by Iñaki Aldasoro, Jon Frost, Sang Hyuk Lim, Fernando Perez-Cruz & Hyun Song Shin

Key takeaways

Existing anti-money laundering (AML) approaches relying on trusted intermediaries have limited effectiveness with decentralized record-keeping in permissionless public blockchains.

The public transaction history on blockchains can enable AML and other compliance efforts, such as FX regulations, by leveraging the provenance and history of any particular unit or balance of a cryptoasset, including stablecoins.

An AML compliance score based on the likelihood that a particular cryptoasset unit or balance is linked with illicit activity may be referenced at points of contact with the banking system (“off-ramps”), preventing inflows of the proceeds of illicit activity and supporting a culture of “duty of care” among crypto market participants.

by Emanuel Kohlscheen, Phurichai Rungcharoenkitkul, Dora Xia & Fabrizio Zampolli

Key takeaways

Tariffs affect economies most directly through trade volume and prices. Tariffs lower output growth everywhere, though the magnitude varies by country and scenario. They also tend to raise inflation, most notably in the imposing countries.

Therefore, the behavior and the volatility of different asset classes have been impacted, altering global financial conditions. This scenario requires particular caution from emerging market economies amid heightened geopolitical tensions.

Regarding the domestic scenario, the set of indicators on economic activity has shown some moderation in growth, as expected, but the labor market is still showing strength.

The inflation outlook remains challenging in several dimensions. Copom assessed the international scenario, economic activity, aggregate demand, inflation expectations, and current inflation. Copom then discussed inflation projections and expectations before deliberating on the current decision and future communication.

The global environment is more adverse and uncertain. If, on the one hand, the approval of certain trade agreements, along with recent inflation and economic activity data from the U.S., could suggest a reduction in global uncertainty, on the other hand, the U.S. fiscal policy—and, particularly for Brazil, the U.S. trade policy—make the outlook more uncertain and adverse. The increase of tradetariffs by the U.S. to Brazil has significant sectoral impacts and still uncertain aggregate effects that depend on the unfolding of the next steps in the negotiations and the perception of risk inherent to this process. The Committee is closely monitoring the potential impacts on the real economy and financial assets. The prevailing assessment within the Committee is the increased global outlook uncertainty, and, therefore, Copom should maintain a cautious stance. As usual, the Committee will focus on the transmission mechanisms from the external environment to the domestic inflation dynamics and their impact on the outlook.

The domestic economic activity outlook has indicated a certain moderation in growth, while also presenting mixed data across sectors and indicators.

Overall, some moderation in growth is observed, supporting the scenario outlined by the Committee. This moderation, necessary for the widening of the output gap and the convergence of inflation to the target, is aligned with a contractionary monetary policy. Monthly sectoral surveys and more timely consumption data support a gradual slowdown in growth.

The credit market, which is more sensitive to financial conditions, has shown clearer moderation. A decline in non-earmarkedcredit granting and an increase in interest and delinquency rates have been observed. Moreover, regarding householdcredit, there has been an increase in the household debt–service ratio and a deepening of the negative credit flow—that is, households repaying more debt than taking on. It was emphasized during the discussion that some recent measures, such as private payroll-deducted loans, have had less impact than many market participants expected. Given the implementation agenda in this credit line, as well as the effects of introducing and removing taxes on other credit modalities, the Committee believes it should closely monitor upcoming credit data releases.

Fiscal policy has a short-term impact, mainly through stimulating aggregate demand, and a more structural dimension, which has the potential to affect perceptions of debt sustainability and influence the term premium in the yield curve. A fiscal policy that acts counter-cyclically and contributes to reducing the risk premium favors the convergence of inflation to the target. Copom reinforced its view that the slowdown in structural reform efforts and fiscal discipline, the increase in earmarkedcredit, and uncertainties over the public debt stabilization have the potential to raise the economy’s neutral interest rate, with deleterious impacts on the power of monetary policy and, consequently, on the cost of disinflation in terms of activity. The Committee remained firmly convinced that policies must be predictable, credible, and countercyclical. In particular, the Committee’s discussion once again highlighted the need for harmonious fiscal and monetary policy.

Inflation expectations, as measured by different instruments and obtained from various groups of agents, remained above the inflation target at all horizons, maintaining the adverse inflation outlook. For shorter-term horizons, following the release of the most recent data, there has been a decline in inflation expectations. For longer-term horizons, conversely, there has been no significant change in inflation expectations between Copom meetings, even though measures of breakeven inflation extracted from financial assets have declined. The Committee reaffirmed and renewed its commitment to re-anchoring expectations and to conducting a monetary policy that supports such a movement.

De-anchored inflation expectations is a factor of discomfort shared by all Committee members and must be tamed. Copom highlighted that environments with de-anchored expectations increase the disinflation cost in terms of activity. The scenario of inflation convergence to the target becomes more challenging with de-anchored expectations for longer horizons. When discussing this topic, the main conclusion obtained and shared by all members of Copom was that, in an environment of de-anchored expectations—as currently is the case—greater monetary restriction is required for a longer period than would be otherwise appropriate.

The inflation scenario has continued to show downside surprises in recent periods compared with analysts’ forecasts, but inflation has remained above the target Industrial goods inflation, which has already been showing weaker wholesale price pressures, continued to ease in the more recent period. Food prices also displayed slightly weaker-than-expected dynamics. Finally, servicesinflation, which has greater inertia, remains above the level required to meet the inflation target, in a context of a positive output gap. Beyond the changes in items, or even short-term oscillations, the core inflation measures have remained above the value consistent with the target achievement for months, corroborating the interpretation that inflation is pressured by demand and requires a contractionary monetary policy for a very prolonged period.

Copom then addressed the projections. In the reference scenario, the interest rate path is extracted from the Focus survey, and the exchange rate starts at USD/BRL 5.552 and evolves according to the purchasing power parity (PPP). The Committee assumes that oil prices follow approximately the futures market curve for the following six months and then start increasing 2% per year onwards. Moreover, the energy tariff flag is assumed to be “green” in December of the years 2025 and 2026.

In the reference scenario, four-quarter inflation projections for 2025 and for 2026 are 4.9% and 3.6%, respectively (Table 1). For the relevant horizon for monetary policy—2027 Q1—the inflation projection based on the reference scenario extracted from the Focus survey remained at 3.4%, above the inflation target.

Regarding the balance of risks, it was assessed that the scenario of greater uncertainty continues to present higher-than-usual upside and downside inflation risks to the inflation outlook. Copom assessed that, among the upside risks for the inflation outlook and inflation expectations, it should be emphasized (i) a more prolonged period of de-anchoring of inflation expectations; (ii) a stronger-than-expected resilience of servicesinflation due to a more positive output gap; and (iii) a conjunction of internal and external economic policies with a stronger-than-expected inflationary impact, for example, through a persistently more depreciatedcurrency. Among the downside risks, it should be noted (i) a greater-than-projected deceleration of domestic economic activity, impacting the inflation scenario; (ii) a steeper global slowdown stemming from the trade shock and the scenario of heightened uncertainty; and (iii) a reduction in commodity prices with disinflationary effects.

Prospectively, the Committee will continue monitoring the pace of economic activity, which is a fundamental driver of inflation, particularly services inflation; the exchange rate pass-through to inflation, after a process of increased exchange rate volatility; and inflation expectations, which remain de-anchored and are drivers of future inflation behavior. It was emphasized that inflationary vectors remain adverse, such as the economic activity resilience and labor market pressures, de-anchored inflation expectations, and high inflation projections. This scenario prescribes a significantly contractionary monetary policy for a very prolonged period to ensure the convergence of inflation to the target.

Copom then discussed the conduct of monetary policy, considering the set of projections evaluated, as well as the balance of risks for prospective inflation.

Following a swift and firm interest rate hike cycle, the Committee anticipates, as its monetary policy strategy, continuity of the interruption of the rate hiking cycle to observe the effects of the cycle already implemented. It was emphasized that, once the appropriate interest rate is determined, it should remain at a significantly contractionary level for a very prolonged period due to de-anchored expectations. The Committee emphasizes that it will remain vigilant, that future monetary policy steps can be adjusted and that it will not hesitate to proceed with the rate hiking cycle if appropriate.

The Committee has been closely monitoring with particular attention the announcements regarding the imposition by the U.S. of tradetariffs on Brazil, reinforcing its cautious stance in a scenario of heightened uncertainty. Moreover, it continues to monitor how the developments on the fiscal side impact monetary policy and financial assets. The current scenario continues to be marked by de-anchored inflation expectations, high inflation projections, resilience on economic activity, and labor market pressures. Ensuring the convergence of inflation to the target in an environment with de-anchored expectations requires a significantly contractionary monetary policy for a very prolonged period.

Copom decided to maintain the Selic rate at 15.00% p.a., and judges that this decision is consistent with the strategy for inflation convergence to a level around its target throughout the relevant horizon for monetary policy. Without compromising its fundamental objective of ensuring price stability, this decision also implies smoothing economic fluctuations and fostering full employment.

The current scenario, marked by heightened uncertainty, requires a cautious stance in monetary policy. If the expected scenario materializes, the Committee foresees a continuation of the interruption of the rate hiking cycle to examine its yet-to-be-seen cumulative impacts, and then evaluate whether the current interest rate level, assuming it stable for a very prolonged period, will be enough to ensure the convergence of inflation to the target. The Committee emphasizes that it will remain vigilant, that future monetary policy steps can be adjusted and that it will not hesitate to resume the rate hiking cycle if appropriate.

The following members of the Committee voted for this decision: Gabriel Muricca Galípolo (Governor), Ailton de Aquino Santos, Diogo Abry Guillen, Gilneu Francisco Astolfi Vivan, Izabela Moreira Correa, Nilton José Schneider David, Paulo Picchetti, Renato Dias de Brito Gomes, and Rodrigo Alves Teixeira.

Table 1

Inflation projections in the reference scenario Year-over-year IPCA change (%)

1 Unless explicitly stated otherwise, this update considers changes since the June Copom meeting (271st meeting).

2 It corresponds to the rounded value of the average exchange rate observed over the ten working days ending on the last day of the week prior to the Copom meeting, according to the procedure adopted since the 258th meeting.

Meeting information

Date: July 29-30 2025

Place: BCB Headquarters’ meeting rooms on the 8th floor (7/29 and 7/30 on the morning) and 20th floor (7/30 on the afternoon) – Brasilia – DF – Brazil

Starting and ending times:

July 29: 10:07 AM – 11:37 AM; 2:17 PM – 5:51 PM

July 30: 10:10 AM – 11:13 AM; 2:37PM – 6:34 PM

In attendance:

Members of the Copom

Gabriel Muricca Galípolo – Governor

Ailton de Aquino Santos

Diogo Abry Guillen

Gilneu Francisco Astolfi Vivan

Izabela Moreira Correa

Nilton José Schneider David

Paulo Picchetti

Renato Dias de Brito Gomes

Rodrigo Alves Teixeira

Department Heads in charge of technical presentations (attending on July 29 and on the morning of July 30)

André de Oliveira Amante

Open Market Operations Department

Euler Pereira Gonçalves de Mello

Research Department (also attending on the afternoon of 7/30)

Fábio Martins Trajano de Arruda

Department of Banking Operations and Payments System

Luís Guilherme Siciliano Pontes

International Reserves Department

Marcelo Antonio Thomaz de Aragão

Department of International Affairs

Ricardo Sabbadini

Department of Economics

Other participants (attending on July 29 and on the morning of July 30)

Alexandre de Carvalho

Office of Economic Advisor

André Maurício Trindade da Rocha

Head of the Financial System Monitoring Department

Angelo Jose Mont Alverne Duarte

Head of Office of the Deputy Governor for Licensing and Resolution (attending on the mornings of 7/29 and 7/30)

Arnaldo José Giongo Galvão

Press Office Advisor

Cristiano de Oliveira Lopes Cozer

General Counsel

Edson Broxado de França Teixeira

Head of Office of the Deputy Governor for Supervision

Eduardo José Araújo Lima

Head of Office of the Deputy Governor for Economic Policy

Fernando Alberto G. Sampaio C. Rocha

Head of the Department of Statistics

Isabela Ribeiro Damaso Maia

Head of the Sustainability and International Portfolio Investors Unit (attending on the mornings of 7/29 and 7/30)

Julio Cesar Costa Pinto

Head of Office of the Governor

Laura Soledad Cutruffo Comparini

Deputy Head of the Department of Economics

Leonardo Martins Nogueira

Head of Office of the Deputy Governor for Monetary Policy

Marcos Ribeiro de Castro

Deputy Head of the Research Department

Mardilson Fernandes Queiroz

Head of the Financial System Regulation Department

Olavo Lins Romano Pereira

Deputy Head of the Department of International Affairs

Renata Modesto Barreto

Deputy Head of the Department of Banking Operations and Payments System

Ricardo da Costa Martinelli

Deputy Head of the International Reserves Department

Ricardo Eyer Harris

Head of Office of the Deputy Governor for Regulation

Ricardo Franco Moura

Head of the Prudential and Foreign Exchange Regulation Department

Rogerio Antonio Lucca

Executive Secretary

Simone Miranda Burello

Advisor in the Office of the Deputy Governor for Monetary Policy

Inflation expectations for 2025 and 2026 collected by the Focus survey remained above the inflation target and stand at 5.1% and 4.4%, respectively. Copom’s inflation projections for the first quarter of 2027, currently the relevant horizon for monetary policy, stand at 3.4% in the reference scenario (Table 1).

The risks to the inflation scenarios, both to the upside and to the downside, continue to be higher than usual. Among the upside risks for the inflation outlook and inflation expectations, it should be emphasized (i) a more prolonged period of de-anchoring of inflation expectations; (ii) a stronger-than-expected resilience of services inflation due to a more positive output gap; and (iii) a conjunction of internal and external economic policies with a stronger-than-expected inflationary impact, for example, through a persistently more depreciatedcurrency. Among the downside risks, it should be noted (i) a greater-than-projected deceleration of domestic economic activity, impacting the inflation scenario; (ii) a steeper global slowdown stemming from the trade shock and the scenario of heightened uncertainty; and (iii) a reduction in commodity prices with disinflationary effects.

The Committee has been closely monitoring the announcements on tariffs by the USA to Brazil, which reinforces its cautious stance in a scenario of heightened uncertainty. Moreover, it continues to monitor how the developments on the fiscal side impact monetary policy and financial assets. The current scenario continues to be marked by de-anchored inflation expectations, high inflation projections, resilience on economic activity and labormarket pressures. Ensuring the convergence of inflation to the target in an environment with de-anchored expectations requires a significantly contractionary monetary policy for a very prolonged period.

Copom decided to maintain the Selic rate at 15.00% p.a., and judges that this decision is consistent with the strategy for inflation convergence to a level around its target throughout the relevant horizon for monetary policy. Without compromising its fundamental objective of ensuring price stability, this decision also implies smoothing economic fluctuations and fostering full employment.

The current scenario, marked by heightened uncertainty, requires a cautious stance in monetary policy. If the expected scenario materializes, the Committee foresees a continuation of the interruption of the rate hiking cycle to examine its yet-to-be-seen cumulative impacts, and then evaluate whether the current interest rate level, assuming it stable for a very prolonged period, will be enough to ensure the convergence of inflation to the target. The Committee emphasizes that it will remain vigilant, that future monetary policy steps can be adjusted and that it will not hesitate to resume the rate hiking cycle if appropriate.

The following members of the Committee voted for this decision: Gabriel Muricca Galípolo (Governor), Ailton de Aquino Santos, Diogo Abry Guillen, Gilneu Francisco Astolfi Vivan, Izabela Moreira Correa, Nilton José Schneider David, Paulo Picchetti, Renato Dias de Brito Gomes, and Rodrigo Alves Teixeira.

Table 1

Inflation projections in the reference scenario Year-over-year IPCA change (%)

In the reference scenario, the interest rate path is extracted from the Focus survey, and the exchange rate starts at USD/BRL 5.55 and evolves according to the purchasing power parity (PPP). The Committee assumes that oil prices follow approximately the futures market curve for the following six months and then start increasing 2% per year onwards. Moreover, the energy tariff flag is assumed to be “green” in December of the years 2025 and 2026. The value for the exchange rate was obtained according to the usual procedure.

Note: This press release represents the Copom’s best effort to provide an English version of its policy statement. In case of any inconsistency, the original version in Portuguese prevails.

[from the International Monetary Fund, by Patrick A. Imam, Kangni R Kpodar, Djoulassi K. Oloufade, Vigninou Gammadigbe]

This paper delves into the intricate relationship between uncertainty and remittance flows. The prevailing focus has been on tangible risk factors like exchange rate volatility and economic downturn, overshadowing the potential impact of uncertainty on remittance dynamics. Leveraging a new dataset of quarterly remittances combined with uncertainty indicators across 77 developing countries from 1999 Q1 to 2019 Q4, the analysis highlights that uncertainty in remittance-sending countries negatively affects remittance flows. In contrast, uncertainty in remittance receiving-countries has a more complex, dual effect. In countries with high private investment ratios, rising domestic uncertainty leads to a decline in remittances. Conversely, in countries with low public spending on education and health, remittances increase in response to uncertainty, serving as a social safety net. The paper underscores the heterogeneous and non-linear effects of domestic uncertainty on remittance flows.

[from NBK Group’s Economic Research Department, 21 November, 2024]

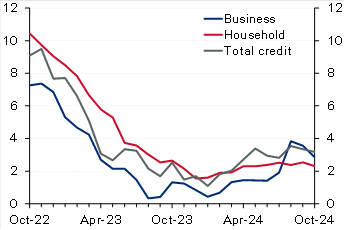

Kuwait: Solid credit growth in October driven by household credit. Domestic credit increased by a solid 0.4% in October, driving up YTD growth to 2.9% (3.2% y/y). The recovery in household credit continued, with growth in October at a solid 0.5%, resulting in a YTD increase of 2.4%. While y/y growth in household credit remains a limited 2.3%, annualized growth over the past four months is a stronger 4.7%. Businesscredit inched up by 0.2% in October, pushing YTD growth to 3.6% (2.9% y/y). Industry and trade drove businesscredit growth in October while construction and trade are the fastest growing YTD at 17% and 8%, respectively. In contrast, the oil/gas sector continued its downtrend, deepening the YTD decrease to 13%. Excluding the oil/gas sector, growth in business credit would increase to a relatively good 5% YTD. Looking ahead, the last couple of months of the year (especially December) are usually the weakest for businesscredit, likely due to increased repayments and write-offs, but it will not be surprising if the recovery in household credit is generally sustained, especially given the commencement of the interest rate-cutting cycle. Meanwhile, driven by a plunge in the volatile public-institution deposits, resident deposits decreased in October, resulting in YTD growth of 2.4% (4.2% y/y). Private-sectordeposits inched up in October driving up YTD growth to 4.5% compared with 10% for government deposits while public-institution deposits are a big drag (-14%). Within private-sector KD deposits, CASA showed further signs of stabilization as there was no decrease for the third straight month while the YTDdrawdown is a limited 1%.

Chart 1: Kuwait credit growth

(% y/y)

Source: Central Bank of Kuwait (CBK)

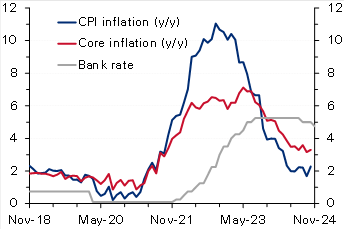

Chart 2: UK inflation

(%)

Source: Haver

Egypt: IMF concludes mission for fourth review, sees external risks. The IMF concluded its visit to Egypt after spending close to 2 weeks, holding several in-person meetings with the Egyptian authorities, private sector, and other stakeholders. The IMF released a statement mentioning that the current ongoing geopolitical tensions in the region in addition to an increasing number of refugees have affected the external sector (Suez Canal receipts down by 70%) and put severe pressure on the fiscal front. The Fund acknowledged the Central Bank of Egypt’s commitment to unify the exchange rate, maintain the flexible exchange rate regime, and keep inflation on a firm downward trend over the medium term by substantially tightening monetary policy. It also highlighted that continued policy discipline was also a key to containing fiscal risks, especially those related to the energy sector. The Fund, as always, re-iterated the need for promoting the private sector mainly through an enhanced tax system and accelerating divestment plans of the state firms. Finally, it also said that the discussions would continue over the coming days to finalize the agreement on the remaining policies and reform plans. However, the release did not provide any clear hints about the conclusion on the government’s earlier request to push the timeline of some of the subsidy moves.

Oman: IMF completes article IV with a strong outlook for the economy in 2025. Oman’s economy continued to expand with growth reaching 1.9% in the first half of 2024 (versus 1.2% in 2023), despite being weighed down by OPEC+ mandated oil production cuts as non-oil GDP grew a stronger 3.8% y/y in H1 (versus 1.8% in 2023). The fiscal and current account balances remain in a comfortable situation evident by a decline in public sectordebt and the recent rating upgrade to investment grade. The Fund expects Oman’s economic growth to see a strong rebound in 2025, supported by higher oil production. It also believes that fiscal and current account balances will remain in surplus but at lower levels. Key risks to the outlook stem from oil price volatility and intensifying geopolitical tensions. The IMF also mentioned that further efforts are needed to raise nonhydrocarbon revenues through more tax policy measures and the phasing out of untargeted subsidies which should help in freeing up resources to finance growth under the government’s diversification agenda.

UK: Inflation rises more than forecast, reinforcing BoE’s caution on rate cuts. UKCPIinflation increased to 2.3% y/y in October from 1.7% the previous month, slightly above the market and the Bank of England’s forecast of 2.2%. On a monthly basis too, inflation rose to 0.6%, a seven-month high, from September’s no change. The steep rise was mainly driven by an almost 10% rise in the household energy price cap effective from October. Core inflation also accelerated to 3.3% y/y (0.4% m/m) from 3.2% (0.1% m/m). While goods prices continued to fall (-0.3% y/y), service prices rose at a faster rate of 5% from 4.9%. Recently, the Bank of England had cautioned about inflation quickening next year (projecting a peak rate of 2.8% in Q3 2025), citing the impact of higher insurance contributions and rising minimum wages as outlined in the latest government budget. Therefore, with inflation rising above forecast, the bank will likely slow the pace of monetary easing after delivering two interest rate cuts of 25 bps earlier, with markets now seeing only two additional cuts by the end of 2025.

Eurozone: ECB warns of fiscal and growth risks in its latest Financial Stability Review [archived PDF]. In its most recent Financial Stability Review (November) [archived PDF], the European Central Bank warned that elevated debt and fiscal deficit levels and anemic long-term growth could expose sovereign debt vulnerabilities in the region, stoking concerns of a repeat of the 2011 sovereign debt crisis. Maturing debt being rolled over at much higher borrowing rates raising debt service costs poses risks to countries with little fiscal space and leaves certain governments exposed to market fluctuations. The bank also emphasized the risks of high equity valuations, low liquidity and a greater concentration of exposure among non-banks. Moreover, it sees current geopolitical uncertainties and the possibility of more trade tensions as heightening risks. The Eurozone’s current government debt-to-GDP ratio stands at 88%, but the underlying data suggest a much more precarious situation with Greece, Italy, and France’s ratios at 164%, 137% and 112%. Recently, concerns about France’s high fiscal deficit (around 5.9% of GDP) and elevated debt levels saw yields on the country’s bonds rise steeply, widening the spread gap with Germanbonds to the highest level in over a decade.

Disclaimer: While every care has been taken in preparing this publication, National Bank of Kuwait accepts no liability whatsoever for any direct or consequential losses arising from its use. Daily Economic Update is distributed on a complimentary and discretionary basis to NBK clients and associates. This report and previous issues can be found in the “News & Insight / Economic Reports” section of the National Bank of Kuwait’s web site. Please visit their web site, nbk.com, for other bank publications.

“One of our most brilliant evolutionary biologists, Richard Lewontin has also been a leading critic of those—scientists and non-scientists alike—who would misuse the science to which he has contributed so much. In The Triple Helix, Lewontin the scientist and Lewontin the critic come together to provide a concise, accessible account of what his work has taught him about biology and about its relevance to human affairs. In the process, he exposes some of the common and troubling misconceptions that misdirect and stall our understanding of biology and evolution.

The central message of this book is that we will never fully understand living things if we continue to think of genes, organisms, and environments as separate entities, each with its distinct role to play in the history and operation of organic processes. Here Lewontin shows that an organism is a unique consequence of both genes and environment, of both internal and external features. Rejecting the notion that genes determine the organism, which then adapts to the environment, he explains that organisms, influenced in their development by their circumstances, in turn create, modify, and choose the environment in which they live.

The Triple Helix is vintage Lewontin: brilliant, eloquent, passionate and deeply critical. But it is neither a manifesto for a radical new methodology nor a brief for a new theory. It is instead a primer on the complexity of biological processes, a reminder to all of us that living things are never as simple as they may seem.”

Borrow from Lewontin the idea of a “triple helix” and apply it to the ultimate wide-angle view of this process of understanding. The educational triple helix includes and always tries to coordinate:

The student and their life (i.e., every student is first of all a person who is playing the role of a student). Every person is born, lives, and dies.

The student and their field are related to the rest of the campus. (William James: all knowledge is relational.)

The student keeps the triple helix “running” in the back of the mind and tries to create a “notebook of composite sketches” of the world and its workings and oneself and this develops through a life as a kind of portable “homemade” university which stays alive and current and vibrant long after one has forgotten the mean value theorem and the names and sequence for the six wives of Henry VIII).

We argue here in this proposal for an educational remedy that two dimensions of understanding must be added to “retro-fit” education.

In the first addition, call it pre-understanding, a student is given an overview not only of the field but of his or her life as well as the “techno-commercial” environment that characterizes the globe.

Pre-understanding includes such “overall cautions” offered to you by Calderón de la Barca’s 17th century classic Spanish play, Life is a Dream (Spanish: La vida es sueño). A student would perhaps ask: “what would it be like if I faced this “dreamlike quality” of life, as shown by the Spanish play, and suddenly realized that a life of “perfect myopia” is not what I want.

Hannah Arendt warns similarly of a life “like a leaf in the whirlwind of time.”

Again, I, the student ask: do I want such a Hannah Arendt-type leaf-in-the-whirlwind-like life, buried further under Calderón de la Barca’s “dream state”?

But that’s not all: while I’m learning about these “life dangers,” all around me from my block to the whole world, humanity does its “techno-commerce” via container ships and robots, hundreds of millions of vehicles and smartphones, multilateral exchange rates, and tariff policies. Real understanding has one eye on the personal and the other on the impersonal and not one or the other.

All of these personal and impersonal layers of the full truth must be faced and followed, “en face,” as they say in French (i.e., “without blinking”).

Call all this pre-understanding which includes of course a sense of how my “field” or major or concentration fits into the “architecture of knowledge” and not in isolation without connections or a “ramification structure.”

Post-understanding comes from the other end: my lifelong effort, after just about all that I learned about the six wives of King Henry VIII and the “mean value theorem”/Rolle’s theorem in freshman math, have been completely forgotten and have utterly evaporated in my mind, to re-understand my life and times and book-learning.

Pre-and post-understanding together allows the Wittgenstein phenomenon of “light falls gradually over the whole.”

Without these deeper dimensions of educational remedy, the student as a person would mostly stumble from “pillar to post” with “perfect myopia.” Education mostly adds to all the “fragmentariness” of the modern world and is in that sense, incomplete or even disorienting.

Education in this deep sense is supposed to be the antidote to this overall sense of modern “shapelessness,” to use Kierkegaard’s term.

History is “forever new” and we keep asking “what’s new?” but the past is “forever suggestive” and so we inquire here as to whether the past gives us interesting echoes of the more recent.

Specifically, we juxtapose the “closing of the gold window” in August 1971 (Nixon) and the British gold standard gyrations between 1925 and 1931, when England left gold (i.e., September 1931).

At the time, under Nixon, the U.S. also had an unemployment rate of 6.1% (August 1971) and an inflation rate of 5.84% (1971).

On the afternoon of Friday, August 13, 1971, these officials along with twelve other high-ranking White House and Treasury advisors met secretly with Nixon at Camp David. There was great debate about what Nixon should do, but ultimately Nixon, relying heavily on the advice of the self-confident Connally, decided to break up Bretton Woods by announcing the following actions on August 15:

Nixon directed Treasury SecretaryConnally to suspend, with certain exceptions, the convertibility of the dollar into gold or other reserve assets, ordering the gold window to be closed such that foreign governments could no longer exchange their dollars for gold.

An importsurcharge of 10 percent was set to ensure that American products would not be at a disadvantage because of the expected fluctuation in exchange rates.

Speaking on television on Sunday, August 15, when American financial markets were closed, Nixon said the following:

“The third indispensable element in building the new prosperity is closely related to creating new jobs and halting inflation. We must protect the position of the American dollar as a pillar of monetary stability around the world.

“In the past 7 years, there has been an average of one international monetary crisis every year …

“I have directed Secretary Connally to suspend temporarily the convertibility of the dollar into gold or other reserve assets, except in amounts and conditions determined to be in the interest of monetary stability and in the best interests of the United States.

“Now, what is this action—which is very technical—what does it mean for you?

“Let me lay to rest the bugaboo of what is called devaluation.

“If you want to buy a foreign car or take a trip abroad, market conditions may cause your dollar to buy slightly less. But if you are among the overwhelming majority of Americans who buy American-made products in America, your dollar will be worth just as much tomorrow as it is today.

“The effect of this action, in other words, will be to stabilize the dollar.”

Britain’s own experience in the twenties is explained like this:

“In 1925, Britain had returned to the gold standard.

(editor: This Churchill decision was deeply critiqued by Keynes.)

“When Labour came to power in May 1929 this was in good time for Black Friday on Wall Street in the following October.

“After the Austrian and German crashes in May and July 1931, Britain’s financial position became critical, and on 21st September she abandoned the gold standard.

(Europe of the Dictators, Elizabeth Wiskemann, Fontana/Collins, 1977, page 92-93)

Nixon’s policies gave us the demise of Bretton Woods, while the economic gyrations of 1925-1931 were part of the lead-up to World War II.

The setting is both “infinitely different” across the decades but the feeling of “flying blind” applies to both cases: U.S.A. “closing the gold window,” August 1971 and Britain’s overturning Churchill’s 1925 return to the gold standard, by 1931. One gets the sense of “concealed turmoil” and a lot of “winging it” in both cases. Policy-makers disagreed and they all saw the world of their moments “through a glass, darkly.”