There were significant downward contributions by many of the factors, with the largest negative contributions from European Area delivery times, European Area backlogs, and Taiwanese purchases.

The GSCPI’s recent movements suggest that global supply chain conditions have largely normalized after experiencing temporary setbacks around the turn of the year.

The GSCPI compiles more than two dozen metrics across seven economies—data on global transportation costs and regional manufacturing conditions—to track shifts in supply chain pressures from 1997 to the present.

The GSCPI is updated regularly at 10 AM ET on the fourth business day of each month.

On April 5, the GDPNow model estimate for real GDP growth in the first quarter of 2023 is 1.5 percent, down from 1.7 percent on April 3.

The next GDPNow update is Monday, April 10.

Want to see even more economic data? The Atlanta Fed’s EconomyNow app will put GDPNow and all its data tools right in your hands. Download it today to see the latest data on inflation, growth, and the labor market.

“Be open, open, and more open,” especially to businesses, investors, media, universities, and research institutions. And tit-for-tat doesn’t work, the professor says.

Professor Zheng Yongnian (郑永年), the Founding Director of the Institute for International Affairs at the Chinese University of Hong Kong, Shenzhen, on January 28 published an article on how China should address Western public opinion on China. His advice is in the last part of the article, and below is a translation.

First, we need to understand how such narratives are formed. Historically, China held a bias due to its self-isolation and limited knowledge of the West. Despite losing the two Opium Wars, Chinese intellectuals at that time still saw Westerners as uncivilized. It was not until China was defeated by Japan, a neighboring country once considered as China’s student, that they realized their ignorance and a need for reform. Before China’s Reform and Opening up, Chinese people barely knew anything about the West. They always assumed Westerners were in deep distress, repeating the same lack of understanding of the West.

Similarly, the West’s uncertainty and fear towards China’s rise stem from a lack of understanding and even fear of the country, and their ingrained ideology would lead to misconceptions.

China is the world’s second-largest economy. The externalities and influence of its economy on the West are obvious. Upon joining the WTO, some Chinese people also felt unsettled by the externalities of the West. Some said, “the wolf is coming.” Now it is the West that is experiencing such worries.

It is crucial to recognize the significant impact of the Western hypocritical narratives against China, even if they are based on ideology rather than facts. We must also acknowledge that ideology-based public opinion from the West can exert a powerful influence on their policies toward China.

Historically, the West tended to demonize others while presenting themselves as morally superior, which enabled them to apply Social Darwinism to international politics easily and thus legitimizing conflicts and even wars with other nations. Given the Soviet Union’s failure in the ideological arena during the Cold War, we should by no means ignore any ideology-based public opinion toward China from the West.

Second, to make rational responses to the Westernideology-based criticisms, we should draw lessons from the history of the world economy, such as the lessons of the Soviet Union, as well as our practices, such as the rhetorical battle with the West in the past few years. Coming up with an externally-facing public opinion based on a different ideology is not the most effective in addressing public opinion attacks based on an ideology. Empirically, tit-for-tat is ineffective and can worsen the situation. Again, the failure of the Soviet Union is a prime example, as its battle with a Westernideology failed. When faced with China-demonizing based on ideology from the West, we need to do the simplest thing, namely resorting to facts, science, and reason.

Third, and most importantly, China needs to prioritize its sustainable development, which ultimately benefits the country itself. It is important to recognize that the foundation of the government’s governance lies in its citizens, not Western praise. The support from its people is crucial for both the nation’s longevity and stability., China’s sustainable development also benefits the world economy by boosting its growth. As mentioned above, China has been the largest contributor to the growth of the world economy since it joined the WTO.

It is crucial to prioritize the building of a knowledge system based on China’s practical experiences. Regarding global soft power, we need a knowledge system based on our experiences rather than a certain ideology. While there has been a proposal for an autonomous knowledge system, continuous effort is still required.

Fourth, given the substantial externalities of our economy, we must further communicate and coordinate with other countries on economic policies, regardless of their respective sizes. Our duty is to fulfill the responsibility as a major player in the international community, which also benefits China.

Fifth, we must be open, open, and more open. Despite China’s efforts, there remains a persistent ideological camp in the West that views China through an ideological lens, a situation made worse by the past three years of the pandemic. The pandemic was so severe that it hindered travel across borders; as a result, some Western media and scholars tend to assess China through ideology since they couldn’t come here to see the facts with their own eyes.

The assessment of China through a uniform ideological lens appears to have strengthened the original Westernideological camp. However, the United States and the West have more than one ideology, and not all people believe in the prevailing ideology in the public opinion sphere. China’s openness provides a “seeing is believing” opportunity for different groups in the West. China should increase its openness to Western groups, including businesses, investors, media, universities, and research institutions. The changes in their understanding could render those ideological-based public opinions less effective.

Conflict, supply disruption, rising prices, and shortages are all impacting food supplies globally. Just as we are nearing some form of recovery from the pandemic, we are now facing another global challenge in the form of a food crisis – and it’s likely to get worse.

This is a regional problem that cannot be solved by individual economies acting on their own. It must be looked at with a wider lens, such as through bodies, like APEC, that promote regional economic cooperation. APEC members acknowledge that all areas of the agri-food value chain are interdependent and that there is a need for a whole-system approach.

In my capacity as the Chair of APEC’s Small and Medium Enterprises Working Group, I’d like to stress the importance of the latter: inclusivity and small business. MSMEs account for over 97 percent of all business in APECeconomies and employ over half of the workforce. Any strategy for reducing food wastage will have to involve the wholesale participation of the region’s smaller businesses.

This is easier written than done. For one thing, fit-for-purpose data is scarce. No APECeconomy has food waste data that is specific to MSMEs. And while all have policies and measures to address the problem of food waste, there are no large-scale direct MSME–food waste reduction targets, policies or plans. Few have tried to reduce MSMEfood waste in the retail food and food service industries. Supermarkets, food storage facilities or warehouses in many APECeconomies aren’t required to donate excesses.

Most entrepreneurs aren’t even aware of the problem, or underestimate its true cost. Those who do understand have limited options or capital, and are unable to find cost-effective solutions to create value out of food waste, and face problems with logistics and transportation. On top of this, there are few to no regulatory frameworks to guide them. From a technology perspective, a majority of APECeconomies utilize modern technologies, including mobile applications, to reduce or manage MSMEfood waste/surplus food, but these modern technologies are used only by large companies in big cities.

Amid these challenges are an abundance of opportunities to help MSMEs reduce food waste. Training, policies and guidelines can aid them in improving profits by reducing costs and increasing the value added of food. They can reduce their carbon footprint, which enhances consumerdemand, and divert waste to new products or bioenergy.

A November study by the APEC Small and Medium Enterprises Working Group presents case studies, identifies the best available data on food waste for MSMEs, and identifies several best practices for economies in dealing with food waste through MSME policy.

In one section, the study’s authors analyze a case study of a successful MSME, and identify four key factors contributing to its successful reduction of food waste: 1) creating a network of people — e.g., a community surrounding a farm; 2) using innovation and technology to facilitate farming and save time; 3) producing knowledge and providing it through several channels — e.g., a learning and training center, friendly guide books; and 4) considering the environment at every step of the process.

“If you raise [the development of the BRI] to the strategic level, there are countries where … you will have to lose money and there are countries where you will be free to make money.”

How to respond to the growing political divide between China and the West marked by partial decoupling, security alliances, and the risk of sanctions, amongst other things, continues to be a major topic of discussion among China’s intellectual elite. As already evidenced in previous editions of this newsletter, opinions vary considerably. Those presented here so far have ranged from Da Wei (达巍) stressing the importance of preserving if not strengthening ties with the West and Shen Wei (沈伟) arguing in favor of reforming the WTO and building up a network of free trade agreements to Ye Hailin (叶海林) emphasizing the need for China to demonstrate its military might to demobilize U.S. allies and Lu Feng (路风) calling for self-reliance and greater assertiveness in the field of tech. A certain amount of overlap certainly exists among these perspectives but the differences are nonetheless striking.

Today’s edition of Sinification looks at a speech made last month by Yang Ping (杨平), head and editor-in-chief of the highly regarded Beijing Cultural Review (文化纵横, hereafter BCR). Yang is also director of the Longway Foundation (修远基金会) which publishes BCR. The foundation describes its publication as “the most influential magazine of intellectual thought and commentary in China” and sees itself as having a key role in helping shape the direction of intellectual debates in China (“议题的设置就是意识形态斗争成功的一半”). Indeed, BCR often republishes old articles at key junctures as so often highlighted by David Ownby’s wonderful Reading the China Dream.

The following are excerpts from an edited transcript of a speech by Yang made at an event hosted by Renmin University’s Chongyang Institute for Financial Studies, which was attended by China’s Vice-minister of foreign affairs Xie Feng (谢锋). In his speech, Yang advocates building a new international system led by countries in the Global South (which, of course, includes China) rather than the West. His ideas are not particularly novel but are nevertheless noteworthy in that they represent yet another viewpoint in the ongoing debate over how China should respond to the increasing tensions that characterize its relations with the U.S. and other Western countries. Next week, I will be sharing a somewhat longer piece that proposes a way of protecting China from the growing threat of Westernsanctions.

China must respond to this growing trend by building a “new type of international system” with other countries in the Global South.

BRI projects should be increasingly focused on achieving this goal and thus allow more room for loss-making endeavors.

Capitalist politics ≠ Capitalist economics

“Since 2022 and the Russo-Ukrainian conflict, our main focus and topic of discussion has been China’s construction of a new type of international system.

“We have witnessed two typical manifestations of the separation of politics and the economy and the impact of politics on the economy:

The first is the conflict between Russia and Ukraine. The sanctions imposed on Russia by the United States and the West have reached unthinkable, abominable [令人发指] and unimaginable proportions. Under established international rules, it was understood that such sanctions could not possibly occur, but now they have. These include the fracturing of the financial system, the expropriation and seizure of Russian private assets and the freezing of Russianforeign exchange reserves. These are all abominable and unimaginable forms of confrontation. At the same time, the Russo-Ukrainian conflict has led to serious disruptions in global food and energy systems and supply chains, with massive food ‘shortages’ and soaring food prices, particularly in developing countries. Sanctions and political repression [政治打压] have severely disrupted the [world’s] economic order.

The second is the conflict between the U.S. and China. Since the Trump era, the U.S. has been engaged in a trade war against China, mainly by raising tariffs. Basically, this was simply about balancing trade [with China] and used mainly economic means. But under Biden, it [has become] a war that mixes politics with economics. Biden’s strategy towards China can basically be summed up in just a few words: one, friend-shoring, [i.e.] only allowing friendly countries into [parts of] its supply chains; two, alliancepolitics, [i.e.] continuously forging an alliance system involving NATO, the European Union, Japan, AUKUS and the four Asia-Pacific countries [I assume he is referring to South Korea, Japan, New Zealand and Australia taking part for the first time in a NATO summit last year] and constantly opposing China [不断应对中国]; three, its so-called ‘precision strikes’, [i.e.] its radical crackdown on China’s high tech [industry], especially our chip industry.”

China is being pushed out of the U.S.-led international system

“The information I have seen so far is that the number of Chinese companies included in the U.S.’s ‘entity list’ has risen from 132 under Trump to over 530 now. The scope of such point-to-point [点对点] precision strikes is constantly expanding. With such a political impact on the economy, we can feel the [world’s] economic order being disrupted across the board. The world is moving inexorably in the direction of decoupling. The phenomenon of politics affecting the economy and the capitalistpolitical order no longer upholding the capitalisteconomic order are extremely striking.

“In such a context, the challenges now facing China are extremely serious and varied. We have the pressures of dealing both with containment in the Indo-Pacific and with the U.S.-led politics of alliances across the world. More importantly and fundamentally China faces the strategic task of building a new type of international system [新型国际体系] … The existing Western-dominated international system used to be one in which we tried hard to blend [so as] to become one with it. During this process, we [sought to] absorb the West’s advanced technologies and management [practices] and thus complete our mission of industrialisation and modernization.

“But once you enter the existing international system, he [who is already inside] does not want to play with you, and even wants to drive you back out. He wants to divide both supply chains and the economic system into two parts [搞成两套] and desperately wants to contain and suppress you. This is not something that can be determined by your own subjective preferences. He has made up his mind: you have already become his ‘fated opponent’ [命定的对手]. He has to suppress you and drive you out of the existing system.”

Building a new international system with the Global South

“It is at this point that China is faced with the task of constructing a new type of international system that is not dominated by the West. In today’s so-called strategic quadrangle consisting of the U.S., Europe, Russia and China, how to construct such an international system appears particularly difficult [逼庂 literally means ‘narrow’ or ‘cramped’ rather than ‘difficult’].

“But if we look a little further south, we will find a vast number of developing countries, the Third World and the countries of the global South. They should be our strategy’s depth [我们的战略纵深]. That is to say, [we should] build a new type of international relations and a new type of international system that has strategic depth and in which China and the countries of the global South are jointly integrated. [This] is, in my view, an important strategic task for China’s international relations in the coming decades.”

BRI projects: Strategy trumps profitability

“For China today, especially for businesses and governments at all levels [within China] that are currently working hard to develop BRI trade, there is a very important point to which they should be alerted or reminded about: the development of the BRI has to go beyond mere business, beyond the general export of [China’s excess] production capacity, beyond the partial thinking of industry and the partial thinking at the regional level, or the simple economic way of thinking of business. The development of the BRI should be considered at the strategic level. That is, it should be included into China’s strategy when thinking about Africa, South America, Southeast Asia and Central Asia.

“If you raise [the development of the BRI] to the strategic level, there are countries where you won’t be able to make money and will have to lose money, and there are countries where you will be free to make money. You have to unite the two within your organic strategy.

“The strategic task of building a new type of international system is, in my view, a strategic proposition that Chinesethink tanks and research institutes should pay very close attention to with regards to international relations.

“Time is limited today. I just wanted to make a start here. I hope to receive your corrections and criticisms. Thank you!”

The recessive importance of the Global South was previously explored by Richard and his partner Larry, with input from Supratik Bose, many decades ago as shown here.

It means that many more qubits, the basic calculating unit, can be joined together than is possible on a single microchip. This will make a more powerful quantum computer possible.

The scaling of qubit numbers from the current level of around 100 qubits to nearer 1 million is central to creating a quantum processor that can make useful calculations.

The significant achievement is based on a technical blueprint for creating a large-scale quantum computer, which was first published in 2017 with funding from EPSRC.

Their development may help solve pressing challenges from drug discovery to energy-efficient fertilizer production. But their impact is expected to sweep across the economy, transforming most sectors and all our lives.

Potential to scale up

Winfried Hensinger, Professor of Quantum Technologies at the University of Sussex and Chief Scientist and co-founder at Universal Quantum said:

The researchers were successful in transporting the qubits using electrical fields with a 99.999993% success rate and a connection rate of 2424 transfers per second. Both numbers are world records.

Dr. Kedar Pandya, Director of Cross-Council Programmes at EPSRC, said:

This significant milestone is evidence of how EPSRC funded science is seeding the commercial future for quantum computing in the UK.

The potential for complex technologies, like quantum, to transform our lives and create economic value widely relies on visionary early-stage investment in academic research.

We deliver that crucial building block and are delighted that the University of Sussex and its spin-out company, Universal Quantum, are demonstrating the strength it supports.

In this Economic Letter, we assess whether recent higher inflation is leading businesses and households in Mexico to expect inflation to remain high over the long run. Specifically, we focus on what rising market-based measures of inflation compensation may imply about bondinvestors’ outlook for inflation. The rise in inflation compensation since spring 2021 could reflect three factors: an increase in investors’ inflation expectations, an uptick in the premium investors demand for assuming inflation risk, or changes in other risk and liquidity premiums. We explore the relative importance of each of these factors using a novel dynamic term structure model of nominal and inflation-adjusted yields described in Beauregard et al. (2021, henceforth BCFZ). Overall, our results for five-year inflation expectations five years from now suggest Mexicanbondinvestors’ long-term inflation expectations have been little affected by the recent rise in inflation. Instead, the rise in inflation compensation reflects a notable uptick in the inflation risk premium to the high end of its historical range. This suggests that, despite inflation expectations being little changed on average, some investors are particularly concerned about the risk that inflation will remain above expected levels.

The recent rise in Mexican inflation

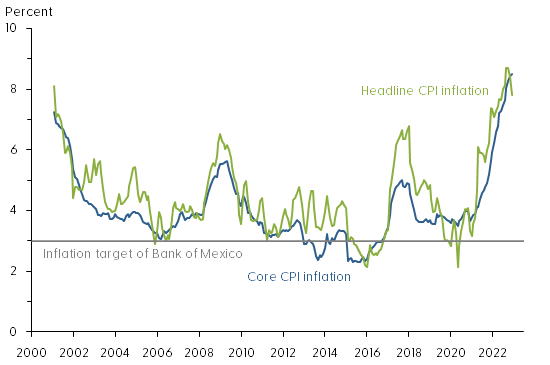

Figure 1 shows the year-over-year change in the Mexicanconsumer price index (CPI) measured both by the headline CPI (green line) and the more stable core CPI (blue line) that strips out volatile food and energy prices. Also shown with a horizontal gray line is the 3% inflation target of the nation’s central bank, the Bank of Mexico.

Figure 1: Mexican consumer price index inflation

Source: Instituto Nacional de Estadística y Geografía.

We note that MexicanCPIinflation has averaged somewhat above the Bank of Mexico’s target since its adoption in 2002. More importantly, CPIinflation in Mexico appears to have become more volatile and somewhat higher over the past five years. Although previous research by De Pooter et al. (2014) found inflation expectations in Mexico to be well anchored, the significant global economic dislocations caused by the coronavirus pandemic and related inflationary pressures could impact inflation expectations of businesses and households.

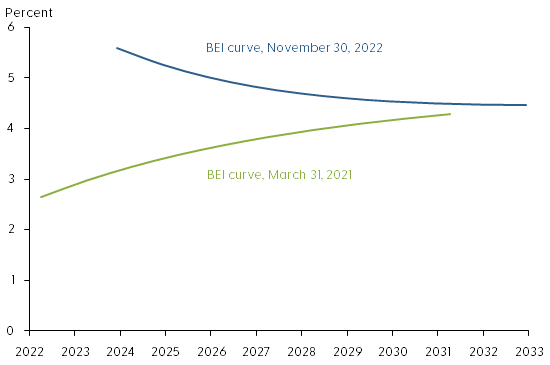

The difference between nominal and real yields for bonds of the same maturity is known as breakeven inflation (BEI). This represents a market-based measure of inflation compensation used to assess financial market participants’ inflation expectations. Figure 2 shows BEI rates at different maturities, meaning annual average rates of inflation compensation between now and maturity, from 1 to 10 years at the end of March 2021 (green line) and at the end of November 2022 (blue line). The slightly upward-sloping BEI curve of close to 3% in 2021 contrasts with the higher downward-sloping BEI curve in 2022.

Figure 2: BEI curves for 1-year to 10-year Mexican bond maturities

Source: Authors’ calculations using bond prices from Bloomberg.

The increase for shorter maturities, the left end of the 2022 BEI curve, is closely tied to the current high level of inflation and suggests inflation may remain elevated for some time. In contrast, the increase at longer maturities, the right end of the 2022 BEI curve, suggests that investors’ longer-term inflation expectations may be drifting above the Bank of Mexico’s inflation target. To better understand the shape and sources of variation of the BEI curve we use a yield curve model.

A yield curve model of nominal and real yields

Market-based measures of inflation compensation such as BEI rates contain three components. First, they include the average CPIinflation rate expected by bondinvestors, which is the focus here. Second is an inflation risk premium to compensate investors for the uncertainty of future inflation. This premium is embedded in nominal yields that provide no inflation protection. Third is the difference in relative market liquidity between standard fixed-coupon and inflation-indexed bonds. As discussed in BCFZ, both of these types of Mexicanbonds are less liquid than U.S. Treasuries, and their prices therefore contain a discount to compensate investors for their liquidity risk. Neither the inflation risk premium nor the liquidity premiums are directly observable and must therefore be estimated.

To adjust for these challenges, we first use the nominal and real yields model developed in BCFZ to identify liquidity premiums in standard fixed-coupon and inflation-indexed bond prices as a function of the time since issuance and the remaining time to maturity. The time since issuance serves as a proxy for declining liquidity as, over time, a larger fraction of bonds gets locked into buy-and-hold strategies. We refer to the observed BEI net of estimated liquidity premiums as the adjusted BEI. In a second step, we then separate adjusted BEI into components representing investors’ inflation expectations using a formula based on the absence of bond market arbitrage opportunities and the residual inflation risk premium.

Results

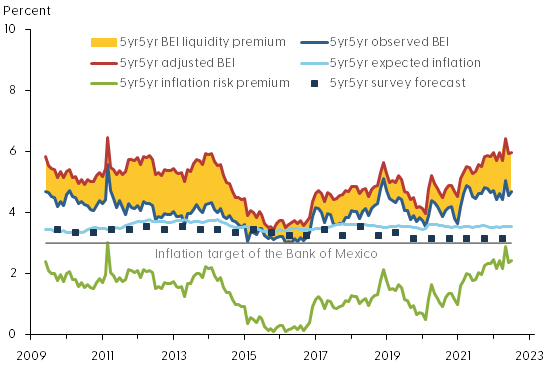

To assess whether investors’ inflation outlook has fundamentally changed, we follow De Pooter et al. (2014) and examine the five-year forward BEI rate that starts five years ahead, denoted 5yr5yr BEI. This is a horizon sufficiently long into the future that most transitory shocks to the economy can be expected to have vanished. Hence, the embedded inflation expectations are presumably less affected by current high inflation and pandemic-related transitory conditions and can therefore speak to the question about the anchoring of inflation expectations in Mexico.

Figure 3 shows the breakdown of 5yr5yr BEI into its various components according to our model. The dark blue line is the observed BEI, and the red line is the estimated adjusted BEI without liquidity risk premiums or other residual disturbances. The difference between these two measures of BEI—the yellow shaded area—represents the model’s estimate of the net liquidity premium or distortion of the observed BEI series due to risk premiums in both nominal and inflation-indexed bond prices. The adjusted BEI is entirely above the observed BEI, suggesting the liquidity risk distortions are systematically larger in the inflation-indexed bond prices, consistent with similar evidence from the U.S. Treasury market (Andreasen and Christensen 2016). Note that the net BEI liquidity premium widened around the financial turmoil in spring 2020 at the start of the pandemic and remains elevated.

Figure 3: Components of 5yr5yr breakeven inflation for Mexico

Source: Survey forecasts from Consensus Economics and authors’ calculations using bond prices from Bloomberg.

The model also allows us to break down the adjusted BEI into an expected inflation component (light blue line) and the residual inflation risk premium (green line). Also shown is the Bank of Mexico’s 3% inflation target (gray horizontal line). For comparison, the figure also shows the 5yr5yr expected CPIinflation in Mexico reported semiannually in the Consensus Forecasts surveys (dark blue squares). We note that both observed and adjusted BEI have trended higher since the start of the pandemic in early 2020. Importantly, the breakdown indicates that long-term expected inflation in Mexico has remained stable, slightly above the 3% inflation target. As a result, the increase in BEI can be attributed to the inflation risk premium, which is at the high end of its historical range towards the end of our sample. Given the elevated levels of current inflation, this suggests some investors are concerned that inflation could remain elevated for longer than currently anticipated.

This raises the question of whether long-term inflation expectations in Mexico are likely to remain anchored near their current level going forward. To assess this risk, we simulate 10,000-factor paths over a three-year horizon using the estimated factors and factor dynamics as of November 2022—that is, the simulations are conditioned on the shapes of the nominal and real yield curves and investors’ embedded forward-looking expectations as of November 2022. These simulated factor paths are then converted into forecasts of 5yr5yr expected inflation. Figure 4 shows the median projection (solid green line) and the 5th and 95th percentile values (dashed green lines) for the simulated 5yr5yr expected inflation over a three-year horizon.

Figure 4: Three-year projections of 5yr5yr expected inflation, Mexico

Source: Authors’ calculations.

Our model projections indicate that long-term inflation expectations are likely to deviate only modestly from their current level, consistent with the variation of the historical estimates back to 2009. Overall, our findings represent tangible evidence that long-term inflation expectations remain well-anchored in Mexico despite the recent rise in inflation.

Conclusion

Global inflation pressures in the aftermath of the pandemic have raised fears about a sustained increase in the level of inflation around the world, which could be particularly challenging for developing economies with monetary policy guided by an inflation target. In this Letter, to assess this risk for a major emerging economy with an established inflation target, we examine the variation in Mexico’s nominal and inflation-indexed bond prices, while accounting for their respective liquidity risk premiums. This allows us to estimate Mexicanbond investors’ inflation expectations and associated risk premiums. The results reveal that the inflation risk premium has pushed up Mexican BEI rates in recent years, while investors’ long-term inflation expectations have remained stable near the Bank of Mexico’s inflation target despite the rise in inflation.

The policy path needed to keep inflation expectations anchored in a situation with highly elevated inflation may involve tradeoffs. The Bank of Mexico responded early and forcefully to inflation pressures starting in June 2021 and has indicated further tightening of the policy rate would likely be appropriate to bring inflation back down to target over the medium term. This could lower economic growth in Mexico in both 2022 and 2023. On the other hand, history shows that it may be difficult and costly to reverse extended departures from announced inflation targets. Thus, it will be important for central banks with inflation-targeting frameworks to monitor measures of long-term inflation expectations in the current situation.

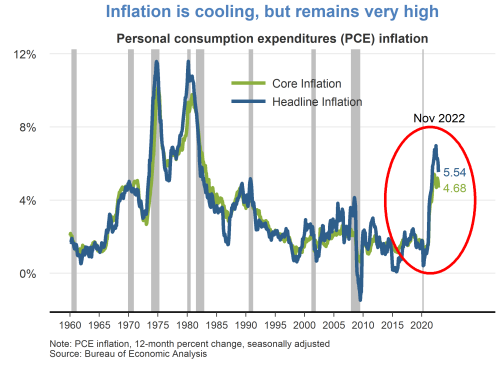

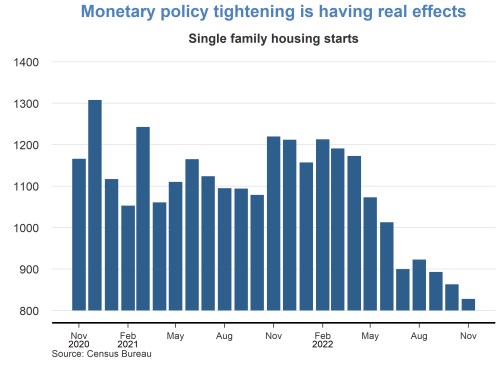

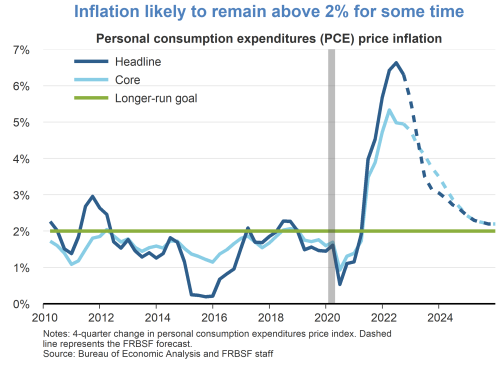

While continuing to cool over the last several months, 12-month inflation remains at historically high levels. The headline personal consumption expenditures (PCE) price index rose 5.5% in November 2022 from a year earlier. This marks a decline in inflation to a level last observed in October 2021, but still well above the Fed’s longer-run goal of 2%. A portion of the inflation moderation is attributable to recent declines in energy prices. Core PCE inflation, which removes food and energy prices, has shown less easing.

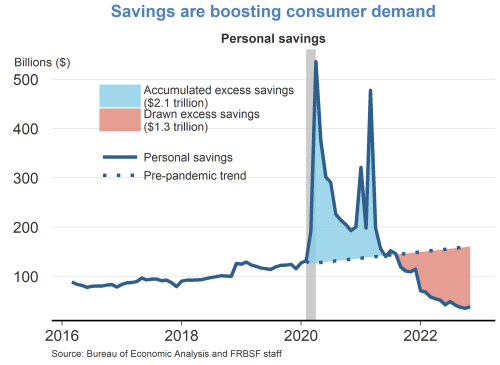

Owing to fiscal relief efforts and lower household spending over the course of the pandemic, consumers accumulated over $2 trillion dollars in excess savings, based on pre-pandemic trends. Since then, consumers have drawn down over half of this excess savings which has helped support recent growth in personal consumption expenditures. A considerable amount of accumulated savings remains for some consumers to support spending in 2023.

In the wake of the pandemic, consumer spending patterns shifted away from services towards goods. While there appears to be some normalization of spending behavior, this shift has generally persisted. Real goods spending remains significantly above its pre-pandemic trend, driven by strong demand for durables such as furniture, electronics, and recreational goods. Spending on services has shown a resurgence but remains below its pre-pandemic trend.

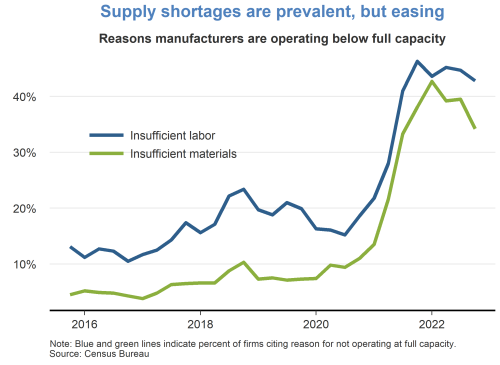

Supply chainbottlenecks for materials and labor remain a constraint on production, although there are some recent signs of easing. The fraction of manufacturers who reported operating below capacity due to insufficient materials peaked in late 2021 and has moderately declined over the past year. However, the fraction of manufacturers reporting insufficient labor has persisted at high levels.

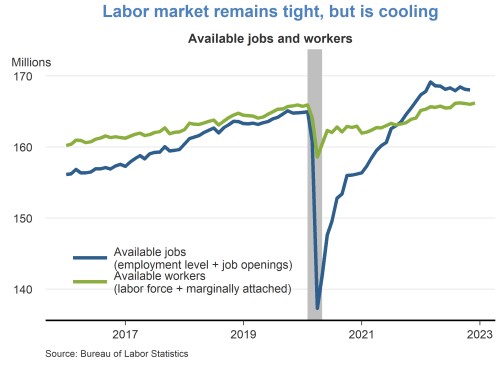

The labor market remains tight, despite some signs of cooling. The number of available jobs remains well above the number of available workers, although vacancy postings have been trending down in recent months. The tight labor market has put continued upward pressure on wages and labor market turnover.

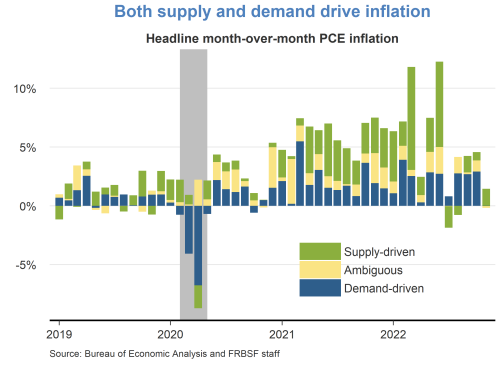

A decomposition of headline PCE inflation into supply– and demand-driven components shows that both supply and demand factors are responsible for the recent rise in inflation. The surge in inflation in early 2021 was mainly due to an increase in demand-driven factors. Subsequently, supply factors became more prevalent for the remainder of 2021. Supply-driven inflation has moderated significantly over recent months, while demand-driven inflation remains elevated.

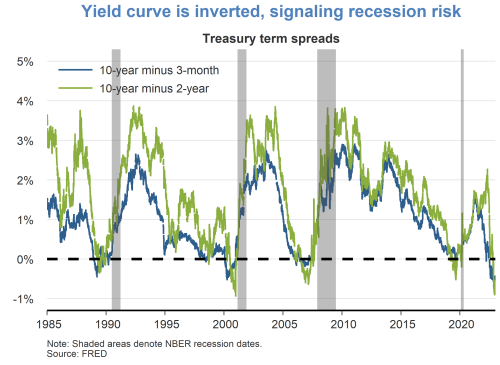

Although the labor market is currently very strong, financial markets are pointing to some downside risks. Namely, the difference between longer- and shorter-term interest rates has turned negative, which historically tends to occur immediately preceding recessions. It remains unclear whether lower longer-term yields are indicative of anticipated slower growth or lower inflation.

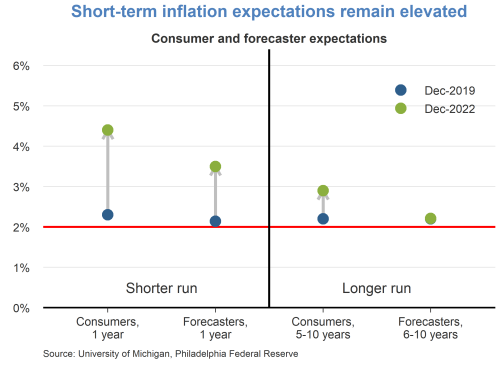

Short-term inflation expectations remain elevated relative to their pre-pandemic levels in December 2019. Consumers are expecting prices to rise 5% this year, while professional forecasters are expecting prices to rise 3.5%. Longer-term inflation expectations remain more subdued, indicating that both consumers and professionals believe inflation pressures will eventually dissipate.

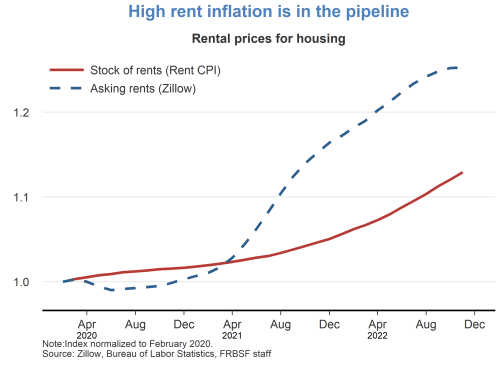

Rentinflation is expected to remain high over the next year. The prices for asking rents have grown quite substantially over the last two years. As new leases begin and existing leases are renewed, these higher asking rents will flow into the stock of rental units, putting upward pressure on rentinflation.

The growth rate of real gross domestic product (GDP) is a key indicator of economic activity, but the official estimate is released with a delay. Our GDPNow forecasting model provides a “nowcast” of the official estimate prior to its release by estimating GDP growth using a methodology similar to the one used by the U.S.Bureau of Economic Analysis.

GDPNow is not an official forecast of the Atlanta Fed. Rather, it is best viewed as a running estimate of real GDP growth based on available economic data for the current measured quarter. There are no subjective adjustments made to GDPNow—the estimate is based solely on the mathematical results of the model. In particular, it does not capture the impact of COVID-19 and social mobility beyond their impact on GDP source data and relevant economic reports that have already been released. It does not anticipate their impact on forthcoming economic reports beyond the standard internal dynamics of the model.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2022 is 3.9 percent on January 3, up from 3.7 percent on December 23. After last week’s Advance Economic Indicators report from the U.S. Census Bureau and this morning’s construction spending release from the U.S. Census Bureau, the nowcasts of fourth-quarter real gross private domestic investment growth and fourth-quarter real government spending growth increased from 3.8 percent and 0.8 percent, respectively, to 6.1 percent and 1.0 percent, respectively, while the nowcast of the contribution of the change in real net exports to fourth-quarter real GDP growth decreased from 0.35 percentage points to 0.17 percentage points.

“In 1985, one of the greatest treasure discoveries was made off the Florida Keys, when the wreck of the Spanish ship Atocha was found. On board were some forty tons of silver and gold, which in 1622 had been heading from the New World to the Spanish treasury as the means to fund the Thirty Years’ War.”

All of these cases constitute a kind of harmless kind of “pop globalization” based on exotic voyages and travels.

Consider another such example, perhaps more academic:

“About the middle of the sixteenth centuryAntwerp reached its apogee. For the first time in history there existed both a European and a world market; the economies of different parts of Europe had become interdependent and were linked through the Antwerp market, not only with each other but also with the economies of large parts of the rest of the world. Perhaps no other city has ever again played such a dominant role as did Antwerp in the second quarter of the sixteenth century.”

This sounds like some kind of identifiably global period.

Actually, modern historians define globalization as “price convergence” (i.e., wheat has now a unified “world price,” implying a world market). This rigorous definition is confirmed by and also shows up in the data in the 1820s and may or may not be prefigured by all the Marco Polo and Atochasilver stories, mentioned above.

Kevin O’Rourke and Jeffrey Williamson present a coherent picture of In Globalization and History, Kevin O’Rourke and Jeffrey Williamson present a coherent picture of trade, migration, and international capital flows in the Atlantic economy in the century prior to 1914—the first great globalization boom, which anticipated the experience of the last fifty years. The authors estimate the extent of globalization and its impact on the participating countries, and discuss the political reactions that it provoked. The book’s originality lies in its application of the tools of open-economyeconomics to this critical historical period—differentiating it from most previous work, which has been based on closed-economy or single-sector models. The authors also keep a close eye on globalization debates of the 1990s, using history to inform the present and vice versa. The book brings together research conducted by the authors over the past decade—work that has profoundly influenced how economic history is now written and that has found audiences in economics and history, as well as in the popular press.

(book summary)

In everyday language, we associate the word globalization with some ever-increasing Marco Polo phenomena. While that’s not entirely wrong, globalization in the more technical sense begins to show up in the data only from the 1820s. At this point, we begin to see the convergence of worldwide wheat prices, for example. This makes the world, for the first time, a global “store” with unified prices. Here is the technical beginning of globalization. The years 1870-1914 are subsequently the first real era of modern globalization and represent a kind of “take-off” from the first stirrings of the 1820s. World Wars I & II might be seen as globalization backlash.