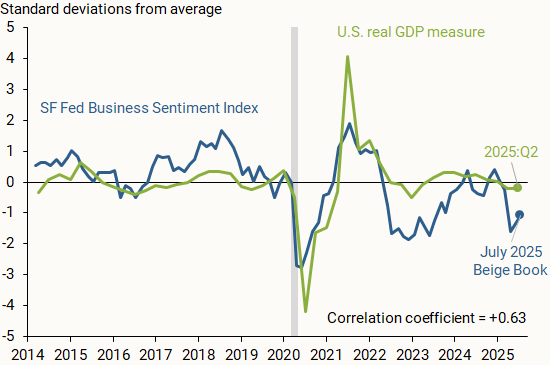

Figure 1 shows how the SF Fed Business Sentiment Index (blue line), compiled from responses to the question on national economic activity, compares with data on changes in national GDP (green line). We measure national output as the four-quarter change in inflation-adjusted, or real, GDP, normalized by its average and standard deviation so that it is centered around zero and, hence, more directly comparable to the SF Fed Business Sentiment Index. The vertical axis shows how many standard deviations away each observation is from its respective measure’s average from 2014 to mid-2025.

Figure 1 Economic growth versus business sentiment

The SF Fed Business Sentiment Index generally tracks the movements in national GDP over the past decade; a correlation coefficient of +0.63 on a scale of –1 to 1 indicates a moderately strong positive relationship between the two measures. A relatively recent exception started in 2022, when our index began showing a considerable decline relative to the national GDP measure. Respondents across the District were downbeat about economic growth and reported expectations of a sharp decline in consumer spending and overall household financial health following the depletion of pandemic-era savings (Abdelrahman and Oliveira 2023). A similar decline appeared in other measures of business and household sentiment. Nevertheless, overall economic growth continued at a solid pace. This decoupling between sentiment and hard data that began in 2022 was dubbed a “vibecession” (Daly 2024, Scanlon 2022).

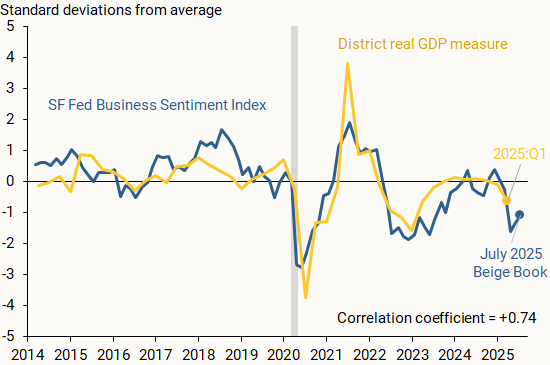

Another possible reason for the divergence between national real GDP and our Business Sentiment Index is the influence of the regional economy. Although respondents are asked about their views of national GDP, their responses may be affected by regional outcomes. Thus, our index may also reflect a regional perspective from our business and community contacts.

Figure 2 supports this rationale, showing the SF Fed Business Sentiment Index alongside a measure of regional output growth (gold line). We find that the measures closely track one another, including for 2022 and 2023, with a correlation coefficient of +0.74. We define District real GDP growth as the year-over-year percent change in the total output of the District’s nine states as reported by the Bureau of Economic Analysis (BEA). We normalize the series as described before.

Figure 2 Regional economic growth and business sentiment

Our findings indicate that the SF Fed Business Sentiment Index can serve as an accurate early indicator for national and regional output growth. Since the regional Beige Book questionnaire is collected twice each quarter, it provides particularly timely insights into economic activity during the current quarter. By contrast, the first GDP data release for any given quarter usually arrives a full month after that quarter has ended, and initial data releases for state-level output growth arrive with even more delay.

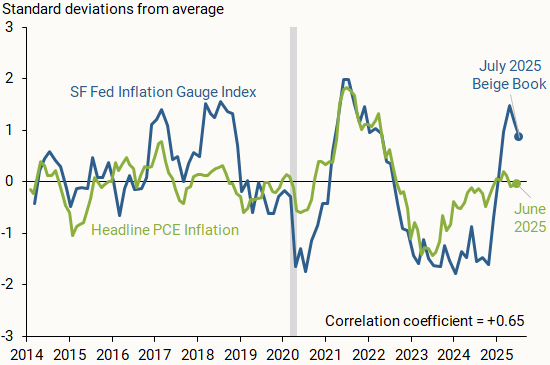

Our Beige Book questionnaire responses also provide insights into how business and community contacts in the District see national inflation evolving. Figure 3 compares the SF Fed Inflation Gauge Index (blue line) with monthly changes in the year-over-year headline personal consumption expenditures (PCE) inflation rate published by the BEA (green line). We normalize the inflation series and index as discussed earlier.

Figure 3 SF Fed Inflation Gauge Index versus realized inflation

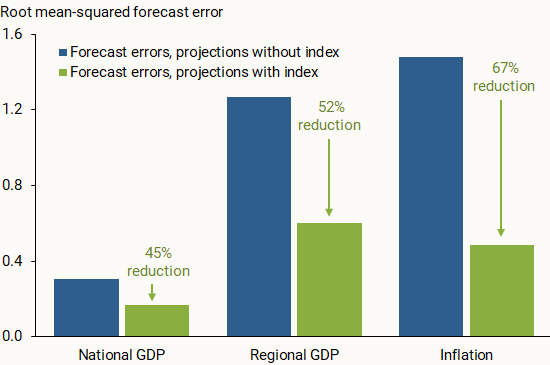

Beyond tracking data on national and regional economic conditions, we consider whether our two indexes can help improve one-year-ahead projections of output growth and overall inflation. We run linear regressions on a 2014–2022 data sample and estimate out-of-sample projections for the period starting in the first quarter of 2023. We run this analysis for the three economic measures—national GDP, regional GDP, and inflation—once with our index included on the right-hand side of the regression equation and once without the index. For this analysis, we use versions of the SF Fed Business Sentiment Index and the SF Fed Inflation Gauge Index that have been aggregated quarterly.

Figure 4 compares the out-of-sample projection accuracy of the two iterations. Across all economic measures, incorporating the SF Fed Business Sentiment Index or the SF Fed Inflation Gauge Index in the regression noticeably reduced the forecast errors for the out-of-sample period. This general result appears to hold when we project output growth and inflation one quarter ahead, in line with other studies that incorporate soft data from the Beige Book in short-term projections (Balke and Petersen 2002). The results are also consistent when using a local projections method from Jordà (2005) for one-year-ahead projections of output growth and shorter-term projections of inflation. This further supports the usefulness of our qualitative measures as early indicators of the future economic landscape over the short term.

Figure 4 Forecast errors with and without SF Fed sentiment indexes

Information collected from businesses and communities through the San Francisco Fed’s regional Beige Book questionnaire can provide valuable insights into the national and regional economies. Sentiment indexes described in this Letter use responses from Twelfth District Beige Book contacts to generally track economic activity and inflation. Our two indexes serve as reliable early indicators of official data, which could help improve near-term forecast accuracy. The SF Fed Business Sentiment Index remained negative for much of 2022 and 2023, possibly reflecting more subdued growth within the District relative to the United States. Meanwhile, the SF Fed Inflation Gauge Index spiked in recent months following adjustments to trade policy.

As programmable payments become more common, an old-school budgeting idea is making a comeback: earmarking. At its core, earmarking just means setting money aside for a specific purpose—like rent, payroll, or taxes—so it’s only used for that. It’s a simple concept, but when combined with automation, it could be the budgeting upgrade many people and businesses have been waiting for.

The word “earmark” dates to the 15th century, when farmers would notch their animals’ ears to show ownership. Over time, it came to mean setting something aside for a specific use. In personal finance, this idea lives on in the envelope system, where people divide up cash into labeled envelopes—groceries, bills, savings—and stick to those limits. It works, but let’s face it: handling cash envelopes isn’t exactly practical in a digital-first world.

That’s where programmable payments come in. These are payments that happen automatically based on rules you set. Instead of stuffing envelopes, you set up digital “buckets” for your money. Maybe 20 percent of every gig workpayment goes straight to a tax account or your weekly paycheck splits into rent, groceries, and savings buckets automatically.

Through banking apps, digital wallets, or budgeting platforms, consumers choose or create spending categories and assign rules—like percentages, spending limits, or triggers. For example, you can link your checking account to a programmable wallet that auto-transfers money into savings or investments accounts on payday, or prevents spending on dining once you hit your monthly cap.

It’s like having a personal money assistant organizing your finances, paying your bills, and keeping you on budget without you having to think about it. For businesses, this brings new efficiency to managing payroll, vendorpayments, and escrow accounts.

The upside of earmarking with programmable payments is clear: automation takes the work out of budgeting, real-time visibility helps track your money, and flexible rules let you customize how it all works. It’s also useful in more regulated settings like distributing aid or managing shared accounts because it adds accountability.

But if the rules are too rigid or confusing, that can frustrate users. Businesses may need to integrate programmable features with legacy systems, which takes time and money. And over reliance on automation poses risks—glitches, errors, or outdated settings can cause missed payments or unintended consequences.

Still, earmarking with programmable payments is a smart, modern take on a tried-and-true budgeting technique. It may not be right for every situation—and some apps already do this behind the scenes—but used intentionally, it can bring clarity, control, and purpose to the way money flows. In a complex financial world, that’s something both individuals and experts can benefit from.

[from NBK Group’s Economic Research Department, 21 November, 2024]

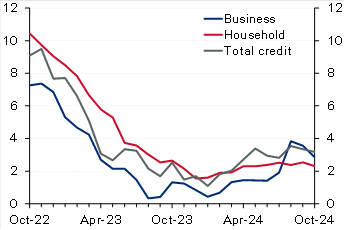

Kuwait: Solid credit growth in October driven by household credit. Domestic credit increased by a solid 0.4% in October, driving up YTD growth to 2.9% (3.2% y/y). The recovery in household credit continued, with growth in October at a solid 0.5%, resulting in a YTD increase of 2.4%. While y/y growth in household credit remains a limited 2.3%, annualized growth over the past four months is a stronger 4.7%. Businesscredit inched up by 0.2% in October, pushing YTD growth to 3.6% (2.9% y/y). Industry and trade drove businesscredit growth in October while construction and trade are the fastest growing YTD at 17% and 8%, respectively. In contrast, the oil/gas sector continued its downtrend, deepening the YTD decrease to 13%. Excluding the oil/gas sector, growth in business credit would increase to a relatively good 5% YTD. Looking ahead, the last couple of months of the year (especially December) are usually the weakest for businesscredit, likely due to increased repayments and write-offs, but it will not be surprising if the recovery in household credit is generally sustained, especially given the commencement of the interest rate-cutting cycle. Meanwhile, driven by a plunge in the volatile public-institution deposits, resident deposits decreased in October, resulting in YTD growth of 2.4% (4.2% y/y). Private-sectordeposits inched up in October driving up YTD growth to 4.5% compared with 10% for government deposits while public-institution deposits are a big drag (-14%). Within private-sector KD deposits, CASA showed further signs of stabilization as there was no decrease for the third straight month while the YTDdrawdown is a limited 1%.

Chart 1: Kuwait credit growth

(% y/y)

Source: Central Bank of Kuwait (CBK)

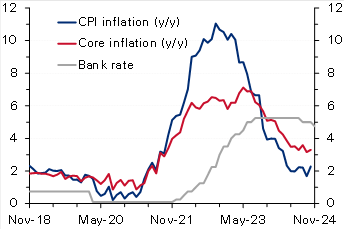

Chart 2: UK inflation

(%)

Source: Haver

Egypt: IMF concludes mission for fourth review, sees external risks. The IMF concluded its visit to Egypt after spending close to 2 weeks, holding several in-person meetings with the Egyptian authorities, private sector, and other stakeholders. The IMF released a statement mentioning that the current ongoing geopolitical tensions in the region in addition to an increasing number of refugees have affected the external sector (Suez Canal receipts down by 70%) and put severe pressure on the fiscal front. The Fund acknowledged the Central Bank of Egypt’s commitment to unify the exchange rate, maintain the flexible exchange rate regime, and keep inflation on a firm downward trend over the medium term by substantially tightening monetary policy. It also highlighted that continued policy discipline was also a key to containing fiscal risks, especially those related to the energy sector. The Fund, as always, re-iterated the need for promoting the private sector mainly through an enhanced tax system and accelerating divestment plans of the state firms. Finally, it also said that the discussions would continue over the coming days to finalize the agreement on the remaining policies and reform plans. However, the release did not provide any clear hints about the conclusion on the government’s earlier request to push the timeline of some of the subsidy moves.

Oman: IMF completes article IV with a strong outlook for the economy in 2025. Oman’s economy continued to expand with growth reaching 1.9% in the first half of 2024 (versus 1.2% in 2023), despite being weighed down by OPEC+ mandated oil production cuts as non-oil GDP grew a stronger 3.8% y/y in H1 (versus 1.8% in 2023). The fiscal and current account balances remain in a comfortable situation evident by a decline in public sectordebt and the recent rating upgrade to investment grade. The Fund expects Oman’s economic growth to see a strong rebound in 2025, supported by higher oil production. It also believes that fiscal and current account balances will remain in surplus but at lower levels. Key risks to the outlook stem from oil price volatility and intensifying geopolitical tensions. The IMF also mentioned that further efforts are needed to raise nonhydrocarbon revenues through more tax policy measures and the phasing out of untargeted subsidies which should help in freeing up resources to finance growth under the government’s diversification agenda.

UK: Inflation rises more than forecast, reinforcing BoE’s caution on rate cuts. UKCPIinflation increased to 2.3% y/y in October from 1.7% the previous month, slightly above the market and the Bank of England’s forecast of 2.2%. On a monthly basis too, inflation rose to 0.6%, a seven-month high, from September’s no change. The steep rise was mainly driven by an almost 10% rise in the household energy price cap effective from October. Core inflation also accelerated to 3.3% y/y (0.4% m/m) from 3.2% (0.1% m/m). While goods prices continued to fall (-0.3% y/y), service prices rose at a faster rate of 5% from 4.9%. Recently, the Bank of England had cautioned about inflation quickening next year (projecting a peak rate of 2.8% in Q3 2025), citing the impact of higher insurance contributions and rising minimum wages as outlined in the latest government budget. Therefore, with inflation rising above forecast, the bank will likely slow the pace of monetary easing after delivering two interest rate cuts of 25 bps earlier, with markets now seeing only two additional cuts by the end of 2025.

Eurozone: ECB warns of fiscal and growth risks in its latest Financial Stability Review [archived PDF]. In its most recent Financial Stability Review (November) [archived PDF], the European Central Bank warned that elevated debt and fiscal deficit levels and anemic long-term growth could expose sovereign debt vulnerabilities in the region, stoking concerns of a repeat of the 2011 sovereign debt crisis. Maturing debt being rolled over at much higher borrowing rates raising debt service costs poses risks to countries with little fiscal space and leaves certain governments exposed to market fluctuations. The bank also emphasized the risks of high equity valuations, low liquidity and a greater concentration of exposure among non-banks. Moreover, it sees current geopolitical uncertainties and the possibility of more trade tensions as heightening risks. The Eurozone’s current government debt-to-GDP ratio stands at 88%, but the underlying data suggest a much more precarious situation with Greece, Italy, and France’s ratios at 164%, 137% and 112%. Recently, concerns about France’s high fiscal deficit (around 5.9% of GDP) and elevated debt levels saw yields on the country’s bonds rise steeply, widening the spread gap with Germanbonds to the highest level in over a decade.

Disclaimer: While every care has been taken in preparing this publication, National Bank of Kuwait accepts no liability whatsoever for any direct or consequential losses arising from its use. Daily Economic Update is distributed on a complimentary and discretionary basis to NBK clients and associates. This report and previous issues can be found in the “News & Insight / Economic Reports” section of the National Bank of Kuwait’s web site. Please visit their web site, nbk.com, for other bank publications.

“Globalization” is here. Signified by an increasingly close economic interconnection that has led to profound political and social change worldwide, the process seems irreversible. In this book, however, Harold James provides a sobering historical perspective, exploring the circumstances in which the globally integrated world of an earlier era broke down under the pressure of unexpected events.

James examines one of the great historical nightmares of the twentieth century: the collapse of globalism in the Great Depression. Analyzing this collapse in terms of three main components of global economics—capital flows, trade and international migration—James argues that it was not simply a consequence of the strains of World War I, but resulted from the interplay of resentments against all these elements of mobility, as well as from the policies and institutions designed to assuage the threats of globalism.

Could it happen again? There are significant parallels today: highly integrated systems are inherently vulnerable to collapse, and world financial markets are vulnerable and unstable.

While James does not foresee another Great Depression, his book provides a cautionary tale in which institutions meant to save the world from the consequences of globalization—think WTO and IMF, in our own time—ended by destroying both prosperity and peace.

PresidentTrump’s speech here at the World Economic Forum went over relatively well. That’s partly because Davos is a conclave of business executives, and they like Trump’s pro-business message. But mostly, the president’s reception was a testament to the fact that he and what he represents are no longer unusual or exceptional. Look around the world and you will see: Trump and Trumpism have become normalized.

Davos was once the place where countries clamored to demonstrate their commitment to opening up their economies and societies. After all, these forces were producing global growth and lifting hundreds of millions out of poverty. Every year, a different nation would become the star of the forum, usually with a celebrated finance minister who was seen as the architect of a boom. The United States was the most energetic promoter of these twin ideas of economic openness and political freedom.

Today, Davos feels very different. Despite the fact that, throughout the world, growth remains solid and countries are moving ahead, the tenor of the times has changed. Where globalization was once the main topic, today it is the populist backlash to it. Where once there was a firm conviction about the way of the future, today there is uncertainty and unease.

This is not simply atmospherics and rhetoric. Ruchir Sharma of Morgan Stanley Investment Management points out that since 2008, we have entered a phase of “deglobalization.” Global trade, which rose almost uninterruptedly since the 1970s, has stagnated, while capital flows have fallen. Net migration flows from poor countries to rich ones have also dropped. In 2018, net migration to the United States hit its lowest point in a decade.

It’s important not to exaggerate the backlash to globalization.

As a 2019 report by DHL demonstrates, globalization is still strong and, by some measures, continues to expand. People still want to trade, travel and transact across the world. But in government policy, where economic logic once trumped politics, today it is often the reverse. EconomistNouriel Roubini argues that the cumulative result of all these measures — protecting local industries, subsidizing national champions, restricting immigration — is to sap growth. “It means slower growth, fewer jobs, less efficient economies,” he told me recently. We’ve seen it happen many times in the past, not least in India, which suffered decades of stagnation as a result of protectionist policies, and we will see the impact in years to come.

This phase of deglobalization is being steered from the top. The world’s leading nations are, as always, the agenda-setters. The example of China, which has shielded some of its markets and still grown rapidly, has made a deep impression on much of the world. Probably deeper still is the example of the planet’s greatest champion of liberty and openness, the United States, which now has a president who calls for managed trade, more limited immigration and protectionist measures. At Davos, Trump invited every nation to follow his example. More and more are complying.

Students should sense that while history does not repeat itself, it sometimes rhymes and this is a major danger. It also might imply that coping with climate change will be all the harder because American-led unilateralism everywhere would mean world policy paralysis.

In October, I wrote about the potential for standards to make business-to-business payments more efficient. Today, let’s talk about standards again, this time for money transfer businesses and the state regulations covering them.

For new and established money transfer businesses and for state regulators, the hodgepodge of state regulations creates headaches. To do business everywhere in the United States, money transfer businesses must register separately in each state and US territory and meet license requirements that can vary from state to state. They can face multiple state examinations, also with different requirements, simultaneously (and annually). During examinations, regulators review operations, financial condition, management, and compliance with anti-money laundering laws.

Fortunately, many states have acted to address this confusing and inefficient situation by adopting the Model Money Transmission Modernization Act (MTMA) [archived PDF], sample legislation developed by the Conference of State Bank Supervisors to establish nationwide standards and requirements for licensed money transmitters. Fourteen states have adopted some version of the MTMA: Arizona, Arkansas, Georgia, Hawaii, Indiana, Iowa, Minnesota, Nevada, New Hampshire, North Dakota, South Dakota, Tennessee, Texas, and West Virginia. In my home state of Massachusetts, the legislature’s Joint Committee on Financial Services heard testimony on a version of this bill just last month. For traditional money transmitters and new fintech entrants, the MTMA aims to reduce the substantive and technical differences among the various state laws and regulations. This kind of change has the potential to reduce compliance burdens, encourage innovation, and remove barriers to entry for new market participants.

The MTMA is important given the prodigious growth in person-to-person, or P2P, payments via apps. Among all USconsumers, half of P2P payments were sent using noncash methods in 2022, up from less than 30 percent in 2020 (see the chart). From Massachusetts alone, money transmitters sent $31 billion in 2022, according to the state’s Division of Banks.

Half of P2P payments were made electronically in 2022.

The MTMA also has the potential to create efficiencies for state supervisors. For example, the Conference of State Bank Supervisors (CSBS) has facilitated a collaborative exam program for nationwide payments and cryptocurrency firms to undergo one exam, each facilitated by one state overseeing a group of examiners sourced from across the country. According to the CSBS, transmitters in more than 40 states that have laws addressing core precepts can benefit from the streamlined exams.

The MTMA is another example showing that standards create efficiencies that are good for businesses, good for regulators and, by extension, good for consumers.

Complaint alleges company violated FTC Act and ROSCA with false promises targeting consumers living paycheck-to-paycheck and by failing to deliver cash advances as advertised

The Federal Trade Commission is taking action against personal financeapp provider Brigit, alleging that its promises of “instant” cash advances of up to $250 for people living paycheck-to-paycheck were deceptive and that the company locked consumers into a $9.99 monthly membership they couldn’t cancel.

Brigit, also known as Bridge It, Inc., has agreed to settle the FTC’s charges, resulting in a proposed court order that would require the company to pay $18 million in consumer refunds, stop its deceptive marketing promises, and end tactics that prevented customers from cancelling.

“Brigit trapped those consumers least able to afford it into monthly membership plans they struggled to escape from,” said Sam Levine, Director of the FTC’s Bureau of Consumer Protection. “Companies that offer cash advances and other alternative financial products have to play by the same rules as other businesses or face potential action by the FTC.”

The FTC’s complaint, however, charges that consumers were rarely able to get an advance for the promised $250, and in many cases, consumers were not able to receive a cash advance at all. Despite Brigit’s promises that advances would be available with “free instant transfers,” the complaint notes that the company began charging consumers a 99-cent fee for an instant transfer. Consumers who did not pay the fee had to wait up to three business days for their advances.

In addition, the complaint charges that while Brigit claimed to offer “non-recourse” advances with no fees or interest, the company prevented consumers who had an open advance from cancelling their subscription and continued to withdraw $9.99 monthly from their bank account until the advance was paid off. Such monthly charges created significant additional hardship for consumers already struggling to pay off a cash advance.

Even when consumers without an open cash advance attempted to cancel the paid subscription, the complaint charges that the company employed dark patterns—manipulative design tricks—to create a confusing and misleading cancellation process that prevented consumers from cancelling their subscriptions, instead of offering a simple mechanism to cancel, as required by the Restore Online Shoppers’ Confidence Act (ROSCA) [archived PDF].

The proposed settlement order [archived PDF], which must be approved by a federal judge before it can go into effect, would require Brigit to pay $18 million to the FTC to be used to provide refunds to consumers. In addition, the order would prohibit Brigit from misleading consumers about how much money is available through their advances, how fast the money would be available, any fees associated with delivery, and consumers’ ability to cancel their service. The order would also require the company to make clear disclosures about its subscription products and provide a simple mechanism for consumers to cancel.

“If you raise [the development of the BRI] to the strategic level, there are countries where … you will have to lose money and there are countries where you will be free to make money.”

How to respond to the growing political divide between China and the West marked by partial decoupling, security alliances, and the risk of sanctions, amongst other things, continues to be a major topic of discussion among China’s intellectual elite. As already evidenced in previous editions of this newsletter, opinions vary considerably. Those presented here so far have ranged from Da Wei (达巍) stressing the importance of preserving if not strengthening ties with the West and Shen Wei (沈伟) arguing in favor of reforming the WTO and building up a network of free trade agreements to Ye Hailin (叶海林) emphasizing the need for China to demonstrate its military might to demobilize U.S. allies and Lu Feng (路风) calling for self-reliance and greater assertiveness in the field of tech. A certain amount of overlap certainly exists among these perspectives but the differences are nonetheless striking.

Today’s edition of Sinification looks at a speech made last month by Yang Ping (杨平), head and editor-in-chief of the highly regarded Beijing Cultural Review (文化纵横, hereafter BCR). Yang is also director of the Longway Foundation (修远基金会) which publishes BCR. The foundation describes its publication as “the most influential magazine of intellectual thought and commentary in China” and sees itself as having a key role in helping shape the direction of intellectual debates in China (“议题的设置就是意识形态斗争成功的一半”). Indeed, BCR often republishes old articles at key junctures as so often highlighted by David Ownby’s wonderful Reading the China Dream.

The following are excerpts from an edited transcript of a speech by Yang made at an event hosted by Renmin University’s Chongyang Institute for Financial Studies, which was attended by China’s Vice-minister of foreign affairs Xie Feng (谢锋). In his speech, Yang advocates building a new international system led by countries in the Global South (which, of course, includes China) rather than the West. His ideas are not particularly novel but are nevertheless noteworthy in that they represent yet another viewpoint in the ongoing debate over how China should respond to the increasing tensions that characterize its relations with the U.S. and other Western countries. Next week, I will be sharing a somewhat longer piece that proposes a way of protecting China from the growing threat of Westernsanctions.

China must respond to this growing trend by building a “new type of international system” with other countries in the Global South.

BRI projects should be increasingly focused on achieving this goal and thus allow more room for loss-making endeavors.

Capitalist politics ≠ Capitalist economics

“Since 2022 and the Russo-Ukrainian conflict, our main focus and topic of discussion has been China’s construction of a new type of international system.

“We have witnessed two typical manifestations of the separation of politics and the economy and the impact of politics on the economy:

The first is the conflict between Russia and Ukraine. The sanctions imposed on Russia by the United States and the West have reached unthinkable, abominable [令人发指] and unimaginable proportions. Under established international rules, it was understood that such sanctions could not possibly occur, but now they have. These include the fracturing of the financial system, the expropriation and seizure of Russian private assets and the freezing of Russianforeign exchange reserves. These are all abominable and unimaginable forms of confrontation. At the same time, the Russo-Ukrainian conflict has led to serious disruptions in global food and energy systems and supply chains, with massive food ‘shortages’ and soaring food prices, particularly in developing countries. Sanctions and political repression [政治打压] have severely disrupted the [world’s] economic order.

The second is the conflict between the U.S. and China. Since the Trump era, the U.S. has been engaged in a trade war against China, mainly by raising tariffs. Basically, this was simply about balancing trade [with China] and used mainly economic means. But under Biden, it [has become] a war that mixes politics with economics. Biden’s strategy towards China can basically be summed up in just a few words: one, friend-shoring, [i.e.] only allowing friendly countries into [parts of] its supply chains; two, alliancepolitics, [i.e.] continuously forging an alliance system involving NATO, the European Union, Japan, AUKUS and the four Asia-Pacific countries [I assume he is referring to South Korea, Japan, New Zealand and Australia taking part for the first time in a NATO summit last year] and constantly opposing China [不断应对中国]; three, its so-called ‘precision strikes’, [i.e.] its radical crackdown on China’s high tech [industry], especially our chip industry.”

China is being pushed out of the U.S.-led international system

“The information I have seen so far is that the number of Chinese companies included in the U.S.’s ‘entity list’ has risen from 132 under Trump to over 530 now. The scope of such point-to-point [点对点] precision strikes is constantly expanding. With such a political impact on the economy, we can feel the [world’s] economic order being disrupted across the board. The world is moving inexorably in the direction of decoupling. The phenomenon of politics affecting the economy and the capitalistpolitical order no longer upholding the capitalisteconomic order are extremely striking.

“In such a context, the challenges now facing China are extremely serious and varied. We have the pressures of dealing both with containment in the Indo-Pacific and with the U.S.-led politics of alliances across the world. More importantly and fundamentally China faces the strategic task of building a new type of international system [新型国际体系] … The existing Western-dominated international system used to be one in which we tried hard to blend [so as] to become one with it. During this process, we [sought to] absorb the West’s advanced technologies and management [practices] and thus complete our mission of industrialisation and modernization.

“But once you enter the existing international system, he [who is already inside] does not want to play with you, and even wants to drive you back out. He wants to divide both supply chains and the economic system into two parts [搞成两套] and desperately wants to contain and suppress you. This is not something that can be determined by your own subjective preferences. He has made up his mind: you have already become his ‘fated opponent’ [命定的对手]. He has to suppress you and drive you out of the existing system.”

Building a new international system with the Global South

“It is at this point that China is faced with the task of constructing a new type of international system that is not dominated by the West. In today’s so-called strategic quadrangle consisting of the U.S., Europe, Russia and China, how to construct such an international system appears particularly difficult [逼庂 literally means ‘narrow’ or ‘cramped’ rather than ‘difficult’].

“But if we look a little further south, we will find a vast number of developing countries, the Third World and the countries of the global South. They should be our strategy’s depth [我们的战略纵深]. That is to say, [we should] build a new type of international relations and a new type of international system that has strategic depth and in which China and the countries of the global South are jointly integrated. [This] is, in my view, an important strategic task for China’s international relations in the coming decades.”

BRI projects: Strategy trumps profitability

“For China today, especially for businesses and governments at all levels [within China] that are currently working hard to develop BRI trade, there is a very important point to which they should be alerted or reminded about: the development of the BRI has to go beyond mere business, beyond the general export of [China’s excess] production capacity, beyond the partial thinking of industry and the partial thinking at the regional level, or the simple economic way of thinking of business. The development of the BRI should be considered at the strategic level. That is, it should be included into China’s strategy when thinking about Africa, South America, Southeast Asia and Central Asia.

“If you raise [the development of the BRI] to the strategic level, there are countries where you won’t be able to make money and will have to lose money, and there are countries where you will be free to make money. You have to unite the two within your organic strategy.

“The strategic task of building a new type of international system is, in my view, a strategic proposition that Chinesethink tanks and research institutes should pay very close attention to with regards to international relations.

“Time is limited today. I just wanted to make a start here. I hope to receive your corrections and criticisms. Thank you!”

The recessive importance of the Global South was previously explored by Richard and his partner Larry, with input from Supratik Bose, many decades ago as shown here.