It’s almost “un-American” to be honest about the nightmare side of life when you cannot “walk on the sunny side of the street” and operate under all those facile Americanisms about “I’ve got the world on a string…” in all the songs and movie lines.

Film noir is supposed to be an antidote to this “false sunniness” and there’s one classic example that exemplifies this undiscussable nightmare side of life, namely, Detour (1945), directed by Edgar Ulmer.

As a refugee/expat, he understood that life isn’t always “a bowl of cherries” and set out to show this in his films.

In this underrated Ulmer masterpiece, Tom Neal plays a musician, Al Roberts, who gets into a labyrinthian mess via bad luck and some mindless impulsiveness combined. Detour is a kind of “road movie” in hell. With life and the world a kind of hellish school, the protagonist Al Roberts captures the enforced money-madness in everything:

“Money. You know what that is, the stuff you never have enough of. Little green things with George Washington’s picture that men slave for, commit crimes for, die for. It’s the stuff that has caused more trouble in the world than anything else we ever invented, simply because there’s too little of it.”

To this nightmarishness, there’s to be added the irrationality of fate or destiny or karma or luck:

“That’s life. Whichever way you turn, Fate sticks out a foot to trip you.”

“But one thing I don’t have to wonder about, I know. Someday a car will stop to pick me up that I never thumbed. Yes. Fate, or some mysterious force, can put the finger on you or me for no good reason at all.”

[as narrator] “Until then I had done things my way, but from then on something stepped in and shunted me off to a different destination than the one I’d picked for myself.”

Vera comments:

“Life’s like a ball game. You gotta take a swing at whatever comes along before you find it’s the ninth inning.”

Hitchhiking, say, is often hellish and not romantic and usually not a Jack KerouacOn the Road poetic or rhapsodic adventure at all, as Al Roberts explains:

“Ever done any hitchhiking? It’s not much fun, believe me. Oh yeah, I know all about how it’s an education, and how you get to meet a lot of people, and all that. But me, from now on I’ll take my education in college, or in PS-62, or I’ll send $1.98 in stamps for ten easy lessons.”

[voiceover] “It wasn’t much of a club, really. You know the kind. A joint where you could have a sandwich and a few drinks and run interference for your girl on the dance floor.”

Ulmer’s Detour is not exactly a “lowlife movie” but rather an undiscussed dark side to life movie, nor is it “stylishly pessimistic” (like the French “poetical pessimism” movies) but rather a truth-telling exercise that shows stability and permanence and happiness as “living” on thin ice. American “cock-eyed optimism” isn’t always appropriate.

In that sense, Detour is a part of remedial education.

“Globalization” is here. Signified by an increasingly close economic interconnection that has led to profound political and social change worldwide, the process seems irreversible. In this book, however, Harold James provides a sobering historical perspective, exploring the circumstances in which the globally integrated world of an earlier era broke down under the pressure of unexpected events.

James examines one of the great historical nightmares of the twentieth century: the collapse of globalism in the Great Depression. Analyzing this collapse in terms of three main components of global economics—capital flows, trade and international migration—James argues that it was not simply a consequence of the strains of World War I, but resulted from the interplay of resentments against all these elements of mobility, as well as from the policies and institutions designed to assuage the threats of globalism.

Could it happen again? There are significant parallels today: highly integrated systems are inherently vulnerable to collapse, and world financial markets are vulnerable and unstable.

While James does not foresee another Great Depression, his book provides a cautionary tale in which institutions meant to save the world from the consequences of globalization—think WTO and IMF, in our own time—ended by destroying both prosperity and peace.

PresidentTrump’s speech here at the World Economic Forum went over relatively well. That’s partly because Davos is a conclave of business executives, and they like Trump’s pro-business message. But mostly, the president’s reception was a testament to the fact that he and what he represents are no longer unusual or exceptional. Look around the world and you will see: Trump and Trumpism have become normalized.

Davos was once the place where countries clamored to demonstrate their commitment to opening up their economies and societies. After all, these forces were producing global growth and lifting hundreds of millions out of poverty. Every year, a different nation would become the star of the forum, usually with a celebrated finance minister who was seen as the architect of a boom. The United States was the most energetic promoter of these twin ideas of economic openness and political freedom.

Today, Davos feels very different. Despite the fact that, throughout the world, growth remains solid and countries are moving ahead, the tenor of the times has changed. Where globalization was once the main topic, today it is the populist backlash to it. Where once there was a firm conviction about the way of the future, today there is uncertainty and unease.

This is not simply atmospherics and rhetoric. Ruchir Sharma of Morgan Stanley Investment Management points out that since 2008, we have entered a phase of “deglobalization.” Global trade, which rose almost uninterruptedly since the 1970s, has stagnated, while capital flows have fallen. Net migration flows from poor countries to rich ones have also dropped. In 2018, net migration to the United States hit its lowest point in a decade.

It’s important not to exaggerate the backlash to globalization.

As a 2019 report by DHL demonstrates, globalization is still strong and, by some measures, continues to expand. People still want to trade, travel and transact across the world. But in government policy, where economic logic once trumped politics, today it is often the reverse. EconomistNouriel Roubini argues that the cumulative result of all these measures — protecting local industries, subsidizing national champions, restricting immigration — is to sap growth. “It means slower growth, fewer jobs, less efficient economies,” he told me recently. We’ve seen it happen many times in the past, not least in India, which suffered decades of stagnation as a result of protectionist policies, and we will see the impact in years to come.

This phase of deglobalization is being steered from the top. The world’s leading nations are, as always, the agenda-setters. The example of China, which has shielded some of its markets and still grown rapidly, has made a deep impression on much of the world. Probably deeper still is the example of the planet’s greatest champion of liberty and openness, the United States, which now has a president who calls for managed trade, more limited immigration and protectionist measures. At Davos, Trump invited every nation to follow his example. More and more are complying.

Students should sense that while history does not repeat itself, it sometimes rhymes and this is a major danger. It also might imply that coping with climate change will be all the harder because American-led unilateralism everywhere would mean world policy paralysis.

Louise Brooks is a rebellious 15-year-old schoolgirl who dreams of fame and fortune in the early 1920s. She soon gets her chance when she travels to New York to study with a leading dance troupe for the summer—accompanied by a watchful chaperone.

Upon Louise’s “induction” into the school, one of the founders says to the girls, “Remember you are not in your body, your body is in you.”

The listener wonders: What could this possibly mean?

The answer is this: In one sense you have a body, but in another, you are your body. The first body is the “thing” you weigh on the bathroom scale. This is your interaction with gravity, as measured in conventions like pounds. On the other hand, you are also “somebody” (i.e., some body). To have and to be are entwined here. In philosophy, say in the writings of Gabriel Marcel during the fifties, the body you weigh is “corporeal” and the body you are is “existential.”

Very roughly, the first body is objectively weighed, the second subjectively sensed as your experience of yourself.

The student will see that a moment in a movie—in this case The Chaperone—can open a door to a whole set of domains, realms and phenomena. Education at its best comes from learning how to go from such instantaneous accidents on the street or screen to a larger canvas.

Thus the declaration, “Remember you are not in your body, your body is in you” explains that biomechanics is an infrastructure, while the artistry of the dance is an art form (i.e., a kind of “communicative action,” to use a Habermas phrase).

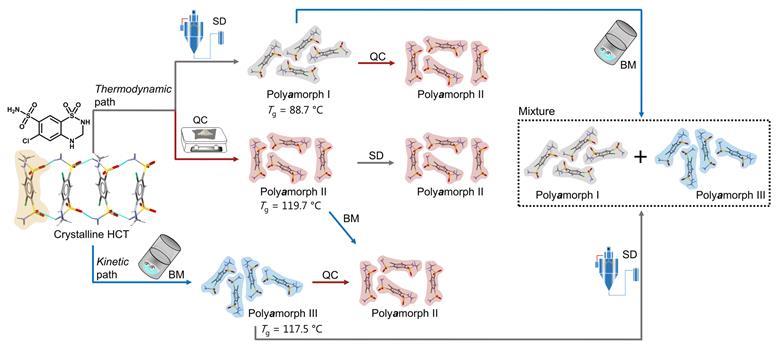

Results from a study combining experiments and simulations could overturn the assumption that amorphous forms of the same compound have the same molecular arrangement. The team behind the work claims to have prepared three amorphous forms of the diureticdrughydrochlorothiazide and determined that they have distinct properties and distinct types of disorder. ‘If polyamorphism is proved in the future to be a universal—or at least not a very rare—phenomenon, then the pharmaceutical industry will need to make screens for polyamorphism and this will also be an opportunity for patenting,’ comments Inês Martins, from the University of Copenhagen in Denmark, who led the work with Thomas Rades.

Crystallineactive pharmaceutical ingredients (APIs) often suffer from poor solubility. A common strategy to circumvent this problem is converting APIs into their amorphous form. This has been demonstrated for various APIs, including hydrochlorothiazide. However, the physical properties of polyamorphs are dependent on how they were prepared. Given there are no straightforward techniques to study how molecules interact and organise themselves in amorphous materials, the area is poorly understood.

‘The problem out of the gate with polyamorphism as a concept is how to tell the difference between a well-defined metastableamorphous structure and an unrelaxed one that simply results from kinetically trapped defects introduced during processing. This is hard to define since the amorphousstructure is statistical in any case,’ comments Simon Billinge, who studies the structure of disordered materials at Columbia University in the US. ‘They process the samples very differently. We know—from our own work—that this results in amorphous phases with very different stabilities against recrystallisation, for example, but is this polyamorphism? On the other hand, they find that the pair distribution functions of each of their “forms” are identical. There is no experimental evidence for a distinct structure. Taken together, the results do little to advance my understanding of polyamorphism.’

The team also says the simulations corroborated its experimental results that polyamorph I can transform into polyamorph II, while the opposite conversion did not take place.

In October, I wrote about the potential for standards to make business-to-business payments more efficient. Today, let’s talk about standards again, this time for money transfer businesses and the state regulations covering them.

For new and established money transfer businesses and for state regulators, the hodgepodge of state regulations creates headaches. To do business everywhere in the United States, money transfer businesses must register separately in each state and US territory and meet license requirements that can vary from state to state. They can face multiple state examinations, also with different requirements, simultaneously (and annually). During examinations, regulators review operations, financial condition, management, and compliance with anti-money laundering laws.

Fortunately, many states have acted to address this confusing and inefficient situation by adopting the Model Money Transmission Modernization Act (MTMA) [archived PDF], sample legislation developed by the Conference of State Bank Supervisors to establish nationwide standards and requirements for licensed money transmitters. Fourteen states have adopted some version of the MTMA: Arizona, Arkansas, Georgia, Hawaii, Indiana, Iowa, Minnesota, Nevada, New Hampshire, North Dakota, South Dakota, Tennessee, Texas, and West Virginia. In my home state of Massachusetts, the legislature’s Joint Committee on Financial Services heard testimony on a version of this bill just last month. For traditional money transmitters and new fintech entrants, the MTMA aims to reduce the substantive and technical differences among the various state laws and regulations. This kind of change has the potential to reduce compliance burdens, encourage innovation, and remove barriers to entry for new market participants.

The MTMA is important given the prodigious growth in person-to-person, or P2P, payments via apps. Among all USconsumers, half of P2P payments were sent using noncash methods in 2022, up from less than 30 percent in 2020 (see the chart). From Massachusetts alone, money transmitters sent $31 billion in 2022, according to the state’s Division of Banks.

Half of P2P payments were made electronically in 2022.

The MTMA also has the potential to create efficiencies for state supervisors. For example, the Conference of State Bank Supervisors (CSBS) has facilitated a collaborative exam program for nationwide payments and cryptocurrency firms to undergo one exam, each facilitated by one state overseeing a group of examiners sourced from across the country. According to the CSBS, transmitters in more than 40 states that have laws addressing core precepts can benefit from the streamlined exams.

The MTMA is another example showing that standards create efficiencies that are good for businesses, good for regulators and, by extension, good for consumers.

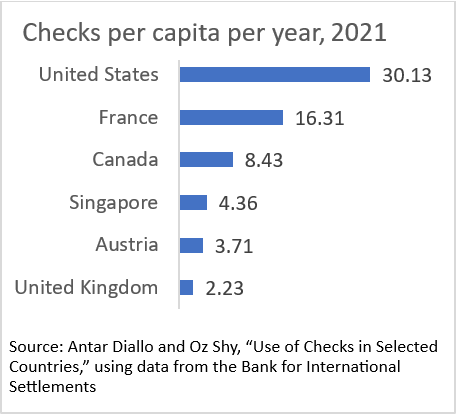

Among the 20 countries that reported the number and value of these payments to the BIS, the United States had by far the highest per capita use of checks per year in 2021: 30 checks. Only six countries reported more than two per capita (chart below), another 12 between zero and two. Belgium and South Africa reported zero.

Given the high per capita use in the United States, it makes sense that our year-over-year decline from 2012 has been slower than that for other countries. The per-year decline in the number of U.S.checks from 2012 to 2021 was slower than the decline for all the other high-use countries listed in the chart. The United States was down 6.7 percent per year from 2012 to 2021, compared to down 8.8 percent per year for Canada at the slow end and down 17.4 percent per year for Austria at the quick end.

No way around it: we love our checks, and our response to innovation has been tepid compared to that of other countries.

Several movies give you an “enchanting” back door or window into chemistry so that you can “beat” the tediousness of regular education and come into the field and its topics via these movies:

I.

The Man in the White Suit is a 1951 British comedy classic with Alec Guinness as a genius research chemist. He fiddles with his flasks and polymer and textile chemistry experiments until he invents a fabric that shows no wear and tear “forever.” This would seem like a great boon to humanity in its clothing needs but the chemist (“Sidney Stratton”) finds that both labor and management reject his discovery violently as it threatens jobs and profits. Textile or fabric polymer chemistry is at the heart of the plot.

RDX was used by both sides in World War II. The U.S. produced about 15,000 long tons per month during WWII and Germany about 7,000 long tons per month. RDX had the major advantages of possessing greater explosive force than TNT, used in World War I and requiring no additional raw materials for its manufacture.

Semtex was developed and manufactured in Czechoslovakia, originally under the name B 1 and then under the “Semtex” designation since 1964, labeled as SEMTEX 1A, since 1967 as SEMTEX H, and since 1987 as SEMTEX 10. Originally developed for Czechoslovakmilitary use and export, Semtex eventually became popular with paramilitary groups and rebels or terrorists because prior to 2000 it was extremely difficult to detect, as in the case of Pan Am Flight 103.

A suspicious device resembling those used in the bombings was found and defused in an apartment block in the Russian city of Ryazan on 22 September. On 23 September, Vladimir Putin praised the vigilance of the inhabitants of Ryazan and ordered the air bombing of Grozny, which marked the beginning of the Second Chechen War. Three FSB agents who had planted the devices at Ryazan were arrested by the local police, with the devices containing a sugar-like substance resembling RDX.

We are told that on an evening in 1889, Mr. Holmes was seated in 221B Baker Street at the deal table loaded with retorts and test tubes. He was settling down to one of those all-night chemical researches in which he frequently indulged.

The research work was interrupted by a message of distress from Violet Hunter. Watson found that there was a train the next morning, and Holmes tells Watson:

“That will do very nicely. Then perhaps I had better postpone my analysis of the acetones as we may need to be at our best in the morning.”

“In the fractional distillation of coal-tar, the distillate separates into five distinct groups or layers, depending upon the stage of the process and the amount of heat applied. Category-one of the five includes benzene, toluene, xylenes and cumenes.

“Be open, open, and more open,” especially to businesses, investors, media, universities, and research institutions. And tit-for-tat doesn’t work, the professor says.

Professor Zheng Yongnian (郑永年), the Founding Director of the Institute for International Affairs at the Chinese University of Hong Kong, Shenzhen, on January 28 published an article on how China should address Western public opinion on China. His advice is in the last part of the article, and below is a translation.

First, we need to understand how such narratives are formed. Historically, China held a bias due to its self-isolation and limited knowledge of the West. Despite losing the two Opium Wars, Chinese intellectuals at that time still saw Westerners as uncivilized. It was not until China was defeated by Japan, a neighboring country once considered as China’s student, that they realized their ignorance and a need for reform. Before China’s Reform and Opening up, Chinese people barely knew anything about the West. They always assumed Westerners were in deep distress, repeating the same lack of understanding of the West.

Similarly, the West’s uncertainty and fear towards China’s rise stem from a lack of understanding and even fear of the country, and their ingrained ideology would lead to misconceptions.

China is the world’s second-largest economy. The externalities and influence of its economy on the West are obvious. Upon joining the WTO, some Chinese people also felt unsettled by the externalities of the West. Some said, “the wolf is coming.” Now it is the West that is experiencing such worries.

It is crucial to recognize the significant impact of the Western hypocritical narratives against China, even if they are based on ideology rather than facts. We must also acknowledge that ideology-based public opinion from the West can exert a powerful influence on their policies toward China.

Historically, the West tended to demonize others while presenting themselves as morally superior, which enabled them to apply Social Darwinism to international politics easily and thus legitimizing conflicts and even wars with other nations. Given the Soviet Union’s failure in the ideological arena during the Cold War, we should by no means ignore any ideology-based public opinion toward China from the West.

Second, to make rational responses to the Westernideology-based criticisms, we should draw lessons from the history of the world economy, such as the lessons of the Soviet Union, as well as our practices, such as the rhetorical battle with the West in the past few years. Coming up with an externally-facing public opinion based on a different ideology is not the most effective in addressing public opinion attacks based on an ideology. Empirically, tit-for-tat is ineffective and can worsen the situation. Again, the failure of the Soviet Union is a prime example, as its battle with a Westernideology failed. When faced with China-demonizing based on ideology from the West, we need to do the simplest thing, namely resorting to facts, science, and reason.

Third, and most importantly, China needs to prioritize its sustainable development, which ultimately benefits the country itself. It is important to recognize that the foundation of the government’s governance lies in its citizens, not Western praise. The support from its people is crucial for both the nation’s longevity and stability., China’s sustainable development also benefits the world economy by boosting its growth. As mentioned above, China has been the largest contributor to the growth of the world economy since it joined the WTO.

It is crucial to prioritize the building of a knowledge system based on China’s practical experiences. Regarding global soft power, we need a knowledge system based on our experiences rather than a certain ideology. While there has been a proposal for an autonomous knowledge system, continuous effort is still required.

Fourth, given the substantial externalities of our economy, we must further communicate and coordinate with other countries on economic policies, regardless of their respective sizes. Our duty is to fulfill the responsibility as a major player in the international community, which also benefits China.

Fifth, we must be open, open, and more open. Despite China’s efforts, there remains a persistent ideological camp in the West that views China through an ideological lens, a situation made worse by the past three years of the pandemic. The pandemic was so severe that it hindered travel across borders; as a result, some Western media and scholars tend to assess China through ideology since they couldn’t come here to see the facts with their own eyes.

The assessment of China through a uniform ideological lens appears to have strengthened the original Westernideological camp. However, the United States and the West have more than one ideology, and not all people believe in the prevailing ideology in the public opinion sphere. China’s openness provides a “seeing is believing” opportunity for different groups in the West. China should increase its openness to Western groups, including businesses, investors, media, universities, and research institutions. The changes in their understanding could render those ideological-based public opinions less effective.

“If you raise [the development of the BRI] to the strategic level, there are countries where … you will have to lose money and there are countries where you will be free to make money.”

How to respond to the growing political divide between China and the West marked by partial decoupling, security alliances, and the risk of sanctions, amongst other things, continues to be a major topic of discussion among China’s intellectual elite. As already evidenced in previous editions of this newsletter, opinions vary considerably. Those presented here so far have ranged from Da Wei (达巍) stressing the importance of preserving if not strengthening ties with the West and Shen Wei (沈伟) arguing in favor of reforming the WTO and building up a network of free trade agreements to Ye Hailin (叶海林) emphasizing the need for China to demonstrate its military might to demobilize U.S. allies and Lu Feng (路风) calling for self-reliance and greater assertiveness in the field of tech. A certain amount of overlap certainly exists among these perspectives but the differences are nonetheless striking.

Today’s edition of Sinification looks at a speech made last month by Yang Ping (杨平), head and editor-in-chief of the highly regarded Beijing Cultural Review (文化纵横, hereafter BCR). Yang is also director of the Longway Foundation (修远基金会) which publishes BCR. The foundation describes its publication as “the most influential magazine of intellectual thought and commentary in China” and sees itself as having a key role in helping shape the direction of intellectual debates in China (“议题的设置就是意识形态斗争成功的一半”). Indeed, BCR often republishes old articles at key junctures as so often highlighted by David Ownby’s wonderful Reading the China Dream.

The following are excerpts from an edited transcript of a speech by Yang made at an event hosted by Renmin University’s Chongyang Institute for Financial Studies, which was attended by China’s Vice-minister of foreign affairs Xie Feng (谢锋). In his speech, Yang advocates building a new international system led by countries in the Global South (which, of course, includes China) rather than the West. His ideas are not particularly novel but are nevertheless noteworthy in that they represent yet another viewpoint in the ongoing debate over how China should respond to the increasing tensions that characterize its relations with the U.S. and other Western countries. Next week, I will be sharing a somewhat longer piece that proposes a way of protecting China from the growing threat of Westernsanctions.

China must respond to this growing trend by building a “new type of international system” with other countries in the Global South.

BRI projects should be increasingly focused on achieving this goal and thus allow more room for loss-making endeavors.

Capitalist politics ≠ Capitalist economics

“Since 2022 and the Russo-Ukrainian conflict, our main focus and topic of discussion has been China’s construction of a new type of international system.

“We have witnessed two typical manifestations of the separation of politics and the economy and the impact of politics on the economy:

The first is the conflict between Russia and Ukraine. The sanctions imposed on Russia by the United States and the West have reached unthinkable, abominable [令人发指] and unimaginable proportions. Under established international rules, it was understood that such sanctions could not possibly occur, but now they have. These include the fracturing of the financial system, the expropriation and seizure of Russian private assets and the freezing of Russianforeign exchange reserves. These are all abominable and unimaginable forms of confrontation. At the same time, the Russo-Ukrainian conflict has led to serious disruptions in global food and energy systems and supply chains, with massive food ‘shortages’ and soaring food prices, particularly in developing countries. Sanctions and political repression [政治打压] have severely disrupted the [world’s] economic order.

The second is the conflict between the U.S. and China. Since the Trump era, the U.S. has been engaged in a trade war against China, mainly by raising tariffs. Basically, this was simply about balancing trade [with China] and used mainly economic means. But under Biden, it [has become] a war that mixes politics with economics. Biden’s strategy towards China can basically be summed up in just a few words: one, friend-shoring, [i.e.] only allowing friendly countries into [parts of] its supply chains; two, alliancepolitics, [i.e.] continuously forging an alliance system involving NATO, the European Union, Japan, AUKUS and the four Asia-Pacific countries [I assume he is referring to South Korea, Japan, New Zealand and Australia taking part for the first time in a NATO summit last year] and constantly opposing China [不断应对中国]; three, its so-called ‘precision strikes’, [i.e.] its radical crackdown on China’s high tech [industry], especially our chip industry.”

China is being pushed out of the U.S.-led international system

“The information I have seen so far is that the number of Chinese companies included in the U.S.’s ‘entity list’ has risen from 132 under Trump to over 530 now. The scope of such point-to-point [点对点] precision strikes is constantly expanding. With such a political impact on the economy, we can feel the [world’s] economic order being disrupted across the board. The world is moving inexorably in the direction of decoupling. The phenomenon of politics affecting the economy and the capitalistpolitical order no longer upholding the capitalisteconomic order are extremely striking.

“In such a context, the challenges now facing China are extremely serious and varied. We have the pressures of dealing both with containment in the Indo-Pacific and with the U.S.-led politics of alliances across the world. More importantly and fundamentally China faces the strategic task of building a new type of international system [新型国际体系] … The existing Western-dominated international system used to be one in which we tried hard to blend [so as] to become one with it. During this process, we [sought to] absorb the West’s advanced technologies and management [practices] and thus complete our mission of industrialisation and modernization.

“But once you enter the existing international system, he [who is already inside] does not want to play with you, and even wants to drive you back out. He wants to divide both supply chains and the economic system into two parts [搞成两套] and desperately wants to contain and suppress you. This is not something that can be determined by your own subjective preferences. He has made up his mind: you have already become his ‘fated opponent’ [命定的对手]. He has to suppress you and drive you out of the existing system.”

Building a new international system with the Global South

“It is at this point that China is faced with the task of constructing a new type of international system that is not dominated by the West. In today’s so-called strategic quadrangle consisting of the U.S., Europe, Russia and China, how to construct such an international system appears particularly difficult [逼庂 literally means ‘narrow’ or ‘cramped’ rather than ‘difficult’].

“But if we look a little further south, we will find a vast number of developing countries, the Third World and the countries of the global South. They should be our strategy’s depth [我们的战略纵深]. That is to say, [we should] build a new type of international relations and a new type of international system that has strategic depth and in which China and the countries of the global South are jointly integrated. [This] is, in my view, an important strategic task for China’s international relations in the coming decades.”

BRI projects: Strategy trumps profitability

“For China today, especially for businesses and governments at all levels [within China] that are currently working hard to develop BRI trade, there is a very important point to which they should be alerted or reminded about: the development of the BRI has to go beyond mere business, beyond the general export of [China’s excess] production capacity, beyond the partial thinking of industry and the partial thinking at the regional level, or the simple economic way of thinking of business. The development of the BRI should be considered at the strategic level. That is, it should be included into China’s strategy when thinking about Africa, South America, Southeast Asia and Central Asia.

“If you raise [the development of the BRI] to the strategic level, there are countries where you won’t be able to make money and will have to lose money, and there are countries where you will be free to make money. You have to unite the two within your organic strategy.

“The strategic task of building a new type of international system is, in my view, a strategic proposition that Chinesethink tanks and research institutes should pay very close attention to with regards to international relations.

“Time is limited today. I just wanted to make a start here. I hope to receive your corrections and criticisms. Thank you!”

The recessive importance of the Global South was previously explored by Richard and his partner Larry, with input from Supratik Bose, many decades ago as shown here.

“We’ve had a time of red-hot housing market all over the country… Shelter inflation is going to remain high for some time. We’re looking for it to come down, but it’s not exactly clear when that will happen. Hope for the best, plan for the worst.”

The rapid run-up of shelter costs—both house prices and rents—during the recovery from the pandemic has raised questions about how inflation pressures might affect housing affordability. Since March 2022, the Federal Reserve has rapidly lifted its federal funds rate target from near zero to over 4%, and policymakers have signaled that they are open to keeping the monetary policy stance sufficiently restrictive to return inflation to the longer-run goal of 2% on average. The tightened financial conditions following those policy changes, especially the surge in mortgageinterest rates, have helped cool house price growth. However, rentinflation remains elevated.

This Economic Letter examines the effectiveness of monetary policy tightening for reducing rentinflation. We estimate that, during the period from 1988 to 2019, a policy tightening equivalent to a 1 percentage point increase in the federal funds rate can reduce rentinflation—measured by 12-month percentage changes in the personal consumption expenditures (PCE)housing price index—by about 3.2 percentage points, but the full impact takes about 2½ years to materialize. Based on housing costs’ share in total PCE, this translates to a reduction in headline PCEinflation of about 0.5 percentage point over the same time horizon.

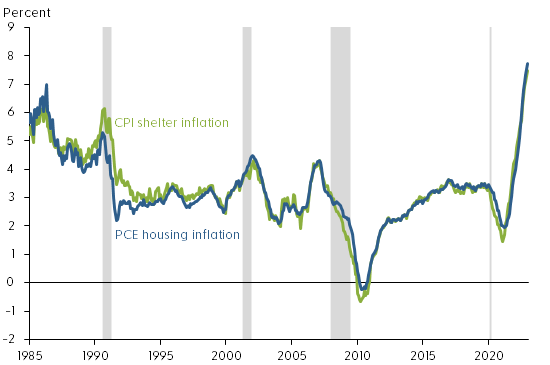

Rentinflation also accelerated during the pandemic period. Figure 1 shows that rentinflation—measured using 12-month changes in the PCEhousing price index and including rents for tenant-occupied housing and imputed rents for owner-occupied housing—rose from a low point of about 2% in early 2021 to 7.7% by December 2022, the highest level since 1986. During the same period, rentinflation measured by 12-month changes in the shelter component of the consumer price index (CPI) experienced a similar increase. Thus, following the tightening of monetary policy, house price growth has slowed but rentinflation continues to rise.

Economic theory suggests that some common forces such as changes in housing demand can drive both rents and house prices. For example, the expansion of remote work since the COVID-19 pandemic has increased demand for housing, raising both house prices and rents (Kmetz, Mondragon, and Wieland 2022). To the extent that the stream of current and future rents reflects the fundamental value of a house, house prices can be a leading indicator of future rentinflation (Lansing, Oliveira, and Shapiro 2022). Thus, monetary policy can affect both house prices and rents by cooling housing demand.

Housing demand responds to changes in financial conditions, such as increases in mortgageinterest rates. However, theory suggests that house prices are more sensitive than rental prices to changes in financial conditions, because home purchases typically require longer-term mortgage financing. In addition, unlike rents, house prices can be partly driven by investor sentiments or beliefs, which explains the observed larger swings in house prices than in rents over business cycles (Dong et al. 2022). Long-term rental contracts can also contribute to slow adjustments in rentinflation.

Rentinflation is an important contributor to overall inflation because housing costs are an important component of total consumption expenditures. On average, housing expenditures represent about 15% of total PCE and 25% of the services component of PCE. In CPI, shelter costs represent an even larger share, accounting for about 30% of total consumption of all urban consumers and about 40% of core consumption expenditures excluding volatile food and energy components.

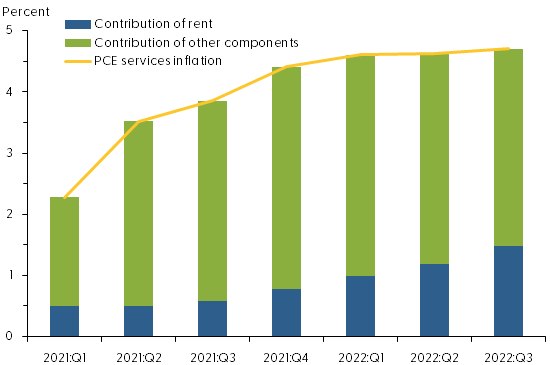

The contribution of rentinflation to overall PCEinflation has increased since early 2021. As Figure 2 shows, in the first quarter of 2021, rentinflation accounted for about 22% of the four-quarter change in the PCE services price index, excluding energy: 0.5 of the 2.3 percentage points increase in service prices was attributable to rentinflation. By the third quarter of 2022, the contribution of rentinflation had climbed to about one-third, or 1.5 of the 4.7 percentage point increase in service prices.

Figure 2: Rising contribution of rent inflation to services inflation

For our analysis, we use a measure of monetary policy surprises constructed by Bauer and Swanson (2022). Their measure focuses on high-frequency changes in financial marketindicators within a short period surrounding the Federal Open Market Committee (FOMC) policy announcements. If the public fully anticipates a policy change, then the financial market would not react to new policy announcements. However, if the market does react to an announcement, then the policy change must contain a surprise element. Thus, changes in financial marketindicators, such as the price of Eurodollar futures, in a narrow window around an FOMC announcement can capture policy surprises. In practice, however, the data constructed this way are not complete surprises because they can be predicted by some macro and financial variables shortly before FOMC announcements. We follow the approach of Bauer and Swanson (2022) to purge the influences of those macro and financial variables from the measure of policy surprises. We use the resulting quarterly time series to measure monetary policy shocks, with a sample period from 1988 to 2019.

We then use a local projections model—a statistical tool proposed by Jordà (2005)—to project how rentinflation responds over time to a tightening of monetary policy equivalent to a 1 percentage point unanticipated increase in the federal funds rate in a given quarter. The model takes into account how monetary policy shocks interact with other macroeconomic variables, including lags of rentinflation, real GDP growth, and core PCEinflation.

In the final step, we compute the responses of rentinflation relative to its preshock level over a period up to 20 quarters after the initial increase in the federal funds rate.

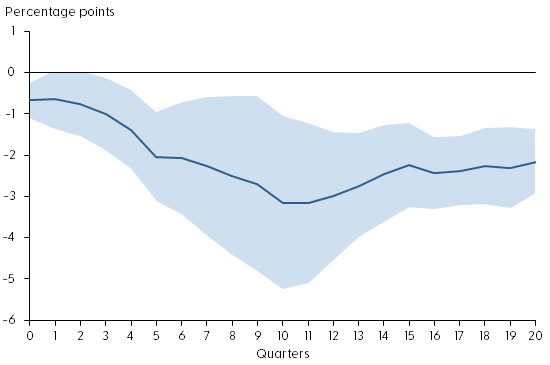

Gradual impact of policy tightening on rent inflation

Figure 3 shows the response of rentinflation during the first 20 quarters after an unanticipated tightening of monetary policy (solid blue line). The shaded area shows the confidence band, indicating the statistical uncertainty in estimating the responses. Under the assumption that the model is correct, the shaded area contains the actual value of the rentinflation responses to the monetary policy shock roughly two-thirds of the time. The policy shock is normalized such that it is equivalent to a 1 percentage point unanticipated increase in the federal funds rate.

Figure 3: Response of rent inflation to monetary policy tightening

Source: Bureau of Economic Analysis, Bauer and Swanson (2022), and authors’ calculations. Note: Response of rentinflation to a monetary policy shock equivalent to a 1 percentage point surprise increase in the federal funds rate. Shaded region shows 68% confidence band around the estimate.

The figure shows that monetary policy tightening has significant and gradual effects on rentinflation. On impact, a 1 percentage point increase in the federal funds rate reduces rentinflation about 0.6 percentage point relative to its preshock level. Over time, rentinflation declines gradually, falling about 3.2 percentage points in the 10 quarters following the impact. The slow adjustment in rentinflation partly reflects the stickiness in nominal rents due to long-term rental contracts. Since housing expenditures account for about 15% of total PCE, this estimate translates to a reduction in headline PCEinflation of about 0.5 percentage point, stemming from the decline in rentinflation over a period of 2½ years.

The rent component of PCE is measured based on average rents, including those locked in long-term rental contracts, which are slow to adjust to changes in economic and financial conditions. Rents on new leases, however, are more flexible. For example, the 12-month growth in Zillow’s observed rent index, which measures changes in asking rents on new leases, has slowed significantly since March 2022 (see Figure 4). Asking rents are typically a leading indicator of future average rents. Thus, the slowdown in asking rent growth could portend lower future rentinflation.

Figure 4: Year-over-year observed rent growth starting to slow

Source: Zillow and Haver Analytics. Note: Twelve-month percentage changes in Zillow’s observed rent index. Gray shading indicates NBER recession dates.

Conclusion

Rents are an important component of consumer expenditures. Recent surges in rentinflation have led to concerns that overall inflation might stay persistently high despite tightening of monetary policy. We present evidence that monetary policy tightening is effective for reducing rentinflation, although the full impact takes time to materialize. A policy tightening equivalent to a 1 percentage point increase in the federal funds rate can reduce rentinflation up to 3.2 percentage points over the course of 2½ years. This translates to a maximum reduction in headline PCEinflation of about 0.5 percentage point over the same time horizon. Although average rents are slow to respond to policy changes, growth of asking rents on new leases has started to slow following recent monetary policy tightening. Our finding suggests that this tightening will gradually bring rentinflation down over time, thereby helping to reduce overall inflation.