[from the International Monetary Fund, by Patrick A. Imam, Kangni R Kpodar, Djoulassi K. Oloufade, Vigninou Gammadigbe]

This paper delves into the intricate relationship between uncertainty and remittance flows. The prevailing focus has been on tangible risk factors like exchange rate volatility and economic downturn, overshadowing the potential impact of uncertainty on remittance dynamics. Leveraging a new dataset of quarterly remittances combined with uncertainty indicators across 77 developing countries from 1999 Q1 to 2019 Q4, the analysis highlights that uncertainty in remittance-sending countries negatively affects remittance flows. In contrast, uncertainty in remittance receiving-countries has a more complex, dual effect. In countries with high private investment ratios, rising domestic uncertainty leads to a decline in remittances. Conversely, in countries with low public spending on education and health, remittances increase in response to uncertainty, serving as a social safety net. The paper underscores the heterogeneous and non-linear effects of domestic uncertainty on remittance flows.

Kicking off a new CGD series of policy proposals to inform the European Union’s upcoming development agenda, Mikaela Gavas and W. Gyude Moore suggest a reset of the EU’s international relations narrative. Explore their ideas for how the EU can position itself as a global development player while staying true to its values and focusing on the common good.

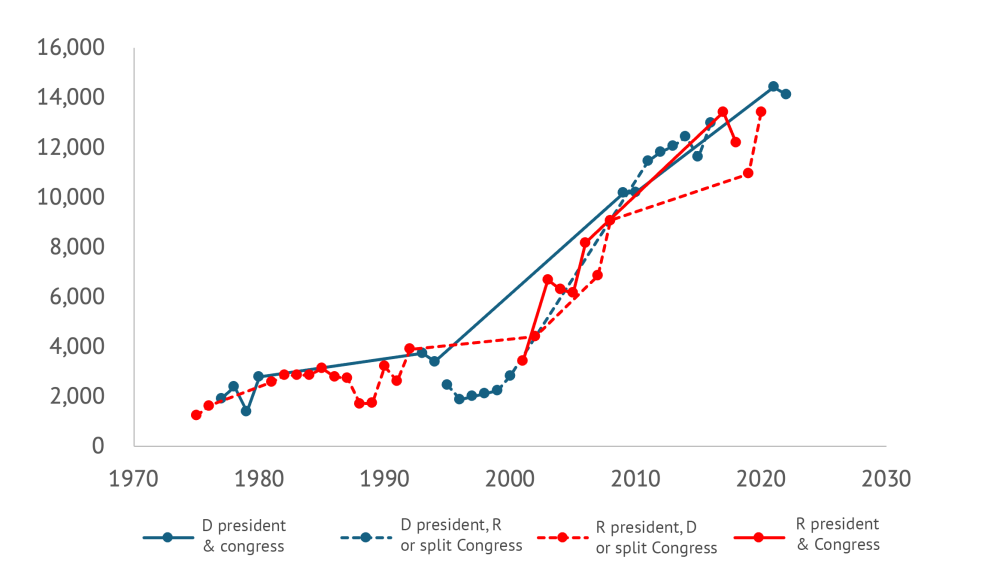

The same applies to aid flows. The figure below shows data on total aid disbursements from the US depending on who is in power: the solid blue line is Democratic control of the presidency and both branches of Congress, the blue dashed line is Democratic control of the presidency and one or neither branch, the solid red line is Republican control of the presidency and both chambers, and the red dashed line is control of the presidency and one or neither chamber. There’s only one data point for each year, of course, but the lines connect between them. The broad picture strongly suggests the trend matters more than who is in power (indeed, remember the Surprise Party?).

Figure 1: US aid disbursements by party control (Current $m)

The potential good news from this is that despite substantive disagreements over topics including the Mexico City Policy, bipartisan cooperation on aid might still be more possible than it might appear from a close-up perspective in the midst of partisan rancor. To repeat the bad news: much of the recent bipartisan movement on foreign economic policy has been to the detriment of developing countries. And there is certainly some talk of sweeping changes, including cuts, that might mean the past is no guide. But perhaps there still space for elements of a positive agenda around aid for the legislative sessions of next year, one that could appeal to at least some people on both sides of the aisle. Examples might include:

Advancing localization: Spending more US aid finance in recipient countries rather than on US contractors has been a hallmark of Samantha Power’s tenure at USAID. But it has Republican antecedents. The Trump administration followed a localization strategy for PEPFAR that significantly increased the number of local partners and a New Partnerships Initiative at USAID designed in part to do the same. And in 2021, US SenatorsMarco Rubio (R–FL) and Tim Kaine (D–VA) introduced legislation to reduce red tape for local organizations seeking USAID funds. It would be great to see further cooperation on ensuring more development dollars are actually spent in developing countries.

Country focus: All else even somewhat equal, a dollar of foreign assistance simply has a larger impact in poorer countries. The logic that richer countries should be able to look after themselves was a justification for the Trump administration’s “Journey to Self-Reliance”—a philosophy dedicated toward “ending the need for aid.” The Biden administration has continued to produce the “country roadmaps” designed to chart the journey. It would be great to see bipartisan efforts to focus grant resources in particular where they’ll have the greatest impact—in the poorest countries.

Sovereign lending and guarantees: While grants should be focused on poorer countries, loans could be an effective and comparatively low-cost tool to support wealthier countries. The recently passed Ukraineaid package provided resources in the form of partially forgivable loans, and senior Republicans have been pushing the model more widely. More lending and guarantees could be a powerful tool to support infrastructure rollout in middle-income countries. And strengthening the US sovereign loan guarantee program could back development and national security goals at a considerably lower cost than grant-based programs.

MCC reform: The Millennium Challenge Corporation, created during the George W. Bush administration, is running into pipeline challenges—and appropriators have clawed back funding in response. That’s a shame. It is a small but effective aid agency providing resources for development priorities including infrastructure and working with client countries to help them deliver—in fact, it’s a model of successful localization. MCC faces spending challenges in part because it hasn’t increased the size of individual country operations, limits repeat operations, and can only work in countries that pass its “scorecard” of development indicators. The agency wants to address its partner problem by working in richer countries. That’s a sad way to achieve impact and goes against the bipartisan principle that richer developing countries should be weaned off aid flows, not given more. Altering the size of compacts, allowing more repeat compacts, and moving away from a scorecard model towards a model of reward for reform—a specific set of policy changes that need to be completed before funds start flowing—would be a far more effective approach.

Fighting malaria: In the 1958 State of the Union, PresidentEisenhower said that the US would lead a global effort to eradicate malaria. The time and the tools were not right then, but today there is far greater hope for rapid progress against the disease. George Bush created the President’s Malaria Initiative in 2005, and the US has been a vital contributor to the global fight against the parasite since then. With the arrival of new vaccines in the past couple of years, we could accelerate progress and save hundreds of thousands of children’s lives each year. And with better vaccines, we could move even faster. PEPFAR, the US initiative to provide HIV drugs, has transformed the battle against AIDS worldwide. A similar bipartisan initiative could achieve as much with malaria.

Transparency: Both parties have shown commitment to increasing the transparency of aid finance including around subawards and indirect cost rate data. It would be great if there was a bipartisan consensus on simply publishing all aid contracts.

Beyond aid, the African Growth and Opportunity Act was first passed during the Clinton administration, renewed during the Bush administration and then again under the Obama administration. A bipartisan proposal to renew the trade package once more was launched in the Senate in April this year. Perhaps AGOA could be made even bigger and better. Even amidst partisan rancor, there is plenty a Congress and administration could do to improve US relations with and support to low- and middle-income countries next year.

Undoing Gender Inequality Traps in the Financial Sector: The Case of Colombia

by Mayra Buvinic and Alba Loureiro, July 9, 2024 (CGD Blog Post)

Gender data is needed to gauge the extent to which financial services include and benefit women. However, sex-disaggregated data that tracks access to and use of financial services is still hard to come by, and it is especially rare to have country-level data that captures the universe of financial sector providers (FSPs) and is published on a regular basis.

A notable exception is Colombia, where Banca de Oportunidades (BdO), a public sector technical assistance and advocacy platform, compiles in a centralized data platform anonymized data from all FSPs in partnership with Colombia’s Superintendency of Banks. The 2023 edition, the 13th annual publication, reports on 15 million transactions, 60 percent of them monetary, from the universe of banks, credit and savings cooperatives, microfinance institutions, and fintechs. The report tells a sobering story worth highlighting of the trajectory of women’s financial inclusion because it mirrors much of what we know [archived PDF] about the constraints women face having access to financial services in low- and middle-income countries. The report’s numbers [archived PDF] suggest that:

Expanding access is not enough

Despite almost universal access to financial products, gender gaps persist. In 2023, 19 out of every 20 adult Colombians (or 94.6 percent) reported access to at least one financial product or service. However, women faced less favorable conditions (see below), underscoring that mere access is insufficient.

Gender gaps are evident in both savings and credit

In 2023, women had 6.5 and 3.7 percentage points (pp) lower access to savings and credit, respectively, than men. While women’s access to savings increased over time–from 75 percent in 2018 to 90.4 percent in 2023–the gender gap widened (from 4.3 pp to 6.5 pp). In the same period, the gender gap in credit narrowed slightly (from 4.8 pp to 3.7 pp) but both men’s and women’s access to credit decreased–for women from 37.7 percent in 2018 to 33.4 percent in 2023.

Women face access to credit in less favorable conditions than men

Interest rates are higher for women clients across all loan types, and highest for microcredit–with a 5.4 percent gender gap–which women access more than men. In 2023, women accessed 1,029 million and men accessed 857,000 microcredit loans. More men than women accessed commercial loans (20,000 versus 14,000 loans) while housing loans went equally to women and men.

Paradoxically, these less favorable conditions coexist with women exhibiting lower credit risks than men

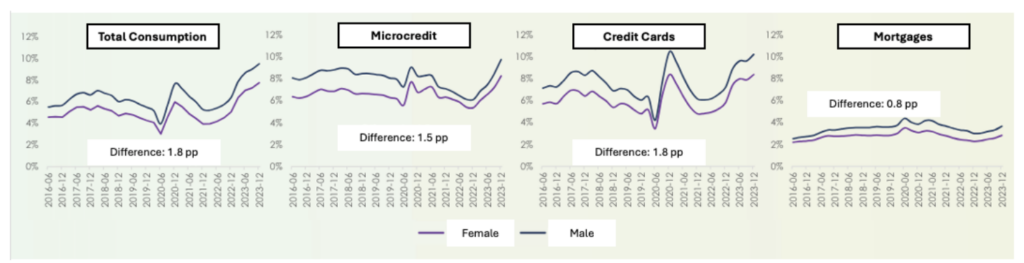

Women have better repayment rates than men across loan types (Figure 1). Women also perform better across insurance products, except for microinsurance, showing lower accident rates. However, female clients have 13.8 pp lower access to insurance products than men.

Figure 1: Total Repayment Rates, Overdue More Than 30 Days.

Source: The graphic was extracted from the Financial Inclusion PowerPoint (Paola Arias and Jaime Rodriguez, 4 June, 2024) [archived PDF], and the labels were translated from Spanish.

The data implies that women’s good financial behavior is penalized rather than prized, with higher interest rates and lower access to financial products

Rationing credit and other financial services to women perpetuates ‘gender inequality traps’ leading to further rationing

It all starts with women having fewer assets to use as collateral and lower earnings than men (a commonplace fact across financial markets everywhere) which leads them to qualify for smaller loans. In turn, this results in women having less access to credit to increase earnings because of the high costs to lenders of serving customers with small loans, resulting in even lower earnings.

Gender biases that affect the supply and demand for credit reinforce this vicious cycle

On the supply side, there are cognitive and perceptual biases (the latter detected by eye-tracking) from financial sector providers–male potential borrowers are ‘ex-ante’ perceived as having higher earnings than similar women. And female bank agents are stricter at evaluating female clients than male clients.

On the demand side, the incorrect assumption that women are higher credit risks than men is reinforced by female clients’ own lower self-confidence and greater self-exclusion from financial services: women do not apply for credit because they anticipate they will be rejected because they have lower earnings.

Not surprisingly perhaps, women in Colombia score lower than men in a financial health indicator–with an average score of 4.9 for women and 5.6 for men measured in a 0 to10 scale (scored by BdO using data from the 2022 edition of the survey).

To overcome these gender inequality traps, only a combination of strategies will work

Solutions must address both demand– and supply-side constraints and include:

Increase women’s self-confidence and combat their self-exclusion from financial services with credit ‘plus’ interventions that include ‘soft skills’ training.

Provide customized products that fit women’s needs, including importantly insurance and microinsurance that respond to women’s greater need for mitigating (family) risks.

Combat supply-side biases that lead to inefficiencies and exclusions, including incentives to financial sector providers to reach women with financial services.

For the above, collect and publish gender data, but data that does not end up sitting on a shelf gathering dust; data that instead is used to make management decisions, which underscores the role of public sector institutions such as BdO in collaborating with and incentivizing financial sector providers, and in measuring, tracking, and reporting progress in financial inclusion.

Fortunately, there is a growing wealth of research that backs up the solutions suggested above. But there is still an important practical research agenda ahead:

First is reaching the poorest and excluded with financial services that they may need. In the case of Colombia, this includes indigenous and Afro-descendent populations in geographically distant regions of the country. This requires building further granularity in the financial inclusion data, following guidelines of intersectionality data in development.

There is substantial research on demand-side constraints in women’s access to financial services. There is comparatively little research on supply-side gender biases and solutions to these biases that can be scaled.

Lastly, there is the task of developing financial health indicators that can be easily and widely used disaggregated by gender and other demographic features to monitor an important development outcome from increasing financial access to all.

Disclaimer

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions.

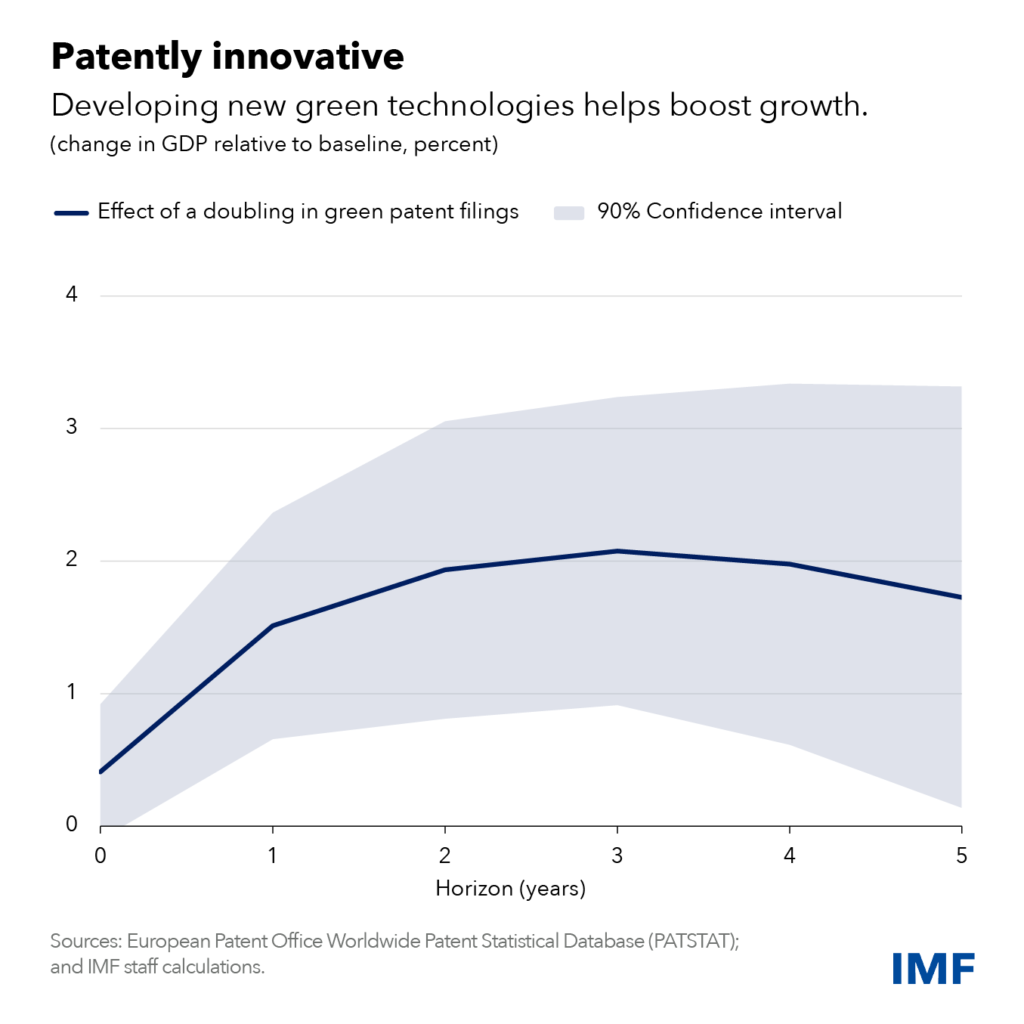

The slower momentum is concerning because, as we show in a new staff discussion note, green innovation is not only good for containing climate change, but for stimulating economic growth too. As the world confronts one of the weakest five-year growth outlooks in more than three decades, those dual benefits are particularly appealing. They ease concerns about the costs of pursuing more ambitious climate plans. And when countries act jointly on climate, we can speed up low-carbon innovation and its transfer to emerging markets and developing economies.

IMF research [archived PDF] shows that doubling green patent filings can boost gross domestic product by 1.7 percent after five years compared with a baseline scenario. And that’s under our most conservative estimate—other estimates show up to four times the effect.

A key question is how countries can better foster green innovation and its deployment. We highlight how domestic and global climate policies spur green innovation. For example, a big increase in the number of climate policies tends to boost green patent filings, our preferred proxy for green innovation, by 10 percent within five years.

One reason policy synchronization has a prominent impact on domestic green innovation is what is called the market size effect. There’s more incentive to develop low-carbon technologies if innovators can expect to sell into a much larger potential market, that is, in countries which adopted similar climate policies.

Another is that climate policies in other countries generate green innovations and knowledge that can be used in the domestic economy. This is known as technology diffusion. Finally, synchronized policy action and international climate commitments create more certainty around domestic climate policies, as they boost people’s confidence in governments’ commitment to addressing climate change.

The risks of protectionism are exacerbated when climate policies, such as subsidies, do not abide by international rules. For example, local content requirements, whereby only locally produced green goods benefit from subsidies, undermine trust in multilateral trade rules and could result in retaliatory measures.

Over the past two weeks, Asia has played host to the most intense sequence of multilateralsummits since the pandemic began, as national leaders gathered for meetings organized by ASEAN, the G20 and APEC. Although overshadowed by geopolitical tensions, the meetings marked a welcome return to in-person summitdiplomacy, and the better-than-expected outcomes show hope yet for multilateralism.

The conclaves began in Phnom Penh with the annual summit of the Association of Southeast Asian Nations. At the first of such in-person events in almost three years, ASEAN leaders took the positive step of agreeing in principle to admit East Timor as the 11th member of the organization.

As leaders moved on to Bali for the Group of 20summit, expectations were low after ministerial meetings in the run-up had failed to produce consensus. Earlier in the year, given fractures in the wake of Russia’s invasion of Ukraine, there was a question mark over whether the G20 could even go ahead or survive in its existing form.

In the end, the summit surpassed expectations by producing a joint declaration after intense negotiations, with leaders finding the compromises necessary to unite in declaring that “today’s era must not be of war” and pledging to uphold the multilateral system.

Reflecting on these three summits, three takeaways give reason for cautious optimism that multilateralism can yet be revived and play a major role in solving our challenges.

First, and perhaps most obviously, the return of in-person summitdiplomacy is a welcome uplift for global cooperation. Virtual formats played a useful interim role at the height of the pandemic but were never a substitute for getting leaders in the same room. That is especially when it comes to interactions on the sidelines, often as important as the main event.

China’s return to diplomacy at the highest level was a further boost, both for the nation and the rest of the world.

Leaders got to meet their new counterparts for the first time or build on existing relationships, which can only help global cooperation.

The second takeaway is that as grave as our challenges are, the threat of escalating conflict and severe economic pressures on all nations seem to be focusing minds and increasing the willingness to engage and cooperate—out of necessity if nothing else.

The G20summit was the second major one this year to surpass expectations after the 12th World Trade OrganizationMinisterial Conference in June surprised observers by agreeing on a plan to reform the organization and its dispute settlement mechanism. The G20 statement reiterated support for this WTO reform plan, which will be critical to get the free trade agenda back on track and provide a much-needed boost for the global economy.

Third, and perhaps most significantly for the long term, the recent summits marked an acceleration of the trend towards multi-polarization in international diplomacy, and in particular, the rising influence of non-aligned “middle powers” to shape multilateral outcomes.

The middle powers represented at ASEAN, the G20 and APEC have huge stakes in avoiding a bifurcation of the global economy that might result from a new cold war. They don’t want to be forced to pick sides and many show a growing willingness and ability to build bridges and restore positive momentum for multilateralism.

Indonesia is a prime example. The country’s strategic heft and non-aligned credibility make it well-placed to bridge different camps. PresidentJoko Widodo made a big political bet on the success of the G20 and has won praise for the deft diplomacy that kept the organization alive and got it to a joint statement.

The Indian delegation reportedly also played a big role in achieving consensus on language in the statement, with the BRICS group (Brazil, Russia, India, China and South Africa)—as well as Indonesia—turning out to be crucial swing voters in securing the joint statement. One Indian official said it was “the first [G20] summit where developing nations shaped the outcome.”

There is scope for this trend to continue next year as middle powers continue to rise in stature, and India and Indonesia take over the presidency of the G20 and ASEAN, respectively. Brazil will host the G20 the year after.

Over in Sharm el-Sheikh at the COP27 UN climate summit, another middle power—the host Egypt—also won praise for helping to shepherd a historic financing deal for poor countries affected by climate change. But the ultimate failure to reach a commitment to phase down fossil fuels was a sobering reminder of the huge difficulties that remain in forging the global consensus needed to overcome our shared challenges.

There is much debate about the effectiveness of Western sanctions, the Ukraine war’s implications for markets and the global economy, and what the West’s next steps should be. While there are few good options, some are clearly worse than others.

On the first question, although the sanctions have been less effective than Europe and the U.S. had hoped, they also are proving more onerous than the Kremlin claims. Russia’s central bank expects GDP to contract by 8-10% this year, while other forecasters expect a larger fall, together with longer-lasting damage to growth potential. Imports and exports have been severely disrupted, and inflows of foreign investment have essentially stopped. Shortages are multiplying, pushing inflation higher. At this point, the country no longer has a properly functioning foreign-exchange market.

The sanctions would have bitten much harder had the West not opted for a carve-out of Russia’s energy sector, and had many more countries joined the U.S. and Europe in the effort. Because that didn’t happen, Russia has not felt nearly as much pressure as it would have. Moreover, it has been able to continue trading through various side and back doors that will likely become increasingly important as long as the sanctions regime, as currently designed, continues.

Nonetheless, it is only a matter of time before the Russian economy experiences a harder hit. Inventories of imported goods – including many critical technological and industrial inputs – are dwindling fast, and many sectors are becoming less resilient. The cumulative damage to Russia’s economy over time will be significant and long-lasting – a fact that has not yet been fully captured by consensus medium-term forecasts.

The second question concerns global spillovers from the war and the sanctions regime. Most observers agree that Russia’s invasion has increased not just energy insecurity but also food insecurity, highlighting the fallout from the war’s disruption to Ukrainian agricultural exports. But there is still much debate about the West’s use of the economic nuclear sanctions option: the curbs placed on Russia’s central bank and on Russia’s use of the international payments system.

These curbs are far more intrusive than the usual mix of restrictions on sanctioned government and private sector trade and on individuals’ financial dealings. Yet, because they are not subject to any internationally agreed standards, guidelines, or checks and balances, they fall outside the purview of relevant global-governance bodies such as the Bank for International Settlements, the International Monetary Fund, and the World Trade Organization.

In a time of war, such oversight might seem like a nicety. But some worry that the sanctions could significantly reduce the dollar’s role as the world’s reserve currency and the U.S.financial system’s role as the primary global intermediary for other countries’ savings and investments. After all, a growing number of countries undoubtedly now feel more vulnerable to the reach of U.S. sanctions.

But it is impossible to replace something with nothing, which means that no significant loss of dollar or U.S. financial primacy will occur in the immediate future. Rather, the sanctions will lend further momentum to the gradual process of global economic fragmentation, which was also fueled a few years ago by the tariffs imposed by the Trump administration. More countries now have even more of a reason to pursue greater financial resilience and inherently inefficient forms of self-insurance.

That brings us to the third debate. With no end in sight for the war, what should the West do next? Fearing the implications for energy prices and the supply of gas to Europe, many in the West are tempted to call for a moratorium on any new sanctions – or even for additional carve-outs. Others, however, favor additional measures to hold Russia accountable for its indiscriminate attacks on Ukrainian civilians.

In any case, maintaining the current sanctions regime is not problem-free, owing to the twin objectives of pressuring Russia and limiting the economic disruption to Europe. Moreover, as European Commission President Ursula von der Leyen recently said, it feels as if Russia is “blackmailing” Europe by threatening to disrupt gas supplies at any moment. No wonder the Commission is urging member countries to cut consumption by 15%.

Doing so would undoubtedly have a severe short-term economic impact on European economies and the rest of the world, amplifying the “little fires everywhere” syndrome that I warned about in May. It is therefore critical that governments use their available fiscal space to provide targeted support to vulnerable segments of the population, as well as to fragile countries; and multilateral agencies must support developing countries through aid and a more operational debt relief framework. If done properly, this option would yield better outcomes in the medium and long term than the current strategy.

Muddling through risks bringing about the worst of all possible worlds. It is insufficient to dissuade Russia from continuing its illegal war; it is fueling deeper fragmentation of the international monetary system; and it is not even protecting Europe from a winter gas disruption.

Today the IMF, European Central Bank, and global economic leaders discussed the future of the economy at the “Global Economic Outlook” session at Davos Agenda 2022.

“In Europe, we are not seeing inflation spiral out of control. We assume energy prices will stabilize from the middle of 2022, bottlenecks will also stabilize in 2022 and gradually, inflation numbers will decline.”

“More recently, we have learnt the lesson of humility–the ECB, IMF, OECD and others all underestimated the recovery, the employment participation and, obviously, inflation.”

“The response to the pandemic crisis has been anything but orthodox— in a highly coordinated manner both central banks and finance authorities have prevented the world falling into yet another great depression.”

“If I were to offer policy makers a new year’s resolution, it would policy flexibility.”

“Japan response to the pandemic has been relatively successful, however, the pandemic has had a significant, negative impact on Japan’s economy.”

“Unlike U.S. or Europe, we have to continue extremely accommodative, easy monetary policy for the time being. We expect the inflation rate in 2022 and 2023 to be around 1 percent still.”

“We see a strong recovery in the Indonesian economy in 2022, and to build on this we are expecting more than 1% of additional GDP growth from a series of recent reforms.”

“Indonesia is the largest economy in the ASEAN region, but it is vulnerable to a dependence on commodities–the emphasis now is on value-added activities.”

About the Davos Agenda 2022

For over 50 years, the World Economic Forum has been the international organization for public-private cooperation. The Davos Agenda 2022 is the focal point at the start of the year for leaders to share their outlook, insights and plans relating to the most urgent global issues. The meeting will provide a platform to accelerate the partnerships needed to tackle shared challenges and shape a more sustainable and inclusive future. Learn more about the program and view sessions live and on demand.

“The wealthy countries must begin providing public climate finance at the scale necessary to support not only adaptation but loss and damage as well, and they must do so in accordance with their responsibility and capacity to act.” This is the main message of a technical report titled “Can Climate Change-Fueled Loss and Damage Ever Be Fair?” launched on the eve of the UN Climate Change Conference (COP25) to be held in Madrid from 2 to 13 December.

The U.S. and the EU owe more than half the cost of repairing future damage says the report, authored by Civil Society Review, an independent group that produces figures on what a “fair share” among countries of the global effort to tackle climate change should look like.

“The poorer countries are bearing the overwhelming majority of the human and social costs of climate change. Consider only one tragic incident—the Cyclones Idai and Kenneth—which caused more than $3 billion in economic damages in Mozambique alone, roughly 20% of its GDP, with lasting implications, not to mention the loss of lives and livelihoods” argues the report. “Given ongoing and deepening climate impacts, to ensure justice and fairness, COP25 must as an urgent matter operationalize loss and damage financing via a facility designed to receive and disburse resources at scale to developing countries.”

The UN Framework Convention on Climate Change (UNFCCC) has defined loss and damage to include harms resulting from sudden-onset events (climate disasters, such as cyclones) as well as slow-onset processes (such as sea level rise). Loss and damage can occur in human systems (such as livelihoods) as well as natural systems (such as biodiversity).

Eight weeks after Hurricane Dorian—the most intense tropical cyclone to ever strike the Bahamas—Prime Minister of Barbados, Mia Amor Mottley, spoke at the United Nations Secretary General’s Climate Action Summit. She said: “For us, our best practice traditionally was to share the risk before disaster strikes, and just over a decade ago we established the Caribbean Catastrophic Risk Insurance Facility. But, the devastation of Hurricane Dorian marks a new chapter for us. Because, as the international community will find out, the CCRIF will not meet the needs of climate refugees or, indeed, will it be sufficient to meet the needs of rebuilding. No longer can we, therefore, consider this as an appropriate mechanism…There will be a growing crisis of affordability of insurance.”

An April 2019 report from ActionAid revealed the insurance and other market based mechanisms fail to meet human rights criteria for responding to loss and damage associated with climate change. The impact of extreme natural disasters is equivalent to an annual global USD$520 billion loss, and forces approximately 26 million people into poverty each year.

Michelle Bachelet, UN High Commissioner for Human Rights, recently warned that the climate crisis is the greatest ever threat to human rights. It threatens the rights to life, health, housing and a clean and safe environment. The UN Human Rights Council has recognized that climate change “poses an immediate and far reaching threat to people and communities around the world and has implications for the full enjoyment of human rights.” In the Paris Agreement, parties to the UN Framework Convention on Climate Change (UNFCCC) acknowledged that they should—when taking action to address climate change—respect, promote and consider their respective obligations with regard to human rights. This includes the right to health, the rights of indigenous peoples, local communities, migrants, children, persons with disabilities and people in vulnerable situations and the right to development, as well as gender equality, the empowerment of women and intergenerational equity. Tackling loss and damage will require a human-rights centered approach that promotes justice and equity.

Across and within countries, the highest per capita carbon emissions are attributable to the wealthiest people, this because individual emissions generally parallel disparities of income and wealth. While the world’s richest 10% cause 50% of emissions, they also claim 52% of the world’s wealth. The world’s poorest 50% contribute approximately 10% of global emissions and receive about 8% of global income. Wealth increases adaptive capacity. All this means that those most responsible for climate change are relatively insulated from its impacts.

Between 1850 and 2002, countries in the Global North emitted three times as many greenhouse gas (GHG) emissions as did the countries in the Global South, where approximately 85% of the global population resides. The average CO2 emissions (metric tons per capita) of citizens in countries most vulnerable to climate change impacts, for example, Mozambique (0.3), Malawi, (0.1), and Zimbabwe (0.9), pale in comparison to the average emissions of a person in the U.S. (15.5), Canada (15.3), Australia (15.8), or UK (6).

In the 1980s, oil companies like Exxon and Shell carried out internal assessments of the carbon dioxide released by fossil fuels, and forecast the planetary consequences of these emissions, including the inundation of entire low-lying countries, the disappearance of specific ecosystems or habitat destruction, destructive floods, the inundation of low-lying farmland, and widespread water stress.

Nevertheless, the same companies and countries have pursued high reliance on GHG emissions, often at the expense of communities where fossil fuels are found (where oil spills, pollution, land grabs, and displacement is widespread) and certainly at the expense of public understanding, even as climate change harms and risks increased. Chevron, Exxon, BP and Shell together are behind more than 10% of the world’s carbon emissions since 1966. They originated in the Global North and its governments continue to provide them with financial subsidies and tax breaks.

Responsibility for, and capacity to act on, mitigation, adaptation and loss and damage varies tremendously across nations and among classes. It must also be recognized that the Nationally Determined Contributions (climate action plans or NDCs) that have thus far been proposed by the world’s nations are not even close to being sufficient, putting us on track for approximately 4°C of warming. They are also altogether out of proportion to national capacity and responsibility, with the developing countries generally proposing to do their fair shares, and developed countries proposed far too little.

Unfortunately, as Kevin Anderson (Professor of Energy and Climate Change at the University of Manchester and a former Director of the Tyndall Centre for Climate Change Research) has said: “a 4°C future is incompatible with an organized global community, is likely to be beyond ‘adaptation,’ is devastating to the majority of ecosystems, and has a high probability of not being stable.”

Equity analysis

The report assess countries’ NDCs against the demands of a 1.5°C pathway using two ‘fair share’ benchmarks, as in the previous reports of the Civil Society Equity Review coalition. These ‘fair share’ benchmarks are grounded in the principle-based claims that countries should act in accordance with their responsibility for causing the climate problem and their capacity to help solve it. These principles are both well-established within the climate negotiations and built into both the UNFCCC and the Paris Agreement.

To be consistent with the UNFCCC’s equity principles—the wealthier countries must urgently and dramatically deepen their own emissions reduction efforts, contribute to mitigation, adaptation and addressing loss and damage initiatives in developing countries; and support additional sustainable actions outside their own borders that enable climate-compatible sustainable development in developing countries.

For example, consider the European Union, whose fair share of the global emission reduction effort in 2030 is roughly about 22% of the global total, or about 8 Gigatons of CO2 equivalent (GtCO2eq). Since its total emissions are less than 5 GtCO2eq, the EU would have to reduce its emissions by approximately 160% per cent below 1990 levels by 2030 if it were to meet its fair share entirely through domestic reductions. It is not physically possible to reduce emissions by more than 100% domestically. So, the only way in which the EU can meet its fair share is by funding mitigation, adaptation and loss and damage efforts in developing countries.

Today’s mitigation commitments are insufficient to prevent unmanageable climate change, and—coming on top of historic emissions—they are setting in motion devastating changes to our climate and natural environment. These impacts are already prevalent, even with our current global average surface temperature rise of about 1°C. Impacts include droughts, firestorms, shifting seasons, sea-level rise, salt-water intrusion, glacial retreat, the spread of vector borne diseases, and devastation from cyclones and other extreme weather events. Some of these impacts can be minimized through adaptation measures designed to increase resilience to inevitable impacts.

These measures include, for example, renewing mangroves to prevent erosion and reduce flooding caused by storms, regulating new construction so that buildings can withstand tomorrow’s severe weather, using scarce water resources efficiently, building flood defenses, and setting aside land corridors to help species migrate. It is also crucial with such solutions that forest dwelling and indigenous peoples be given enforceable land rights, for not only are such rights matters of basic justice, they are also pragmatic recognitions of the fact that indigenous peoples have successfully protected key ecosystems.

Tackling underlying social injustices and inequalities—including through technological and financial transfers, as well as though capacity building—would also contribute to increasing resilience. Other climate impacts, however, are unavoidable, unmanageable or unpredictable, leading to a huge degree of loss and damage. Experts estimate the financial damage also will reach at least USD$300-700 billion by 2030, but the loss of locally sustained livelihoods, relationships and connections to ancestral lands are incalculable.

Failure to reduce GHG emissions now—through energy efficiency, waste reduction, renewable energy generation, reduced consumption, sustainable agriculture and transport—will only deepen impacts in the future. Avoidable impacts require urgent adaptation measures. At the same time, unavoidable and unmanageable change impacts—such as loss of homes, livelihoods, crops, heat and water stress, displacement, and infrastructure damage—need adequate responses through well-resourced disaster response plans and social protection policies.

For loss and damage financing, developed countries have a considerable responsibility and capacity to pay for harms that are already occurring. Of course, many harms will be irreparable in financial terms. However, where monetary contributions can help restore the livelihoods or homes of individuals exposed to climate change impacts, they must be paid. Just as the EU’s fair share of the global mitigation effort is approximately 22% in 2030, it could be held accountable for that same share of the financial support for such incidents of loss and damage in that year.

The table below provides an illustrative quantification of this simple application of fair shares to loss and damage estimates, and how they change if we compute the contribution to global climate change from the start of the industrial revolution in 1850 or from 1950.

Table 1: Countries’ Share of Global Responsibility and Capacity in 2019, the time of Cyclones Idai and Kenneth, as illustrative application of a fair share approach to Loss and Damage funding requirements.

The advantage of setting out responsibility and capacity to act in such numerical terms is to drive equitable and robust action today. Responsible and capable countries must—of course—ensure that those most able to pay towards loss and damage repairs are called upon to do so through domestic legislation that ensures correlated progressive responsibility. However, it should also motivate mitigation action to ensure that harms are not deepened in the future.

In the Equity analysis used here, capacity—a nation’s financial ability to contribute to solving the climate problem—can be captured by a quantitative benchmark defined in a more or less progressive way, making the definition of national capacity dependent on national income distribution. This means a country’s capacity is calculated in a manner that can explicitly account for the income of the wealthy more strongly than that of the poor, and can exclude the incomes of the poorest altogether. Similarly, responsibility—a nation’s contribution to the planetary GHG burden—can be based on cumulative GHG emissions since a range of historical start years, and can consider the emissions arising from luxury consumption more strongly than emissions from the fulfillment of basic needs, and can altogether exclude the survival emissions of the poorest. Of course, the ‘right’ level of progressivity, like the ‘right’ start year, are matters for deliberation and debate.1

The report acknowledges “the difficulties in estimating financial loss and damage and the limited data we currently have,” but it recommends nevertheless “a minimal goal of providing at least USD$300 billion per year by 2030 of financing for loss and damage through the UNFCCC’s Warsaw International Mechanism for Loss and Damage (WIM).” Given that this corresponds to a conservative estimate of damage costs, the report further recommends “the formalization of a global obligation to revise this figure upward as observed and forecast damages increase.”

The new finance facility should provide “public climate financing and new and innovative sources of financing, in addition to budget contributions from rich countries, that can truly generate additional resources (such as air and maritime levies, Climate Damages Tax on oil, gas and coal extraction, a Financial Transaction Tax) at a progressive scale to reach at least USD$300 billion by 2030.” This means aiming for at least USD$150 billion by 2025 and ratcheting up commitments on an annual basis. Ambition targets should be revised based on the level of quantified and quantifiable harms experienced.

Further, developing countries who face climate emergencies should benefit from immediate debt relief–in the form of an interest-free moratorium on debt payments. This would open up resources currently earmarked for debt repayments to immediate emergency relief and reconstruction.

Finally, a financial architecture needs to be set up that ensures funding reaches the marginalized communities in developing countries, and that such communities have decision making say over reconstruction plans. Funds should reach communities in an efficient and effective manner, taking into account existing institutions as appropriate.

Currently, the Paris Rulebook allows countries to count non-grant instruments as climate finance, including commercial loans, equity, guarantees and insurance. Under these rules, the United States could give a USD$50 million commercial loan to Malawi for a climate mitigation project. This loan would have to be repaid at marketinterest rates—a net profit for the U.S.—so its grant-equivalence is $0. But under the Paris Rulebook, the U.S. could report the loan’s face value ($50 million) as climate finance. This is not acceptable. COP25 must ensure that the WIM has robust outcomes and sufficient authority to deliver a fair and ambitious outcome for the poorest and most vulnerable in relation to loss & damage.

Note

For more details, including how progressivity is calculated and a description of the standard data sets upon which those calculations are based, see the referenceproject page. For an interactive experience and a finer set of controls, see the Climate Equity Reference Calculator. (return to text)

The provision of financial services and products is undergoing rapid transformation, including through the development of stablecoins, which seek to stabilize the price of a digital currency by linking its value to that of a pool of assets. Stablecoins can potentially serve as a means of payment and store of value, and may contribute to the development of global payment arrangements that are faster, cheaper, and more inclusive. Yet these potential benefits can only be realized if significant risks are addressed. Stablecoin initiatives built on an existing big tech platform with a global customer base may have the potential to scale rapidly, and could pose regulatory and oversight challenges and risks related to consumer protection, fair competition, and the combating of money laundering and terrorism financing, among others, as well as have a significant impact on public policy goals such as financial stability and monetary policy transmission. This paper, written jointly by G7 members, the BIS, and the IMF, including RESMF staff, scopes the causes and implications of the adoption of global stablecoins, and the potential policy efforts to rein in the risks they can bring about.

We study the optimal design of a central bank digital currency (CBDC) in an environment where agents sort into cash, CBDC and bank deposits according to their preferences over anonymity and security; and where network effects make the convenience of payment instruments dependent on the number of their users. CBDC can be designed with attributes similar to cash or deposits, and can be interest-bearing: a CBDC that closely competes with deposits depresses bankcredit and output, while a cash-like CBDC may lead to the disappearance of cash. Then, the optimal CBDC design trades off bank intermediation against the social value of maintaining diverse payment instruments. When network effects matter, an interest-bearing CBDC alleviates the central bank’s tradeoff.

We estimate world cycles using a new quarterly dataset of output, credit and assetprices assembled using IMF archives and covering a large set of advanced and emerging economies since 1950. World cycles, both real and financial, exist and are generally driven by US shocks. But their impact is modest for most countries. The global financial cycle is also much weaker when looking at credit rather than assetprices. We also challenge the view that synchronization has increased over time. Although this is true for prices (goods and assets), this not true for quantities (output and credit). The world business and credit cycles were as strong during Bretton Woods (1950–1972) as during the Globalization period (1984-2006). For most countries, the way their output co-moves with the rest of the world has changed little over the last 70 years. We discuss the reasons behind these new findings and their policy implications for small open economies.

by Nina Biljanovska, Lucyna Gornicka & Alexandros Vardoulakis

An asset bubble relaxes collateral constraints and increases borrowing by credit-constrained agents. At the same time, as the bubble deflates when constraints start binding, it amplifies downturns. We show analytically and quantitatively that the macroprudential policy should optimally respond to building asset price bubbles non-monotonically depending on the underlying level of indebtedness. If the level of debt is moderate, policy should accommodate the bubble to reduce the incidence of a binding collateral constraint. If debt is elevated, policy should lean against the bubble more aggressively to mitigate the pecuniary externalities from a deflating bubble when constraints bind.

by Senay Agca, Deniz O Igan, Fuhong Li & Prachi Mishra

Why do firms lobby? This paper exploits the unanticipated sequestration of federal budget accounts in March 2013 that reduced the availability of government funds disbursed through procurement contracts to shed light on this question. Following this event, firms with little or no prior exposure to the federal accounts that experienced cuts reduced their lobbying spending. In contrast, firms with a high degree of exposure to the cuts maintained and even increased their lobbying spending. This suggests that, when the same number of contractors competed for a piece of a reduced pie, the more affected firms likely intensified their lobbying efforts to distinguish themselves from the others and improve their chances of procuring a larger share of the smaller overall. These findings are stronger in government-dependent sectors and when there is intense competition. The evidence is more consistent with a rent-seeking explanation for lobbying.

by Deniz O Igan, Hala Moussawi, Alexander F. Tieman, Aleksandra Zdzienicka, Giovanni Dell’Ariccia, Paolo Mauro

We track direct public interventions and public holdings in 1,114 financial institutions over the period 2007–17 in 37 countries based on publicly available information. We use aggregate official data to validate this new dataset and estimate the fiscal impact of interventions, including the value of asset holdings remaining in state hands at end-2017. Direct public support to financial institutions amounted to $1.6 trillion ($3.5 trillion including guarantees), with larger amounts allocated to lower capitalized and less profitable banks. As of end-2017, only a few countries had fully divested the initial support they provided during the crisis. Public holdings were divested faster in better capitalized, more profitable, and more liquid banks, and in countries where the economy recovered faster. In countries where the government stake remained high relative to the initial intervention, private investment and credit growth were slower, financial access, depth, efficiency, and competition were worse, and financial stability improved less.

Over the past three decades, the price of machinery and equipment fell dramatically relative to other prices in advanced and emerging market and developing economies. Using cross-country and sectoral data, we show that the decline in the relative price of tangible tradablecapital goods provided a significant impetus to the capital deepening that took place during the same time period. The broad-based decline in the relative price of machinery and equipment, in turn, was driven by the faster productivity growth in the capital goods producing sectors relative to the rest of the economy, and deeper trade integration, which induced domestic producers to lower prices and increase their efficiency. Our findings suggest an additional channel through which rising trade tensions and sluggish productivity could threaten real investment growth going forward.

We study the impact of bankcredit on firm productivity. We exploit a matched firm-bank database covering all the credit relationships of Italiancorporations, together with a natural experiment, to measure idiosyncratic supply-side shocks to credit availability and to estimate a production model augmented with financial frictions. We find that a contraction in credit supply causes a reduction of firm TFP growth and also harms IT-adoption, innovation, exporting, and adoption of superior management practices, while a credit expansion has limited impact. Quantitatively, the credit contraction between 2007 and 2009 accounts for about a quarter of observed the decline in TFP.

by Antonio Fatás, Atish R. Ghosh, Ugo Panizza & Andrea F Presbitero

Governments issue debt for good and bad reasons. While the good reasons—intertemporal tax-smoothing, fiscal stimulus, and asset management—can explain some of the increases in public debt in recent years, they cannot account for all of the observed changes. Bad reasons for borrowing are driven by political failures associated with intergenerational transfers, strategic manipulation, and common pool problems. These political failures are a major cause of overborrowing though budgetary institutions and fiscal rules can play a role in mitigating governments’ tendencies to overborrow. While it is difficult to establish a clear causal link from high public debt to low output growth, it is likely that some countries pay a price—in terms of lower growth and greater output volatility—for excessive debt accumulation.

by Harald Hau, Peter Hoffmann, Sam Langfield & Yannick Timmer

New regulatory data reveal extensive price discrimination against non-financial clients in the FX derivatives market. The client at the 90th percentile pays an effective spread of 0.5%, while the bottom quarter incur transaction costs of less than 0.02%. Consistent with models of search frictions in over-the-counter markets, dealers charge higher spreads to less sophisticated clients. However, price discrimination is eliminated when clients trade through multi-dealer request-for-quote platforms. We also document that dealers extract rents from captive clients and market opacity, but only for contracts negotiated bilaterally with unsophisticated clients.