It means that many more qubits, the basic calculating unit, can be joined together than is possible on a single microchip. This will make a more powerful quantum computer possible.

The scaling of qubit numbers from the current level of around 100 qubits to nearer 1 million is central to creating a quantum processor that can make useful calculations.

The significant achievement is based on a technical blueprint for creating a large-scale quantum computer, which was first published in 2017 with funding from EPSRC.

Their development may help solve pressing challenges from drug discovery to energy-efficient fertilizer production. But their impact is expected to sweep across the economy, transforming most sectors and all our lives.

Potential to scale up

Winfried Hensinger, Professor of Quantum Technologies at the University of Sussex and Chief Scientist and co-founder at Universal Quantum said:

The researchers were successful in transporting the qubits using electrical fields with a 99.999993% success rate and a connection rate of 2424 transfers per second. Both numbers are world records.

Dr. Kedar Pandya, Director of Cross-Council Programmes at EPSRC, said:

This significant milestone is evidence of how EPSRC funded science is seeding the commercial future for quantum computing in the UK.

The potential for complex technologies, like quantum, to transform our lives and create economic value widely relies on visionary early-stage investment in academic research.

We deliver that crucial building block and are delighted that the University of Sussex and its spin-out company, Universal Quantum, are demonstrating the strength it supports.

The Atlanta Fed’s Wage Growth Tracker was 6.1 percent in January, the same as in December. For people who changed jobs, the Tracker in January was 7.3 percent, compared to 7.7 percent in December. For those not changing jobs, the Tracker was 5.4 percent, compared to the 5.3 percent reading in December.

In this Economic Letter, we assess whether recent higher inflation is leading businesses and households in Mexico to expect inflation to remain high over the long run. Specifically, we focus on what rising market-based measures of inflation compensation may imply about bondinvestors’ outlook for inflation. The rise in inflation compensation since spring 2021 could reflect three factors: an increase in investors’ inflation expectations, an uptick in the premium investors demand for assuming inflation risk, or changes in other risk and liquidity premiums. We explore the relative importance of each of these factors using a novel dynamic term structure model of nominal and inflation-adjusted yields described in Beauregard et al. (2021, henceforth BCFZ). Overall, our results for five-year inflation expectations five years from now suggest Mexicanbondinvestors’ long-term inflation expectations have been little affected by the recent rise in inflation. Instead, the rise in inflation compensation reflects a notable uptick in the inflation risk premium to the high end of its historical range. This suggests that, despite inflation expectations being little changed on average, some investors are particularly concerned about the risk that inflation will remain above expected levels.

The recent rise in Mexican inflation

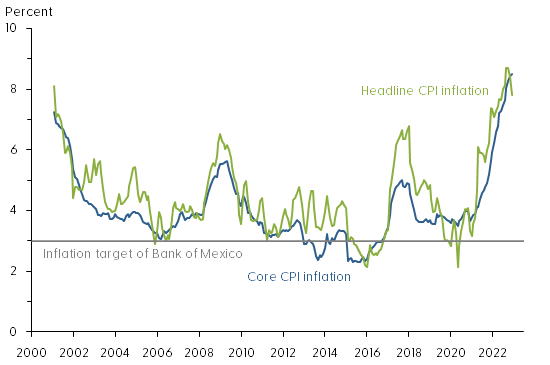

Figure 1 shows the year-over-year change in the Mexicanconsumer price index (CPI) measured both by the headline CPI (green line) and the more stable core CPI (blue line) that strips out volatile food and energy prices. Also shown with a horizontal gray line is the 3% inflation target of the nation’s central bank, the Bank of Mexico.

Figure 1: Mexican consumer price index inflation

Source: Instituto Nacional de Estadística y Geografía.

We note that MexicanCPIinflation has averaged somewhat above the Bank of Mexico’s target since its adoption in 2002. More importantly, CPIinflation in Mexico appears to have become more volatile and somewhat higher over the past five years. Although previous research by De Pooter et al. (2014) found inflation expectations in Mexico to be well anchored, the significant global economic dislocations caused by the coronavirus pandemic and related inflationary pressures could impact inflation expectations of businesses and households.

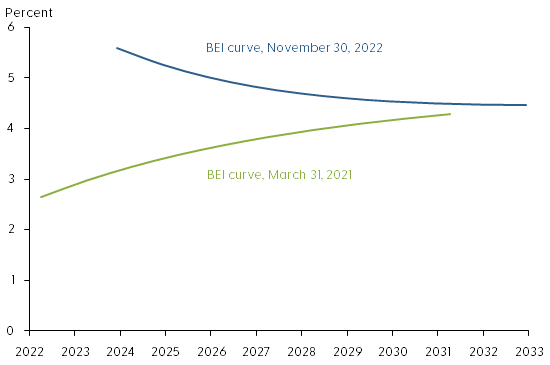

The difference between nominal and real yields for bonds of the same maturity is known as breakeven inflation (BEI). This represents a market-based measure of inflation compensation used to assess financial market participants’ inflation expectations. Figure 2 shows BEI rates at different maturities, meaning annual average rates of inflation compensation between now and maturity, from 1 to 10 years at the end of March 2021 (green line) and at the end of November 2022 (blue line). The slightly upward-sloping BEI curve of close to 3% in 2021 contrasts with the higher downward-sloping BEI curve in 2022.

Figure 2: BEI curves for 1-year to 10-year Mexican bond maturities

Source: Authors’ calculations using bond prices from Bloomberg.

The increase for shorter maturities, the left end of the 2022 BEI curve, is closely tied to the current high level of inflation and suggests inflation may remain elevated for some time. In contrast, the increase at longer maturities, the right end of the 2022 BEI curve, suggests that investors’ longer-term inflation expectations may be drifting above the Bank of Mexico’s inflation target. To better understand the shape and sources of variation of the BEI curve we use a yield curve model.

A yield curve model of nominal and real yields

Market-based measures of inflation compensation such as BEI rates contain three components. First, they include the average CPIinflation rate expected by bondinvestors, which is the focus here. Second is an inflation risk premium to compensate investors for the uncertainty of future inflation. This premium is embedded in nominal yields that provide no inflation protection. Third is the difference in relative market liquidity between standard fixed-coupon and inflation-indexed bonds. As discussed in BCFZ, both of these types of Mexicanbonds are less liquid than U.S. Treasuries, and their prices therefore contain a discount to compensate investors for their liquidity risk. Neither the inflation risk premium nor the liquidity premiums are directly observable and must therefore be estimated.

To adjust for these challenges, we first use the nominal and real yields model developed in BCFZ to identify liquidity premiums in standard fixed-coupon and inflation-indexed bond prices as a function of the time since issuance and the remaining time to maturity. The time since issuance serves as a proxy for declining liquidity as, over time, a larger fraction of bonds gets locked into buy-and-hold strategies. We refer to the observed BEI net of estimated liquidity premiums as the adjusted BEI. In a second step, we then separate adjusted BEI into components representing investors’ inflation expectations using a formula based on the absence of bond market arbitrage opportunities and the residual inflation risk premium.

Results

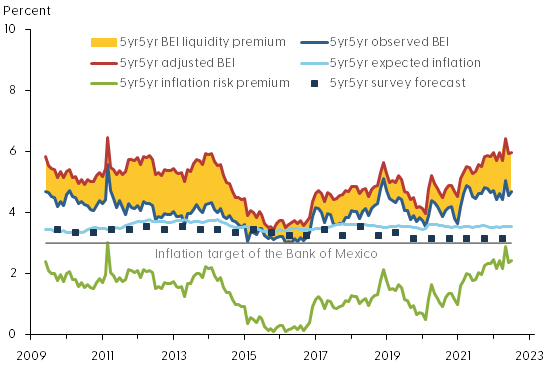

To assess whether investors’ inflation outlook has fundamentally changed, we follow De Pooter et al. (2014) and examine the five-year forward BEI rate that starts five years ahead, denoted 5yr5yr BEI. This is a horizon sufficiently long into the future that most transitory shocks to the economy can be expected to have vanished. Hence, the embedded inflation expectations are presumably less affected by current high inflation and pandemic-related transitory conditions and can therefore speak to the question about the anchoring of inflation expectations in Mexico.

Figure 3 shows the breakdown of 5yr5yr BEI into its various components according to our model. The dark blue line is the observed BEI, and the red line is the estimated adjusted BEI without liquidity risk premiums or other residual disturbances. The difference between these two measures of BEI—the yellow shaded area—represents the model’s estimate of the net liquidity premium or distortion of the observed BEI series due to risk premiums in both nominal and inflation-indexed bond prices. The adjusted BEI is entirely above the observed BEI, suggesting the liquidity risk distortions are systematically larger in the inflation-indexed bond prices, consistent with similar evidence from the U.S. Treasury market (Andreasen and Christensen 2016). Note that the net BEI liquidity premium widened around the financial turmoil in spring 2020 at the start of the pandemic and remains elevated.

Figure 3: Components of 5yr5yr breakeven inflation for Mexico

Source: Survey forecasts from Consensus Economics and authors’ calculations using bond prices from Bloomberg.

The model also allows us to break down the adjusted BEI into an expected inflation component (light blue line) and the residual inflation risk premium (green line). Also shown is the Bank of Mexico’s 3% inflation target (gray horizontal line). For comparison, the figure also shows the 5yr5yr expected CPIinflation in Mexico reported semiannually in the Consensus Forecasts surveys (dark blue squares). We note that both observed and adjusted BEI have trended higher since the start of the pandemic in early 2020. Importantly, the breakdown indicates that long-term expected inflation in Mexico has remained stable, slightly above the 3% inflation target. As a result, the increase in BEI can be attributed to the inflation risk premium, which is at the high end of its historical range towards the end of our sample. Given the elevated levels of current inflation, this suggests some investors are concerned that inflation could remain elevated for longer than currently anticipated.

This raises the question of whether long-term inflation expectations in Mexico are likely to remain anchored near their current level going forward. To assess this risk, we simulate 10,000-factor paths over a three-year horizon using the estimated factors and factor dynamics as of November 2022—that is, the simulations are conditioned on the shapes of the nominal and real yield curves and investors’ embedded forward-looking expectations as of November 2022. These simulated factor paths are then converted into forecasts of 5yr5yr expected inflation. Figure 4 shows the median projection (solid green line) and the 5th and 95th percentile values (dashed green lines) for the simulated 5yr5yr expected inflation over a three-year horizon.

Figure 4: Three-year projections of 5yr5yr expected inflation, Mexico

Source: Authors’ calculations.

Our model projections indicate that long-term inflation expectations are likely to deviate only modestly from their current level, consistent with the variation of the historical estimates back to 2009. Overall, our findings represent tangible evidence that long-term inflation expectations remain well-anchored in Mexico despite the recent rise in inflation.

Conclusion

Global inflation pressures in the aftermath of the pandemic have raised fears about a sustained increase in the level of inflation around the world, which could be particularly challenging for developing economies with monetary policy guided by an inflation target. In this Letter, to assess this risk for a major emerging economy with an established inflation target, we examine the variation in Mexico’s nominal and inflation-indexed bond prices, while accounting for their respective liquidity risk premiums. This allows us to estimate Mexicanbond investors’ inflation expectations and associated risk premiums. The results reveal that the inflation risk premium has pushed up Mexican BEI rates in recent years, while investors’ long-term inflation expectations have remained stable near the Bank of Mexico’s inflation target despite the rise in inflation.

The policy path needed to keep inflation expectations anchored in a situation with highly elevated inflation may involve tradeoffs. The Bank of Mexico responded early and forcefully to inflation pressures starting in June 2021 and has indicated further tightening of the policy rate would likely be appropriate to bring inflation back down to target over the medium term. This could lower economic growth in Mexico in both 2022 and 2023. On the other hand, history shows that it may be difficult and costly to reverse extended departures from announced inflation targets. Thus, it will be important for central banks with inflation-targeting frameworks to monitor measures of long-term inflation expectations in the current situation.

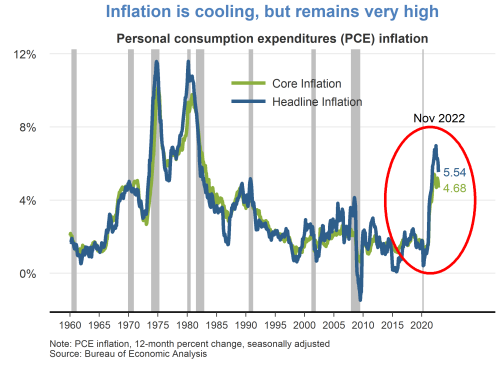

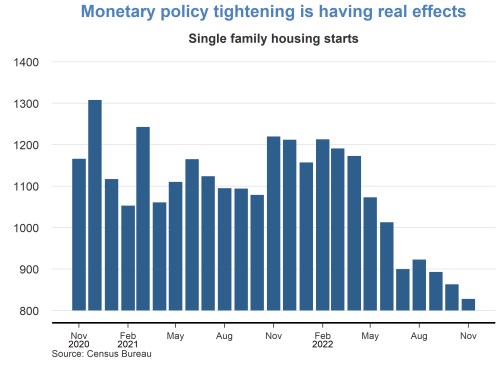

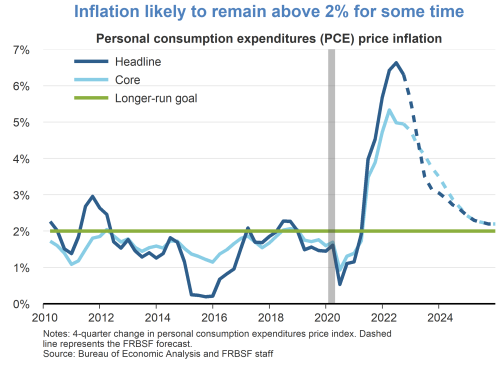

While continuing to cool over the last several months, 12-month inflation remains at historically high levels. The headline personal consumption expenditures (PCE) price index rose 5.5% in November 2022 from a year earlier. This marks a decline in inflation to a level last observed in October 2021, but still well above the Fed’s longer-run goal of 2%. A portion of the inflation moderation is attributable to recent declines in energy prices. Core PCE inflation, which removes food and energy prices, has shown less easing.

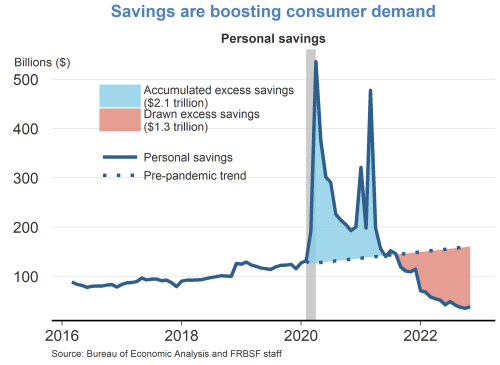

Owing to fiscal relief efforts and lower household spending over the course of the pandemic, consumers accumulated over $2 trillion dollars in excess savings, based on pre-pandemic trends. Since then, consumers have drawn down over half of this excess savings which has helped support recent growth in personal consumption expenditures. A considerable amount of accumulated savings remains for some consumers to support spending in 2023.

In the wake of the pandemic, consumer spending patterns shifted away from services towards goods. While there appears to be some normalization of spending behavior, this shift has generally persisted. Real goods spending remains significantly above its pre-pandemic trend, driven by strong demand for durables such as furniture, electronics, and recreational goods. Spending on services has shown a resurgence but remains below its pre-pandemic trend.

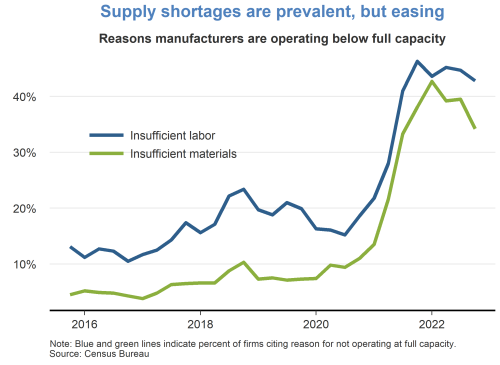

Supply chainbottlenecks for materials and labor remain a constraint on production, although there are some recent signs of easing. The fraction of manufacturers who reported operating below capacity due to insufficient materials peaked in late 2021 and has moderately declined over the past year. However, the fraction of manufacturers reporting insufficient labor has persisted at high levels.

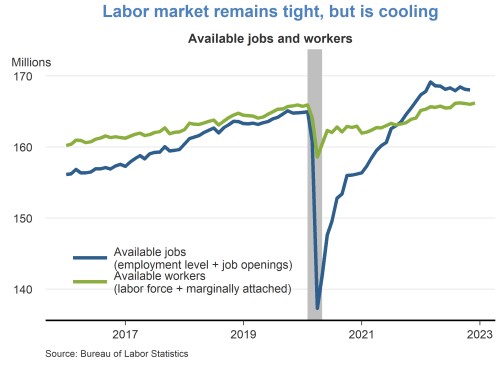

The labor market remains tight, despite some signs of cooling. The number of available jobs remains well above the number of available workers, although vacancy postings have been trending down in recent months. The tight labor market has put continued upward pressure on wages and labor market turnover.

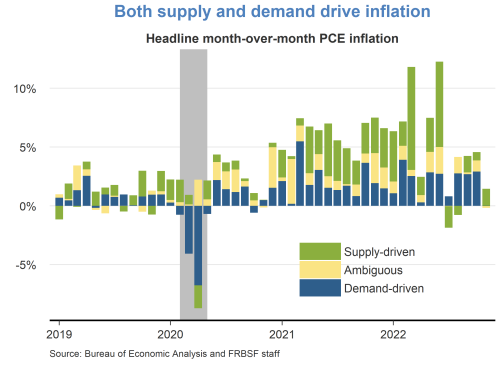

A decomposition of headline PCE inflation into supply– and demand-driven components shows that both supply and demand factors are responsible for the recent rise in inflation. The surge in inflation in early 2021 was mainly due to an increase in demand-driven factors. Subsequently, supply factors became more prevalent for the remainder of 2021. Supply-driven inflation has moderated significantly over recent months, while demand-driven inflation remains elevated.

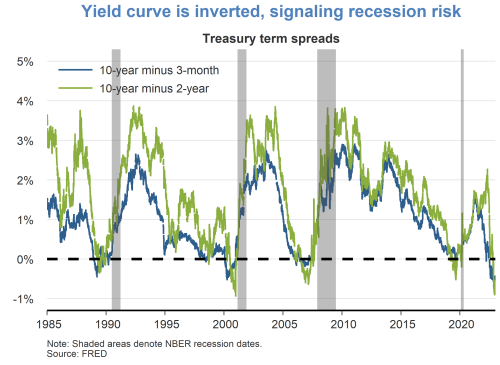

Although the labor market is currently very strong, financial markets are pointing to some downside risks. Namely, the difference between longer- and shorter-term interest rates has turned negative, which historically tends to occur immediately preceding recessions. It remains unclear whether lower longer-term yields are indicative of anticipated slower growth or lower inflation.

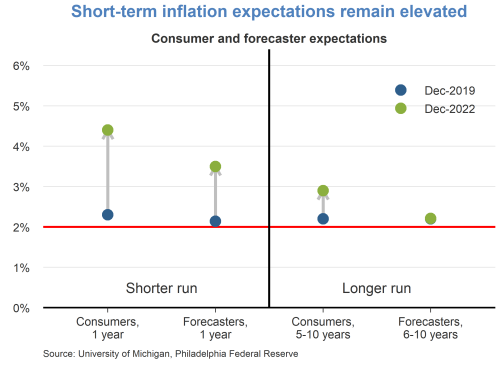

Short-term inflation expectations remain elevated relative to their pre-pandemic levels in December 2019. Consumers are expecting prices to rise 5% this year, while professional forecasters are expecting prices to rise 3.5%. Longer-term inflation expectations remain more subdued, indicating that both consumers and professionals believe inflation pressures will eventually dissipate.

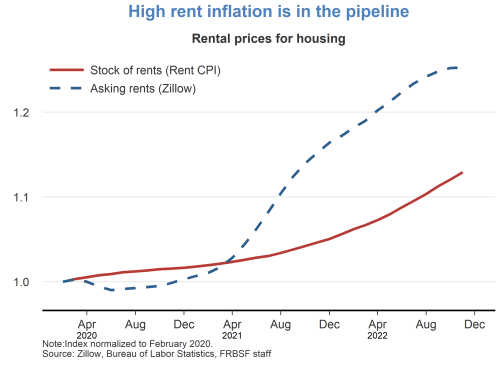

Rentinflation is expected to remain high over the next year. The prices for asking rents have grown quite substantially over the last two years. As new leases begin and existing leases are renewed, these higher asking rents will flow into the stock of rental units, putting upward pressure on rentinflation.

The growth rate of real gross domestic product (GDP) is a key indicator of economic activity, but the official estimate is released with a delay. Our GDPNow forecasting model provides a “nowcast” of the official estimate prior to its release by estimating GDP growth using a methodology similar to the one used by the U.S.Bureau of Economic Analysis.

GDPNow is not an official forecast of the Atlanta Fed. Rather, it is best viewed as a running estimate of real GDP growth based on available economic data for the current measured quarter. There are no subjective adjustments made to GDPNow—the estimate is based solely on the mathematical results of the model. In particular, it does not capture the impact of COVID-19 and social mobility beyond their impact on GDP source data and relevant economic reports that have already been released. It does not anticipate their impact on forthcoming economic reports beyond the standard internal dynamics of the model.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2022 is 3.9 percent on January 3, up from 3.7 percent on December 23. After last week’s Advance Economic Indicators report from the U.S. Census Bureau and this morning’s construction spending release from the U.S. Census Bureau, the nowcasts of fourth-quarter real gross private domestic investment growth and fourth-quarter real government spending growth increased from 3.8 percent and 0.8 percent, respectively, to 6.1 percent and 1.0 percent, respectively, while the nowcast of the contribution of the change in real net exports to fourth-quarter real GDP growth decreased from 0.35 percentage points to 0.17 percentage points.

In Karatani’s sharpest departure from conventional wisdom, he locates the origins of philosophy not in Athens, but in the earlier Ionian culture that greatly influenced the so-called “pre-Socratic thinkers” such as Heraclitus and Parmenides. Their ideas centered on the flux of constant change, in which “matter moves itself” without the gods, and the oneness of all being—a philosophical outlook closer to Daoist and Buddhist thought than to Plato’s later metaphysics, which posited that, as Karatani puts it, “the soul rules matter.”

In the political realm, Karatani contrasts the form of self-rule from Ionian times based on free and equal reciprocity among all inhabitants — “isonomia” — with what he calls the “degraded democracy” of Athens that rested on slavery and conquest. He considers the former the better foundation for a just polity.

In a novel twist on classical categorizations, Karatani regards Socrates himself as fitting into the pre-Socratic mold. “If one wants to properly consider the pre-Socratics, one must include Socrates in their number,” he writes. “Socrates was the last person to try to re-institute Ionian thought in politics.”

A Degraded Form of Democracy in Athens

For Karatani, Athenian democracy was debased because it was “constrained by the distinctions between public and private, and spiritual and manual labor,” a duality of existence that Socrates and the pre-Socratics sought to dismantle. As a result, by Karatani’s reading, Socrates was both held in contempt by the “aristocratic faction,” which sought to preserve its privileges built on the labor of others, and condemned to death by a narrow-minded mobocracy for his idiosyncratic insistence on autonomy and liberty in pursuit of truth.

Appalled at Socrates’ fate, Plato blamed democracy for giving birth to demagoguery and tyranny, radically rejecting the idea of rule by the masses and proposing instead a political order governed by philosophers. In Karatani’s reckoning, Plato then “took as his life’s work driving out the Ionian spirit that touched off Athenian democracy”—in short, throwing out the baby with the bathwater but maintaining the disassociations, such as citizen and slave, that follow from the distinction between public and private grounded in an apprehension of reality that separates the spiritual from the material.

In his seminal work, The Structure of World History, Karatani flips Marx’s core tenet that the economic “mode of production” is the substructure of society that determines all else. He postulates instead that it is the ever-shifting “modes of exchange” among capital, the state and nation which together shape the social order.

For Karatani, historically cultivated norms and beliefs about fairness and justice, including universal religions, compel the state to regulate inequality within the mythic commonality of the nation, which sees itself as whole people, tempering the logic of the unfettered market. As he sees it, the siren call of reciprocity and equality has remained deeply resonant throughout the ages, drawing history toward a return to the original ideal of isonomia.

Expanding the Space of Civil Society

Not an armchair philosopher, Karatani has actively promoted a modern form of the kind of reciprocity he saw in ancient Ionian culture, which he calls “associationism.” In practical terms in Japan, this entails the activation of civil society, such as through citizens’ assemblies, that would exercise self-rule from the bottom up.

In the wake of the Fukushima nuclear accident in 2011, Karatani famously called for “a society where people demonstrate” that would expand the space of civil society and constrict the collusive power of Japan’s political, bureaucratic and corporate establishment. Like other activists, he blamed this closed system of governance that shuts out the voices of ordinary citizens for fatally mismanaging the nuclear power industry in a country where earthquakes and tsunamis are an ever-present danger.

Over the past two weeks, Asia has played host to the most intense sequence of multilateralsummits since the pandemic began, as national leaders gathered for meetings organized by ASEAN, the G20 and APEC. Although overshadowed by geopolitical tensions, the meetings marked a welcome return to in-person summitdiplomacy, and the better-than-expected outcomes show hope yet for multilateralism.

The conclaves began in Phnom Penh with the annual summit of the Association of Southeast Asian Nations. At the first of such in-person events in almost three years, ASEAN leaders took the positive step of agreeing in principle to admit East Timor as the 11th member of the organization.

As leaders moved on to Bali for the Group of 20summit, expectations were low after ministerial meetings in the run-up had failed to produce consensus. Earlier in the year, given fractures in the wake of Russia’s invasion of Ukraine, there was a question mark over whether the G20 could even go ahead or survive in its existing form.

In the end, the summit surpassed expectations by producing a joint declaration after intense negotiations, with leaders finding the compromises necessary to unite in declaring that “today’s era must not be of war” and pledging to uphold the multilateral system.

Reflecting on these three summits, three takeaways give reason for cautious optimism that multilateralism can yet be revived and play a major role in solving our challenges.

First, and perhaps most obviously, the return of in-person summitdiplomacy is a welcome uplift for global cooperation. Virtual formats played a useful interim role at the height of the pandemic but were never a substitute for getting leaders in the same room. That is especially when it comes to interactions on the sidelines, often as important as the main event.

China’s return to diplomacy at the highest level was a further boost, both for the nation and the rest of the world.

Leaders got to meet their new counterparts for the first time or build on existing relationships, which can only help global cooperation.

The second takeaway is that as grave as our challenges are, the threat of escalating conflict and severe economic pressures on all nations seem to be focusing minds and increasing the willingness to engage and cooperate—out of necessity if nothing else.

The G20summit was the second major one this year to surpass expectations after the 12th World Trade OrganizationMinisterial Conference in June surprised observers by agreeing on a plan to reform the organization and its dispute settlement mechanism. The G20 statement reiterated support for this WTO reform plan, which will be critical to get the free trade agenda back on track and provide a much-needed boost for the global economy.

Third, and perhaps most significantly for the long term, the recent summits marked an acceleration of the trend towards multi-polarization in international diplomacy, and in particular, the rising influence of non-aligned “middle powers” to shape multilateral outcomes.

The middle powers represented at ASEAN, the G20 and APEC have huge stakes in avoiding a bifurcation of the global economy that might result from a new cold war. They don’t want to be forced to pick sides and many show a growing willingness and ability to build bridges and restore positive momentum for multilateralism.

Indonesia is a prime example. The country’s strategic heft and non-aligned credibility make it well-placed to bridge different camps. PresidentJoko Widodo made a big political bet on the success of the G20 and has won praise for the deft diplomacy that kept the organization alive and got it to a joint statement.

The Indian delegation reportedly also played a big role in achieving consensus on language in the statement, with the BRICS group (Brazil, Russia, India, China and South Africa)—as well as Indonesia—turning out to be crucial swing voters in securing the joint statement. One Indian official said it was “the first [G20] summit where developing nations shaped the outcome.”

There is scope for this trend to continue next year as middle powers continue to rise in stature, and India and Indonesia take over the presidency of the G20 and ASEAN, respectively. Brazil will host the G20 the year after.

Over in Sharm el-Sheikh at the COP27 UN climate summit, another middle power—the host Egypt—also won praise for helping to shepherd a historic financing deal for poor countries affected by climate change. But the ultimate failure to reach a commitment to phase down fossil fuels was a sobering reminder of the huge difficulties that remain in forging the global consensus needed to overcome our shared challenges.

The selected solution providers will take part in a six-month acceleration period, where solutions will be evaluated in the Advanced Research on Integrated Energy Systems (ARIES) cyber range.

“We are thrilled to welcome and work with the first participants to the secure energy transformation,” said Jon White, director of NREL’s Cybersecurity Program Office. “These cyber-solution providers will work with NREL, using its world-class capabilities, to develop their ideas into real-world solutions. We are ready to build security into technologies at the early development stages when most effective and efficient.”

Xage uses identity-based access control to protect users, machines, apps, and data, at the edge and in the cloud, enforcing zero-trust access to secure operations and data universally. To test technology in energy sector environments, Xage provides zero-trust remote access, has demonstrated proofs of concept, and deploys local and remote access at various organizations.

Three major U.S.utilities, with more expected to join, are partners with CECA: Berkshire Hathaway Energy, Duke Energy and Xcel Energy. At the end of each cohort cycle, cyber innovators will present their solutions to the utilities with the goal to make an immediate impact.

Additionally, CECA participants benefit from access to NREL’s unique testing and evaluation capabilities, including its ARIES cyber range, developed with support from EERE. The ARIES cyber range provides one of the most advanced simulation environments with unparalleled real-time situational awareness and visualization to evaluate renewable energy system defenses.

Applications for the second CECA cohort will open in early January 2023 for providers offering solutions that uncover hidden risks due to incomplete system visibility and device security and configuration.

NREL is the U.S. Department of Energy’s primary national laboratory for renewable energy and energy efficiency research and development. NREL is operated for DOE by the Alliance for Sustainable Energy LLC.