This gives us the theme of anxiety over national destiny and trajectory, which currently preoccupies the American mind.

In the second book, this antagonism question involves real and imaginary threats, and all of these anxieties and antagonisms are related. The masterpiece series, Downton Abbey, depicts a scene that takes place in the garden, where the Lord announces that they are at war with Germany, and his audience is perplexed, thinking, “How can we be at war? Germany is our biggest trading partner.” This teaches us that wars and the antagonisms that precede them are not solely based on rational factors like trade volumes.

Let us turn our attention to China. We are all aware, however vaguely, of the Chinese Exclusion Act of 1882. In the recent PBS television series, American Masters, the episode “Tyrus” (season 31, episode 7, aired September 8, 2017) has the artist Tyrus Wong recounting the story of his father, with whom he immigrated to California in 1920 at the age of 9. It is hard for us to believe that, as people of Chinese descent, they were forbidden from owning property outside of Chinatown. He describes his struggle with the hassles of overt racism. He did not gain his American citizenship until 1946, after the act was repealed. He came to fame with Disney’s Bambi, where he was the film’s lead artist.

“…But all the people who live in the little shipping and trading towns along the coast are immigrants from far away, who care little about the Kashubian hinterland because there’s nothing there for them, their concerns are elsewhere. What concerns them is where their trade is, and since they trade with the whole world and are in communication with the whole world, you find people among them from all corners of the globe. Which goes for Kessin too, backwater though it is.”

“But this is delightful, Geert. You keep calling it a backwater, but now, if you haven’t been exaggerating, I find that it’s a completely new world. All sorts of exotic things. Isn’t that right? That’s what you meant, isn’t it?”

He nodded.

“A whole world, I say, with perhaps a Negro or a Turk, or perhaps even a Chinaman.”

“A Chinaman too. What a good guess. We may still have one, we certainly did have; he’s dead now, buried in a little plot with a railing round it next to the churchyard. If you’re not afraid I’ll show you his grave sometime. It’s in the dunes with just some marram grass round it and a little immortelle here and there, and the sound of the sea all the time. It’s very beautiful and very eerie.”

“Yes, eerie — I would like to know more about it. Or maybe rather not, I invariably start imagining things and then I have dreams, and I don’t want to see a Chinaman approaching my bed tonight when I hope I’ll be sleeping soundly.”

“Well, he won’t.”

“Well, he won’t. Listen to that. How odd it sounds, as if it were somehow possible. You’re trying to make Kessin interesting for me, but you’re rather overdoing it. Are there many foreigners like that in Kessin?”

“A great many. The whole town consists of foreigners like that, people whose parents or grandparents lived somewhere else altogether.”

“How very peculiar. Tell me more, please. But nothing sinister. A Chinaman, I think, is always a bit sinister.”

Notice the quote, “…I don’t want to see a Chinaman approaching my bed tonight when I hope I’ll be sleeping soundly.” This character echoes similar sentiments several more times above.

This “othering” of the Chinese in the novel continues:

Innstetten laughed. “We’re seventy miles further north than Hohen-Cremmen here and you have to wait a while for the first polar bear. I think you’re feeling the strain of the long journey, what with the St. Privat panorama and the story of the Chinaman and everything?”

“You didn’t tell me any story.”

“No, I just referred to him. But the mere mention of a Chinaman is a story in itself…”

“Oh, some nonsense: an old ship’s captain with a granddaughter or a niece who disappeared one fine day, and then a Chinaman, who may have been her lover, and in the hallway there was a little shark and a crocodile, both suspended on strings and always in motion. Makes a marvellous story, but not now. There are all kinds of other things flitting through my mind.”

All of this global antagonism-watching and paranoia is disconcertingly related to our current situation. Donald Trump and the Republicans are essentially entrepreneurs of hatred. As is widely misattributed to Mark Twain, “history doesn’t repeat itself, but it often rhymes.”

At the same time, economists have been documenting the loss of work opportunities and earning power by workers without college degrees as manufacturingemployment has declined. In 2013, David Autor, David Dorn, and Gordon Hanson published a study that estimated the labor market impacts resulting from increased trade competition following China’s entrance into the World Trade Organization, an effect often referred to as the “China shock.” Dozens of studies have since used the regional variation in job and income losses caused by the China shock to measure the adverse impacts of job displacement on family structures, crime, health, and other social indicators. Some supporters of industrial subsidies and higher tariffs have expressed the hope that these dynamics can be put into reverse.

The newspaper as an institution came into the service of commerce at an astonishingly late date.

The newspaper, as an institution, is not a product of capitalism. It brought together in the first place political news and then mainly all sorts of curiosities from the world at large. The advertisement, however, made its way into the newspaper very late. It was never entirely absent but originally it related to family announcements, while the advertisement as a notice by the merchant, directed toward finding a market, first becomes an established phenomenon at the end of the 18th century—in the journal which for a century was the first in the world, the “Times.” Official price bulletins did not become general until the 19th century; originally all the exchanges were closed clubs, as they have remained in America virtually down to the present. Hence in the 18th century, business depended on the organized exchange of letters. Rational trading between regions was impossible without secure transmission of letters. This was accomplished partly by the merchant guilds and in part by butchers, wheelwrights, etc. The final stage in the rationalization of transmission of letters was brought about by the post, which collected letters and in connection therewith made tariff agreements with commercial houses. In Germany, the family of Thurn and Taxis, who held the postal concession, made notable advances in the rationalization of communication by letter. Yet the volume of correspondence is in the beginning surprisingly small. In 1633, a million letters were posted in all England while today a place of 4,000 population will equal the number.

The first half of the nineteenth century witnessed the rapid rise to power of the periodical press. Journalism had been active — though dangerous to those engaged in it — during the Revolutionary period. Napoleon had kept the press under his thumb, as Giroudeau points out on page 235. The ‘freedom’ of the press was one of the most controversial issues both under the Restoration and the July Monarchy. Under Louis XVIII and Charles X the struggle between those who, like the Liberals and Bonapartists, wanted to keep the Revolutionary principles and gains intact, and the Conservatives of various hues, especially the ‘Ultras’, who wanted to put the political clock back, was an affair of major importance; likewise, under Louis-Philippe, the conflict between the spirit of stagnation and the parties in favour of ‘movement’. Balzac’s contention is that the majority of journalists under these three monarchs, instead of recognizing that they were called to a serious, even sacred mission, turned the Press into an instrument for self-advancement, prostituted principles to intrigue and used journalism merely as a means of acquiring money, position and power. He is reluctant to admit that there were great, responsible press organs, like Le Journal des Débats, Le Conservateur, Le Constitutionnel and, from 1824, Le Globe, which stood firm on principle; he is above all aware of the vogue which the petits journaux enjoyed after the fall of Napoleon, and of the role they played as political privateers.

The petits journaux were so-called because they were produced in smaller format than the important dailies or weeklies, which were more or less grave, staid and ponderous. They proliferated in Paris once the fall of the Empire had given a relative, though still precarious liberty to the Press — precarious because it was constantly threatened by the increasingly reactionary governments of the time. The politicians of the Right found it difficult to keep the newspapers under control even by such means as stamp-duty, caution-money, fines, suspensions and suppressions, the object of these being mainly to put obstacles in the way of would-be founders of hostile periodicals. The ‘little papers’, short-lived as they often proved to be, were much given to journalistic sharp-shooting. They preferred satire, personal attack, sarcasm and scandal-mongering to serious argument or the affirmation of ideals. They were mostly Opposition journals and were a constant thorn in the flesh of the Government. Balzac’s aim was to expose their addiction to ‘graft’, intrigue, blackmail and the misuse of the feuilleton, namely the bottom portion of the first page or other pages generally reserved for critical articles and frequently devoted to the malicious task of slashing literary reputations. Andoche Finot — the prototype of such later newspaper magnates as Émile de Girardin and Armand Dutacq, pioneers in 1836 in the founding of cheap dailies which relied on advertisement and serialized novels as a chief source of income — acquires a large share in a big daily and hands on to the equally unprincipled Lousteau the editorship of the ‘little paper’ he already owns. Balzac probably had Le Figaro chiefly in mind, a periodical which was constantly going bankrupt or being suppressed but kept popping up again under different editors. Hector Merlin’s royalist Drapeau Blanc, edited by Martainville, really existed, having been founded in 1819; so did Le Réveil. Other examples of ‘little papers’ before 1830 were Le Nain Jaume (Bonapartist), Le Diable Boiteux and Le Corsaire (both Liberal), Le Voleur, La Mode, La Silhouette, and, under Louis-Philippe, not only the phoenix-like Figaro, but also La Caricature, Le Charivari (ancestor of our English Punch), and once more Le Corsaire: a few among many. Louis-Philippe and his Cabinets were easy prey for these stinging gad-flies whose unremitting satire and innuendo remind one of the present-day Canard Enchaîné.

It is an amusing thought that, in the late twenties and early thirties, Balzac had himself been a contributor to these disreputable rags and sometimes had a hand in the running of them; for instance he had helped Philipon to found La Caricature. Throughout his career he contributed many novels in serial form to the more important newspapers, notably those founded by Girardin and Dutacq — La Presse and Le Siècle. But by the time he was writing A Great Man in Embryo he had left the petits journaux far behind him. He himself tried his luck as a newspaper-proprietor and editor: he bought La Chronique de Paris in 1836 and founded La Revue Parisienne in 1840. Both of these ventures failed. We can well imagine therefore what a large amount of bile was accumulating inside him. On the whole, reviews of his works appearing in periodicals had been hostile if not harsh. He suffered much from the disparagement of editors and critics such as Sainte-Beuve and Jules Janin respectively. He was always quarrelling with Émile de Girardin. And so he took his revenge. He had already made a preliminary attack on the periodical press in The Skin. And he followed up his attack of 1839 with his Monograph of the Paris Press (1842).

Balzac’s novel is very concerned with all aspects of journalism. For example, chapter 17 is titled “How a news-sheet is edited” and chapter 18 is a symposium on newspapers. Chapter 18 quotes a German guest who states, “I thank god there are no newspapers in my country.” (page 312). Another participant states, “In corporate crimes no one is implicated.” “A newspaper can behave in the most atrocious manner and no one on the staff considers that his own hands are soiled.” (page 314).

‘The influence and power of newspapers are only just dawning,’ said Finot. ‘Journalism is in its infancy; it will grow up. In ten years from now, everything will be subject to publicity. Thought will enlighten the world…’

‘Newspapers are an evil,’ said Claude Vignon. ‘An evil which could be utilized, but the Government wants to fight it. There’ll be a conflict. Who will go under? That’s the question.’

by Iñaki Aldasoro, Jon Frost, Sang Hyuk Lim, Fernando Perez-Cruz & Hyun Song Shin

Key takeaways

Existing anti-money laundering (AML) approaches relying on trusted intermediaries have limited effectiveness with decentralized record-keeping in permissionless public blockchains.

The public transaction history on blockchains can enable AML and other compliance efforts, such as FX regulations, by leveraging the provenance and history of any particular unit or balance of a cryptoasset, including stablecoins.

An AML compliance score based on the likelihood that a particular cryptoasset unit or balance is linked with illicit activity may be referenced at points of contact with the banking system (“off-ramps”), preventing inflows of the proceeds of illicit activity and supporting a culture of “duty of care” among crypto market participants.

by Emanuel Kohlscheen, Phurichai Rungcharoenkitkul, Dora Xia & Fabrizio Zampolli

Key takeaways

Tariffs affect economies most directly through trade volume and prices. Tariffs lower output growth everywhere, though the magnitude varies by country and scenario. They also tend to raise inflation, most notably in the imposing countries.

Ever since new tariffs were enacted in early 2025, a key policy question has been what is the extent to which businesses will pass tariff costs through to prices, and when? The effects of a tariff are rarely straightforward, given, among other things, competitive dynamics and the challenges of implementation, but the historically large and changing nature of these tariffs have created additional levels of uncertainty over the effects.

In uncertain times, anecdotal evidence from businesses can be especially insightful. We are learning how businesses are reacting to tariffs through the Richmond Fed’s business surveys as well as through hundreds of one-on-one conversations with Fifth District businesses since the start of 2025.

These conversations showcase that navigating tariffs is a complex and sometimes protracted process for firms, particularly when there is uncertainty. Firms describe several reasons they may not have experienced the full impact of proposed tariffs yet (even when goods and countries they deal with are subject to them), as well as reasons that even when they have incurred tariff-related cost increases, there can be a delayed impact on pricing decisions.

Reasons Firms May Not Have Incurred Tariffs Yet

Business contacts describe several strategies or circumstances that can delay or reduce the tariffs on inputs or other imported items. These include the following:

Delayed ordering. In response to announced tariffs, many firms ran down existing inventories or ran inventories lean in hopes that tariffs would become lower. For example, a national retailer said everyone was “delaying all we can delay in hopes we get more clarity on trade deals” and reported meeting with procurement teams multiple times per week to discuss ports and ship capacity, evolving tariffs, and inventories to keep goods flowing and prices as low as possible. One port said they have a crane waiting to be shipped but can’t do so now due to the tariffcost.

Cost-sharing.Vendor relationships are often long term, and many firms report partnering with suppliers and customers to share costs. When tariffs first rolled out, multiple firms (a beverage distributer, supply chainlogistics company) anticipated a “rule of thirds” where the cost was split evenly among the supplier, the importer, and the customer. A national retailer reported being large enough to force suppliers to bear much of the cost, though it varied by relationship and item. Interestingly, firms also reported that cost-sharing is not necessarily a permanent solution: A steeldistributer said that with the second round of tariffs announced in June, “The ‘kumbaya’ of cost-sharing was likely to come to an end.” Similarly, a fabricmanufacturer said that upon an announced trade deal with Vietnam that took tariffs from 10 percent to 20 percent, suppliers took a new stand on cost sharing: “Most vendors said you’re on your own” for the second 10 percent, and one even clawed back cost-sharing from the first round.

Transit time. It takes up to six weeks for container ships to arrive to the East Coast from China, so even if firms are ordering goods, there is a natural delay when the tariff is incurred. Shipping time in a world of rapidly changing tariff proposals add to uncertainty around tariffcosts.

Tariff implementation delays.Richmond FedeconomistMarina Azzimonti has found that a variety of tariff implementation delays help explain why actual tariffs as of May 2025 were much lower than expected. These factors include legacy exemptions and delays in customs system updates. Azzimonti also finds that a small percentage is explained by countries substituting away from high-tariff countries. For example, one national retailer we spoke with was in the process of dropping 10 percent of products sourced from China. Whether a company can change sourcing varies dramatically by type of firm and product.

As our monthly business surveys have found, many firms report deploying more than one strategy to delay tariffs. Notably, many of these delays are only temporary.

Reasons Tariffs May Have a Delayed Impact on Prices

Even when firms have incurred tariffs, they give several reasons why tariffs may not be immediately reflected in the prices they charge for their products. These include the following:

Waiting for tariff policy to clarify. Higher prices could reduce demand for goods and services and/or lead firms to lose market share, so many firms said they are hesitant to increase prices until they’re sure tariffs will remain in place. For example, a large national retailer said if tariffs are finalized at a sufficiently low level, they’ll absorb what they’ve incurred to date, but if high tariffs stick, they’ll have to raise prices. A steel fabricator for industrial equipment described being reluctant to raise prices on the 10 percent cost increases they’d seen thus far but would have to raise prices should the increases reach 12 to 13 percent. A grocery store chain was reluctant to raise prices and instead might reduce margins, which had recovered in recent years, to maintain their customer base. Some firms explicitly noted a strategy to both raise prices over time and pursue efficiency gains to cut costs and completely restore margins within a year or two.

Elasticity testing. Firms reported testing across goods whether consumers will accept price increases. A furnituremanufacturer said he’s seen competitors pass along just 5 percentage points of the tariffs at a time so it isn’t such a huge shock to customers, though in that sector, “We all end in the same place which is the customer bearing most of it.” A national retailer said most firms are doing a version of stair-stepping tariffs through, e.g., raising prices a small amount once or twice to see if consumer demand holds, and if so, trying again two months later. This retailer said prices were going up very marginally in early summer, would increase more in July and August, and would be up by 3 to 5 percent by the end of Q4 and into 2026. Another national retailer said they would start testing the extent to which demand falls with price increases, e.g., when the first items that were subject to tariffs—in this case back to school items—hit shelves in late July.

Blind margin. Some firms reported attempting to pass through cost in less noticeable ways. While any price increase to consumers will be captured in measures of aggregate inflation, the fact that price increases may occur on non-tariffedgoods might make it difficult to directly relate price increases to tariffs. An outdoor goodsretailer said, “Unless it’s a branded item where everyone knows the price, if something goes for $18, it can also go for $19.” A national retailer plans to print new shelf labels with updated pricing, which will be less noticeable for consumers compared to multiple new price stickers layered on top. This takes time (akin to a textbook “menu cost” in economics), so it will not be reflected in prices until July and August. A grocery store said their goal was to increase average prices across the store but focus on less visible prices.

Selling out of preexisting inventory: Many firms noted they still have productioninventory from before tariffs were announced, so they do not need to raise prices as long as they still sell these lower cost goods. A national retailer noted they have at least 25 weeks of inventory on hand for most importedproducts. A firm that produces grocery items said they will decide how much to raise prices as they get closer to selling tariff-affected products. Similarly, retailers order seasonal items quarters in advance. Many were receiving items for fall and winter when the new tariffs were going into effect in the spring. They paid the tariff then, but we won’t see the price increase until those items hit the shelves in the fall or winter. One retailer speculated that seasonal décor items will look the most like a one-time increase.

Pre-established prices. Many firms face infrequent pricing due to factors like annual contracts or pre-sales. For example, a dealer of farm equipment gets half its sales through incentivized pre-sales to lock in demand and smooth around crop cycles. They noted that while it would be difficult to retroactively ask those customers to pay for part of the tariff, they will pass tariffs directly through on spare parts. A steel fabricator for industrial equipment has a contract for steel through Q3, so they haven’t been impacted yet by price increases. However, they will face new costs once that contract expires.

In general, compared to small firms, large firms have more ability to negotiate with vendors, temporarily absorb costs, burn cash, wait for strategic opportunity, and test things out. This matters because large firms often lead pricing behavior among firms, so these strategic choices may influence the response of inflation to tariffs more generally. Even within firm size, one often hears that negotiations on price vary considerably by relationship and item.

Conclusion

A key question surrounding tariffs is whether any effects on inflation will resemble a short-lived price increase—as in the simplest textbook model of tariffs—or a more sustained increase to inflation that may warrant tighter Fedmonetary policy. When asked in May what will determine the answer, Fed ChairJerome Powellcited three factors [archived PDF]: 1) the size of the tariff effects; 2) how long it takes to work their way through to prices; and 3) whether inflation expectations remain anchored. The insights shared above suggest the process from proposed tariffs to the prices set by firms is far from instantaneous or clear-cut, particularly when tariff policy is changing.

Sensing from businesses suggests that the impact of tariffs on their price-setting [archived PDF] has been lagged, but it is starting to play out. Nonetheless, it remains highly uncertain how tariffs will impact consumerinflation. The discussion above makes clear that firms are nimble and innovative in the face of challenge, and they are concerned about losing customers in the current environment, particularly consumer-facing firms. We will continue to learn from our business contacts and share their insights.

by Hamza Abdelrahman, Luiz Edgard Oliveira and Aditi Poduri

Information the San Francisco Fed collects from businesses and community sources for the Beige Book provides timely insights into economic activity at both the national and regional levels. Two new indexes based on Beige Book questionnaire responses track business sentiment across the western United States. The indexes track data on economic activity and inflation, serving as early indicators of official data releases and helping improve near-term forecasting accuracy. The latest index readings suggest weakening economic growth and intensifying inflationary pressures over the coming months.

This Economic Letter examines the economic information collected through the SF Fed’s Beige Book questionnaire over the past 10-plus years. We analyze this information by constructing sentiment indexes from the qualitative data and comparing them with quantitative measures of national and regional economic activity and inflation. We introduce two indexes—the SF Fed Business Sentiment Index and the SF Fed Inflation Gauge Index—which track our contacts’ views and expectations for economic growth and inflation, respectively. We find that these new indexes serve as reliable early indicators of official data releases and help improve near-term forecast accuracy. The SF Fed Business Sentiment Index has generally exhibited patterns similar to other recent business and household sentiment indexes, and the SF Fed Inflation Gauge Index has shown a strong uptick in expected inflation. To regularly monitor changes in these two indexes, the San Francisco Fed has launched a new Twelfth District Business Sentiment data page.

Constructing regional sentiment indexes

The San Francisco Fed sends out a Beige Book questionnaire to business and community contacts across the District eight times a year to gather regional information. In addition to answering questions regarding their organizations, respondents share their views on regional and national topics, including economic activity and inflationary pressures.

In two questions, respondents indicate whether they see national output growth and inflation rates increasing, decreasing, or staying stable over the coming year using a standard five-tiered scale. We use these responses since 2014 to formulate two business sentiment indexes, one on economic activity and another on inflation. We assign standard weights to the five-tiered qualitative scale that are symmetrical around zero. For example, we ask if activity is expected to “decrease significantly” = –2, “decrease” = –1, “remain unchanged” = 0, “increase” = 1, or “increase significantly” = 2. We add up the weighted shares of responses for each tier within each index. We then normalize each resulting series by its own average and standard deviation for ease of comparison with traditional economic indicators.

Tracking business sentiment

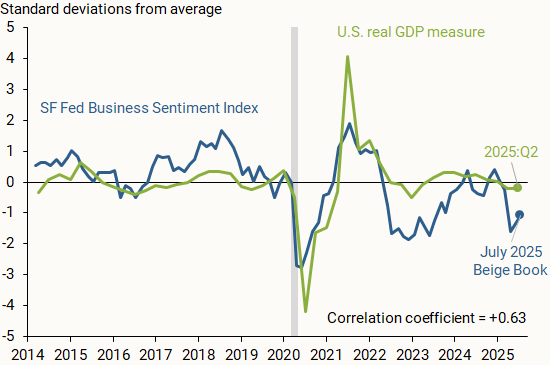

Figure 1 shows how the SF Fed Business Sentiment Index (blue line), compiled from responses to the question on national economic activity, compares with data on changes in national GDP (green line). We measure national output as the four-quarter change in inflation-adjusted, or real, GDP, normalized by its average and standard deviation so that it is centered around zero and, hence, more directly comparable to the SF Fed Business Sentiment Index. The vertical axis shows how many standard deviations away each observation is from its respective measure’s average from 2014 to mid-2025.

Figure 1 Economic growth versus business sentiment

The SF Fed Business Sentiment Index generally tracks the movements in national GDP over the past decade; a correlation coefficient of +0.63 on a scale of –1 to 1 indicates a moderately strong positive relationship between the two measures. A relatively recent exception started in 2022, when our index began showing a considerable decline relative to the national GDP measure. Respondents across the District were downbeat about economic growth and reported expectations of a sharp decline in consumer spending and overall household financial health following the depletion of pandemic-era savings (Abdelrahman and Oliveira 2023). A similar decline appeared in other measures of business and household sentiment. Nevertheless, overall economic growth continued at a solid pace. This decoupling between sentiment and hard data that began in 2022 was dubbed a “vibecession” (Daly 2024, Scanlon 2022).

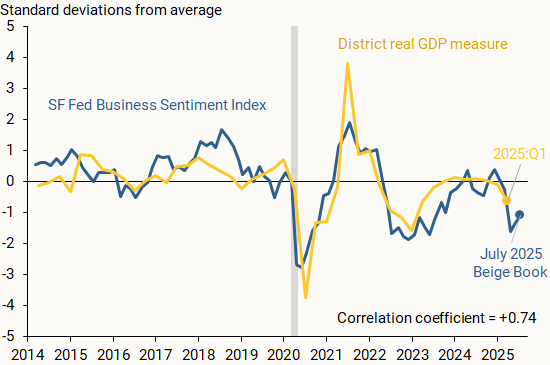

Another possible reason for the divergence between national real GDP and our Business Sentiment Index is the influence of the regional economy. Although respondents are asked about their views of national GDP, their responses may be affected by regional outcomes. Thus, our index may also reflect a regional perspective from our business and community contacts.

Figure 2 supports this rationale, showing the SF Fed Business Sentiment Index alongside a measure of regional output growth (gold line). We find that the measures closely track one another, including for 2022 and 2023, with a correlation coefficient of +0.74. We define District real GDP growth as the year-over-year percent change in the total output of the District’s nine states as reported by the Bureau of Economic Analysis (BEA). We normalize the series as described before.

Figure 2 Regional economic growth and business sentiment

Our findings indicate that the SF Fed Business Sentiment Index can serve as an accurate early indicator for national and regional output growth. Since the regional Beige Book questionnaire is collected twice each quarter, it provides particularly timely insights into economic activity during the current quarter. By contrast, the first GDP data release for any given quarter usually arrives a full month after that quarter has ended, and initial data releases for state-level output growth arrive with even more delay.

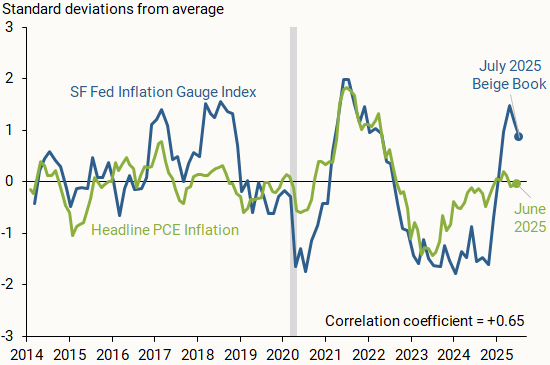

Our Beige Book questionnaire responses also provide insights into how business and community contacts in the District see national inflation evolving. Figure 3 compares the SF Fed Inflation Gauge Index (blue line) with monthly changes in the year-over-year headline personal consumption expenditures (PCE) inflation rate published by the BEA (green line). We normalize the inflation series and index as discussed earlier.

Figure 3 SF Fed Inflation Gauge Index versus realized inflation

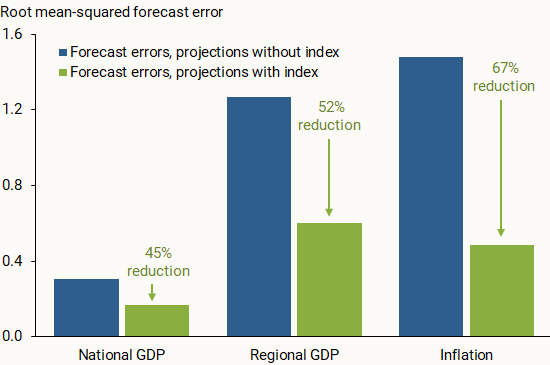

Beyond tracking data on national and regional economic conditions, we consider whether our two indexes can help improve one-year-ahead projections of output growth and overall inflation. We run linear regressions on a 2014–2022 data sample and estimate out-of-sample projections for the period starting in the first quarter of 2023. We run this analysis for the three economic measures—national GDP, regional GDP, and inflation—once with our index included on the right-hand side of the regression equation and once without the index. For this analysis, we use versions of the SF Fed Business Sentiment Index and the SF Fed Inflation Gauge Index that have been aggregated quarterly.

Figure 4 compares the out-of-sample projection accuracy of the two iterations. Across all economic measures, incorporating the SF Fed Business Sentiment Index or the SF Fed Inflation Gauge Index in the regression noticeably reduced the forecast errors for the out-of-sample period. This general result appears to hold when we project output growth and inflation one quarter ahead, in line with other studies that incorporate soft data from the Beige Book in short-term projections (Balke and Petersen 2002). The results are also consistent when using a local projections method from Jordà (2005) for one-year-ahead projections of output growth and shorter-term projections of inflation. This further supports the usefulness of our qualitative measures as early indicators of the future economic landscape over the short term.

Figure 4 Forecast errors with and without SF Fed sentiment indexes

Information collected from businesses and communities through the San Francisco Fed’s regional Beige Book questionnaire can provide valuable insights into the national and regional economies. Sentiment indexes described in this Letter use responses from Twelfth District Beige Book contacts to generally track economic activity and inflation. Our two indexes serve as reliable early indicators of official data, which could help improve near-term forecast accuracy. The SF Fed Business Sentiment Index remained negative for much of 2022 and 2023, possibly reflecting more subdued growth within the District relative to the United States. Meanwhile, the SF Fed Inflation Gauge Index spiked in recent months following adjustments to trade policy.

Inflation expectations for 2025 and 2026 collected by the Focus survey remained above the inflation target and stand at 5.1% and 4.4%, respectively. Copom’s inflation projections for the first quarter of 2027, currently the relevant horizon for monetary policy, stand at 3.4% in the reference scenario (Table 1).

The risks to the inflation scenarios, both to the upside and to the downside, continue to be higher than usual. Among the upside risks for the inflation outlook and inflation expectations, it should be emphasized (i) a more prolonged period of de-anchoring of inflation expectations; (ii) a stronger-than-expected resilience of services inflation due to a more positive output gap; and (iii) a conjunction of internal and external economic policies with a stronger-than-expected inflationary impact, for example, through a persistently more depreciatedcurrency. Among the downside risks, it should be noted (i) a greater-than-projected deceleration of domestic economic activity, impacting the inflation scenario; (ii) a steeper global slowdown stemming from the trade shock and the scenario of heightened uncertainty; and (iii) a reduction in commodity prices with disinflationary effects.

The Committee has been closely monitoring the announcements on tariffs by the USA to Brazil, which reinforces its cautious stance in a scenario of heightened uncertainty. Moreover, it continues to monitor how the developments on the fiscal side impact monetary policy and financial assets. The current scenario continues to be marked by de-anchored inflation expectations, high inflation projections, resilience on economic activity and labormarket pressures. Ensuring the convergence of inflation to the target in an environment with de-anchored expectations requires a significantly contractionary monetary policy for a very prolonged period.

Copom decided to maintain the Selic rate at 15.00% p.a., and judges that this decision is consistent with the strategy for inflation convergence to a level around its target throughout the relevant horizon for monetary policy. Without compromising its fundamental objective of ensuring price stability, this decision also implies smoothing economic fluctuations and fostering full employment.

The current scenario, marked by heightened uncertainty, requires a cautious stance in monetary policy. If the expected scenario materializes, the Committee foresees a continuation of the interruption of the rate hiking cycle to examine its yet-to-be-seen cumulative impacts, and then evaluate whether the current interest rate level, assuming it stable for a very prolonged period, will be enough to ensure the convergence of inflation to the target. The Committee emphasizes that it will remain vigilant, that future monetary policy steps can be adjusted and that it will not hesitate to resume the rate hiking cycle if appropriate.

The following members of the Committee voted for this decision: Gabriel Muricca Galípolo (Governor), Ailton de Aquino Santos, Diogo Abry Guillen, Gilneu Francisco Astolfi Vivan, Izabela Moreira Correa, Nilton José Schneider David, Paulo Picchetti, Renato Dias de Brito Gomes, and Rodrigo Alves Teixeira.

Table 1

Inflation projections in the reference scenario Year-over-year IPCA change (%)

In the reference scenario, the interest rate path is extracted from the Focus survey, and the exchange rate starts at USD/BRL 5.55 and evolves according to the purchasing power parity (PPP). The Committee assumes that oil prices follow approximately the futures market curve for the following six months and then start increasing 2% per year onwards. Moreover, the energy tariff flag is assumed to be “green” in December of the years 2025 and 2026. The value for the exchange rate was obtained according to the usual procedure.

Note: This press release represents the Copom’s best effort to provide an English version of its policy statement. In case of any inconsistency, the original version in Portuguese prevails.

by Mohammad Al-Shehri, Assistant Economist & Omar Al-Nakib, Head of MENA Research

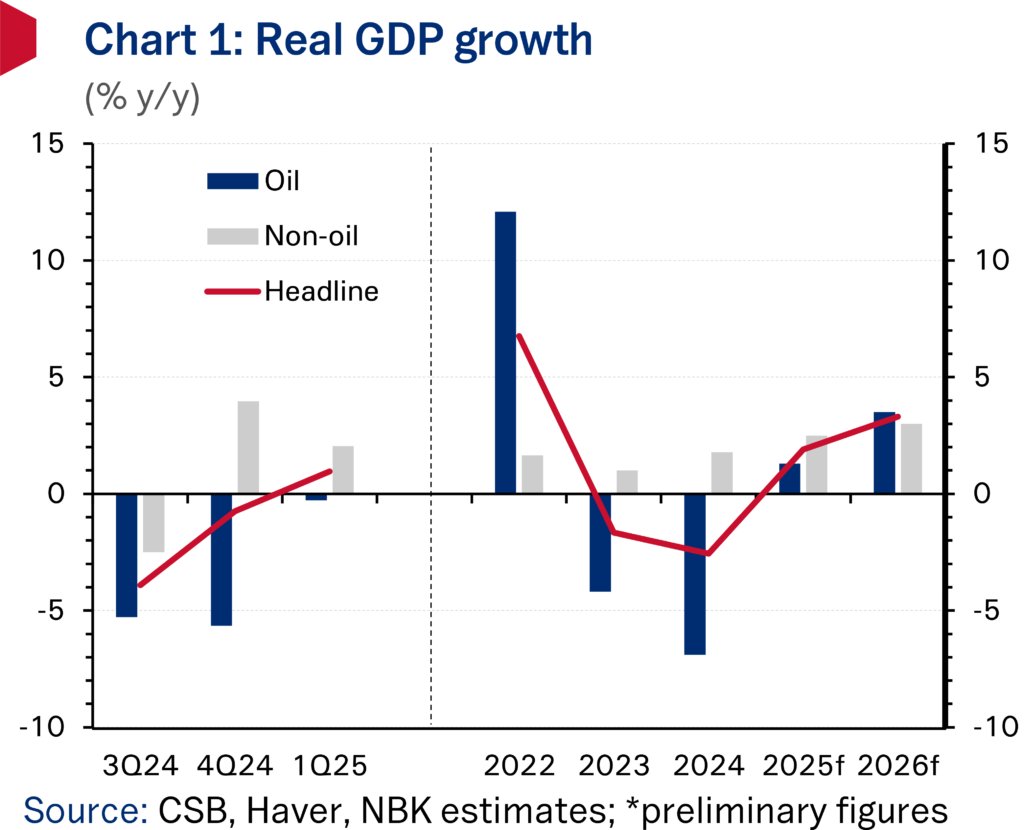

Preliminary official figures show GDP expanding 1% y/y in Q1 2025 following seven consecutive quarters of contraction, helped by a less severe downturn in oil output. With the negative effects of earlier voluntary oil production cuts beginning to fade, oilGDP recorded only a marginal decline, the softest since Q2 2023. Growth in non-oil activity remained positive though eased, weighed by a moderation in the manufacturing, real estate, and transportsectors. The near-term outlook for GDP is one of positive growth, lifted by rising oil production after Kuwait started to restore 135 kb/d of oil output cuts between April and September 2025, while the non-oilsector should also register further steady gains.

Non-oil GDP growth softens in Q1 2025 after strong performance in Q4 2024

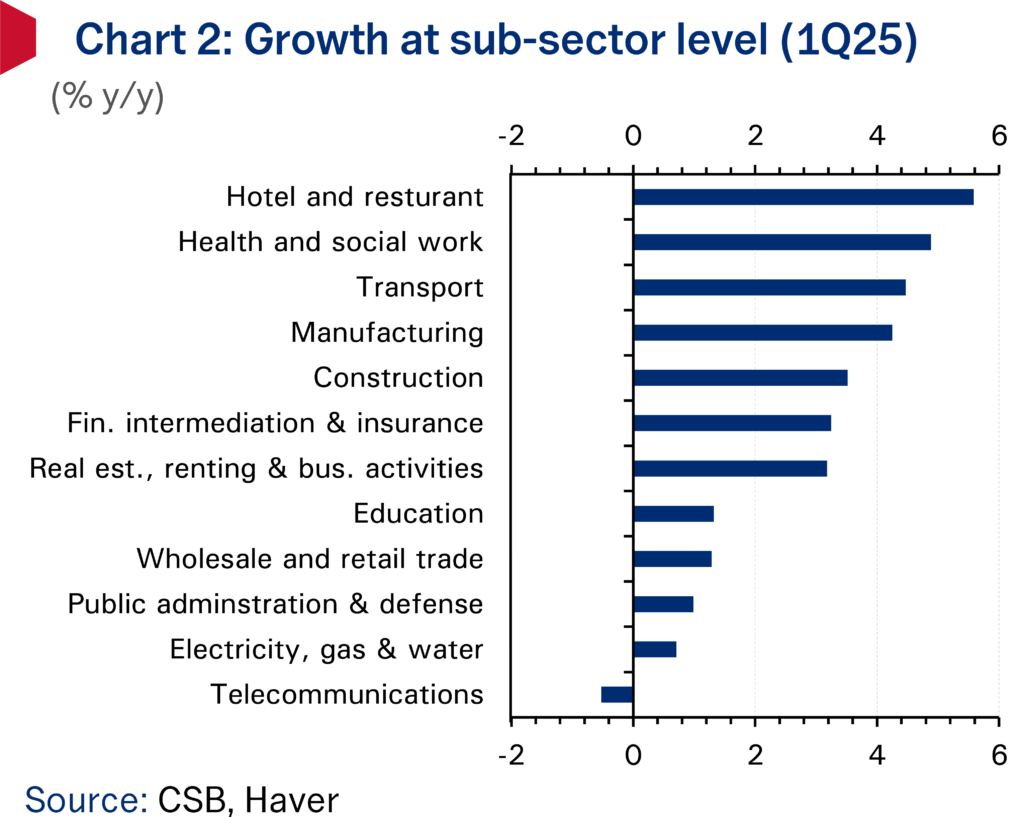

Growth in the non-oilsector weakened in Q1 2025, slowing to 2% y/y compared to 4% recorded in the prior quarter. (Chart 1.) The softer expansion in non-oil activity reflected, among other things, a moderation in the manufacturingsector, where activity grew at a still-solid 4.3% despite a decline in refined petroleum products output but slowed notably from the 12.2% reading registered in Q4 2024. Growth in other sectors including real estate, wholesale & retailtrade, transport, and education also slowed. Offsetting the slowdown was stronger expansion in the non-oileconomy’s largest segments: public administration and defense as well as financial intermediation and insurance, which grew 1% and 3.2% y/y, respectively. (Chart 2.)

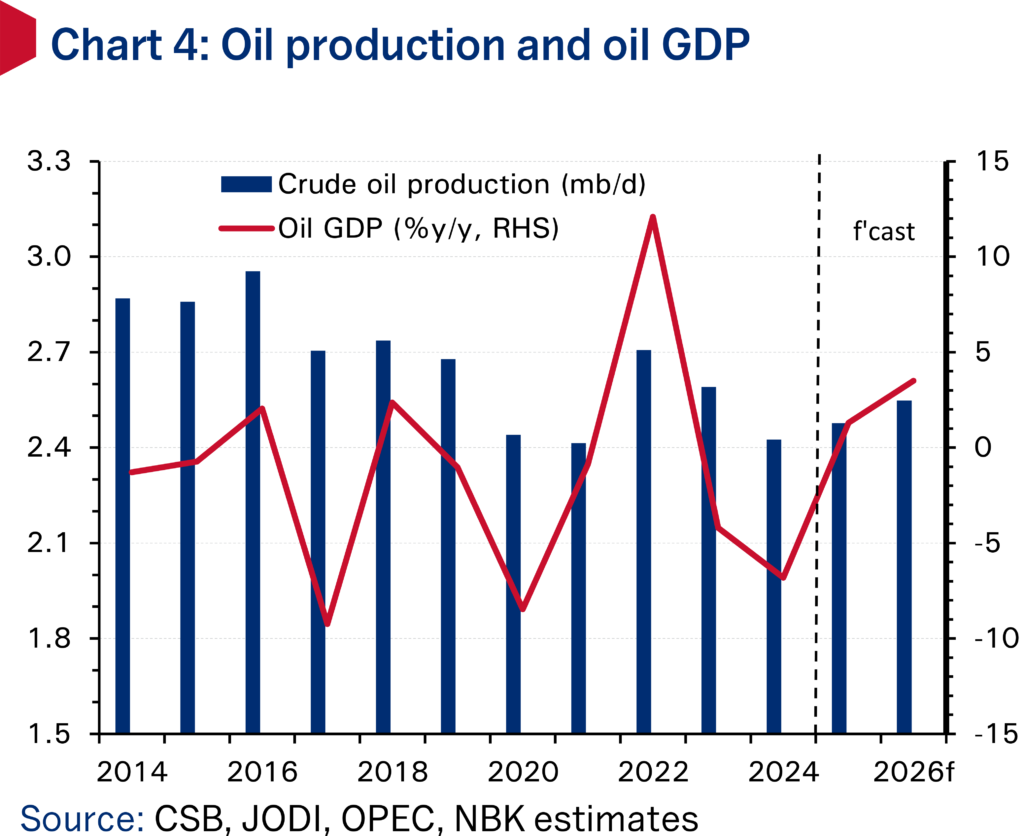

Oil sector logs marginal contraction, set to return to growth in Q2

The contraction in oilGDP eased significantly to -0.3% y/y from -5.7% y/y in Q4 2024, registering the softest rate of decline since Kuwait embarked on cutting oil production in Q2 2023 after participating in the voluntary cuts scheme with 7 other OPEC+ members. (Chart 4.) Kuwait’s oil production averaged 2.415 mb/d in Q1 2025, a 0.7% decline from the same quarter last year, according to OPEC secondary sources. However, oilsector fortunes are set to shift in Q2 2025 and thereafter, after the OPEC-8 member alliance started unwinding the 2.2 mb/d voluntary cut tranche in April 2025. Originally planned to be unwound over the course of 18 months, OPEC+ has accelerated the pace of supply hikes with output now on a path to be fully restored in September, a full year ahead of schedule. For Kuwait, crude production rose by 0.5% q/q in Q2 to 2.426 mb/d and is set to accelerate further to average 2.533 mb/d in H2 2025. With the oil market so far able to absorb the additional OPEC and global supply and oil prices currently holding near $70/bbl, an upside risk to our oilsector outlook involves the potential unwinding of the outstanding OPEC-8 voluntary cuts (1.66 mb/d), of which Kuwait’s share is 128 kb/d.

Growth heading back into positive territory in 2025

Growth in total GDP is set to remain on a positive trajectory in the near term, buoyed by further steady expansion in non-oileconomic activity and increased oil production. Non-oilGDP is set to benefit from the government’s reform drive which includes the recent passing of the debtlaw that could catalyze the implementation of key development projects and the potential approval of the ‘mortgage’ law later in 2025, which could spur higher household borrowing and consumer spending. Economic indicators for Q2 2025 pointed to a healthy pace of non-oileconomic activity. The key ‘output’ and ‘new orders’ balances in the non-oilprivate sectorPMI gauge both averaged a very robust 57+ in Q2 2025, real estate activity continued to expand at a robust pace with earlier price falls in the residentialsector abating, while credit growth stood at a healthy 5.5% y/y in May, and could benefit in coming months if interest rates are reduced further.

Nonetheless, there are also downside risks to the outlook. Local consumer spending growth (according to central bankcardtransactions data) turned negative in Q1 2025, extending the weakening trend now observed for more than a year. The government’s ongoing fiscal consolidation push will also weigh on wage and job growth. Overall, we see GDP growing 1.9% this year, boosted by expansions in both the oil and non-oilsectors of 1.2% and 2.5%, respectively.

Beijing clarifies its deal with Washington didn’t include NVIDIA’s 4th-best AI chip, disputing widely-reported comments by U.S. Commerce Secretary Howard Lutnick

“We have taken note that Washington has now taken the initiative to announce it will authorize sales of NVIDIA’s H20 chips to China,” the trade ministry added.

Beijing’s clarification stands in stark contrast to widely reported public comments earlier this week by U.S. Commerce SecretaryHoward Lutnick, who told Reuters on Tuesday that “We put that in the trade deal with the magnets,” referring to the agreement made to restart Chineserare earth shipments to U.S. manufacturers. He did not provide additional details, according to Reuters.

NVIDIA’s H20 was designed to be technologically inferior. The company also sells three other chips that far surpass the H20’s power.

Following the China–U.S.economic and trade consultations in London, the two sides have maintained close communication, finalized the “London framework,” and moved forward with implementation. China, in accordance with its laws and regulations, approves export applications for controlled items that meet the necessary criteria. In early July, the United States reciprocally lifted the restrictions on China that had been discussed during those talks.

We have taken note that Washington has now taken the initiative to announce it will authorize sales of NVIDIA’s H20chips to China.Beijing believes the United States should abandon a zero-sum mentality and continue to roll back a range of unwarranted trade and technology restrictions on China.

Cooperation and mutual benefit are the only viable path; suppression and containment lead nowhere. In May, the United States issued new export-control guidelines targeting Huawei’s Ascend chips, tightening restrictions on Chinesesemiconductor products under unfounded pretexts. By wielding administrative power to distort fair market competition, these measures severely undermine the legitimate rights and interests of Chinesecompanies. China has made its position clear and firmly opposes such actions.

We look forward to the United States working with China in a spirit of equality to correct these erroneous practices, foster a sound environment for mutually beneficial cooperation between the two countries’ enterprises, and jointly safeguard the stability of global semiconductorsupply chains.